Global| Jun 04 2026

Global| Jun 04 2026Charts of the Week: Inflation Fears, AI Cheers

by:Andrew Cates

|in:Economy in Brief

Summary

The global macro backdrop continues to evolve in ways that would have surprised many investors at the start of the year. Expectations of widespread monetary easing have steadily receded as inflation has proven more persistent and economic activity more resilient than anticipated. The latest Blue Chip Financial Forecasts point to a growing bias towards policy tightening rather than loosening in several major economies (chart 1), while rising US job opening rates suggest labour demand remains firmer than expected (chart 2). At the same time, ongoing instability in the Middle East continues to generate supply-side inflation risks and lengthier delivery times (chart 3). There are, however, also reasons for optimism. Manufacturing activity appears to be finding some support from a reduction in effective tariff rates facing many major US trading partners (chