March CPI: Pressure in the Energy Sector (as Expected); Tame Elsewhere (Surprisingly)

Summary

- Gasoline prices drove the energy component higher; electricity prices also contributed.

- Food prices provided a surprise by posting a fractional decline.

- Core prices rose less than expected; both goods and services components were contained.

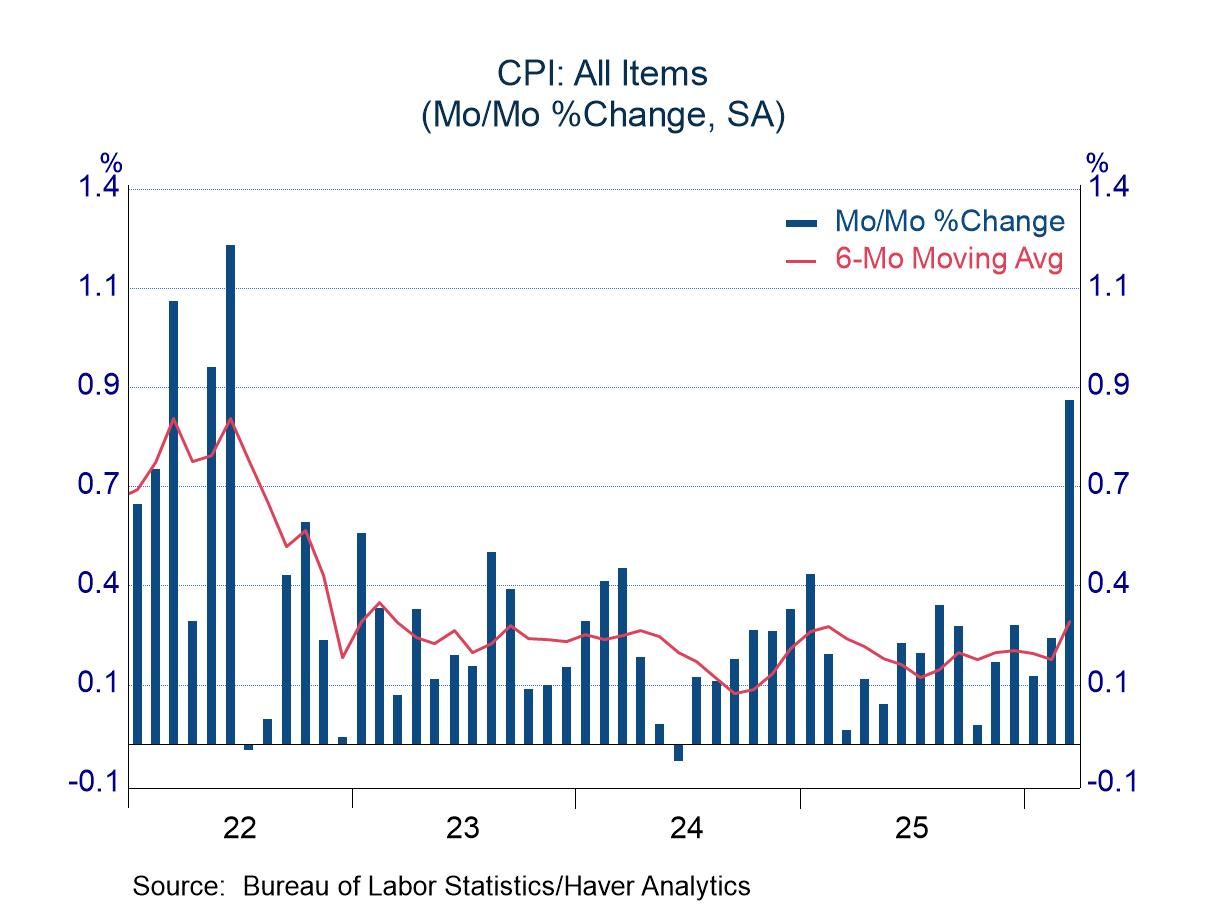

The Consumer Price Index rose 0.9% in March, easily the sharpest monthly rise since the inflation burst in 2022. Although pronounced in magnitude, the increase was not surprising, as essentially all analysts had built in pressure from the energy sector. Energy prices jumped 10.9%, led by a surge of 21.2% in gasoline prices. Other energy components wiggled: charges for electricity services rose 0.8%, offsetting declines in the prior two months; a drop 0.9% in the price of natural gas services followed sharp increases in the prior three months.

The press report from the Bureau of Labor Statistics showed food prices as unchanged, but calculating the shift to more than one decimal point showed a marginal decline (-0.005%) The dip was almost imperceptible, but it nevertheless was a welcome rarity. The decline occurred in the food-at-home component (i.e. grocery store prices, -0.2%); prices of food away from home (i.e. at restaurants and bars) rose 0.2%.

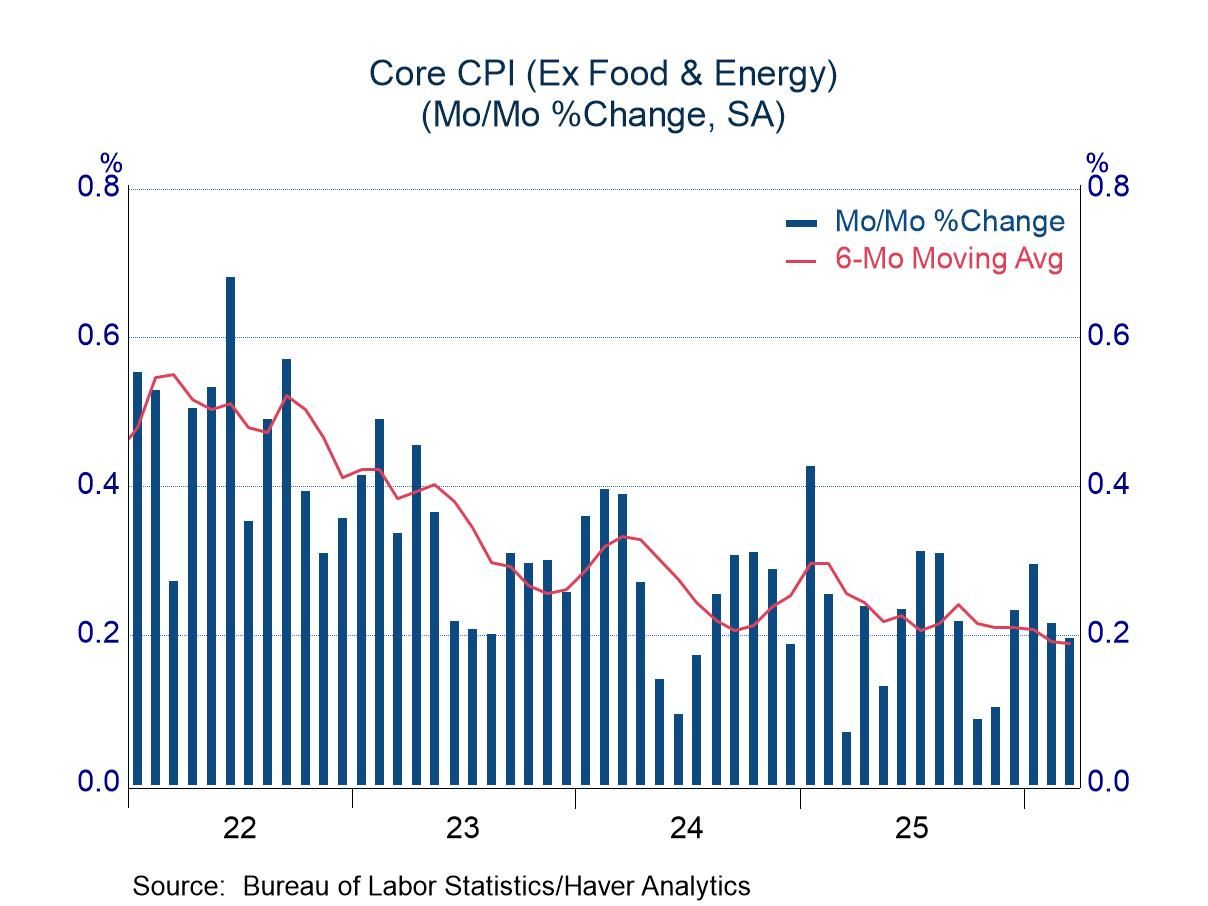

Core prices rose 0.2 percent, softer than the expected increase of 0.3%. Only two areas posted high-side readings. Apparel prices increased 1.0% after a jump of 1.3% in February, perhaps reflecting hope for an active spring selling season. Airfares jumped 2.7%, hardly surprising in light of recent energy developments. Sharper increases are likely in coming months because of higher fuel prices. Most other core items were contained, including declines of 1.0% in medical-care commodities and 0.4% in the prices of used motor vehicles. Prices of medical-care commodities have been quiet since the middle of 2024; the latest year-over-year change totaled only 0.3%. Prices of used cars and trucks have declined for four consecutive months, leaving a year-over-year decline of 3.2%.

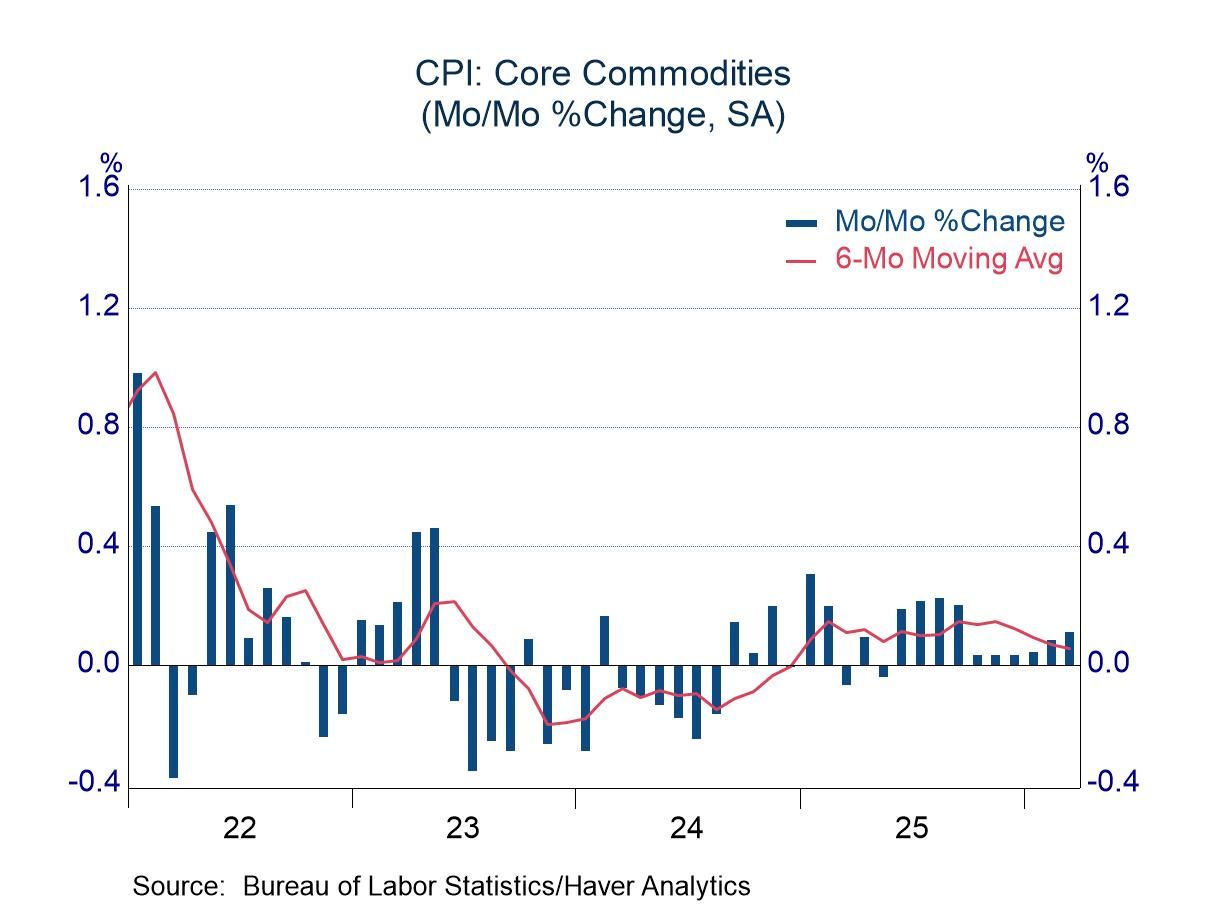

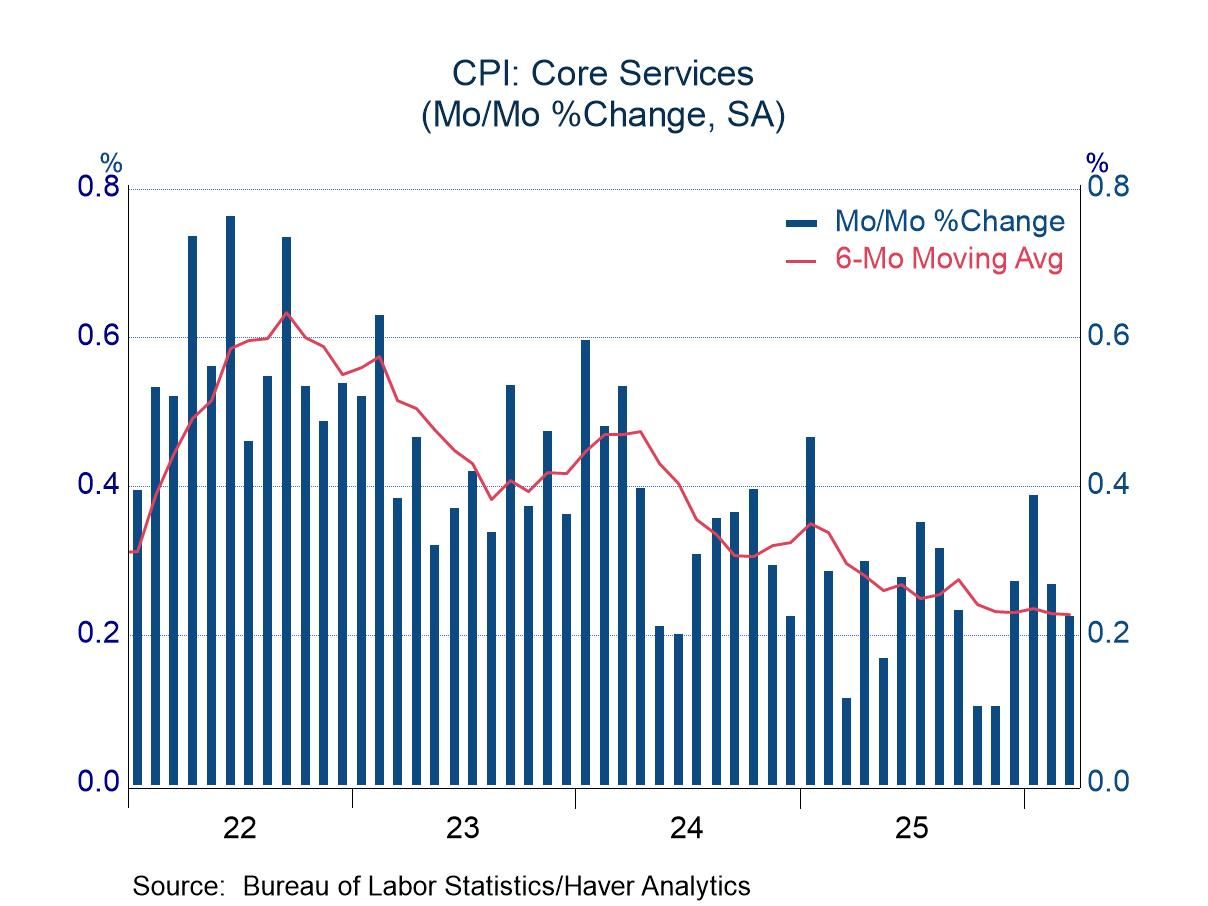

Although core prices were well contained in March, the outlook is uncertain because of potential passthrough from higher energy prices. At the same time, recent trends in the inflation rates for core goods and core services offer a reason to be optimistic, as both are decelerating. As shown in the left chart below, core goods prices in the past six months have been subdued, which has pulled the year-over-year change from 1.5% last fall (August to October) to 1.2% in March. Core service prices, shown in the right chart below, have registered changes of 0.3% or 0.4% in the three months before the 0.2% reading in March. However, results for October and November were restrained, and changes in the past six months in total show deceleration. The year-over-year change of 3.0% in core service prices in March reflects an advance of 3.3% in the first six months of this span (annual rate) and 2.7% in the past six months. The pattern is choppy, but it traces a decelerating trend.

The Consumer Price figures can be found in Haver's USECON database. The expectations figure is contained in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia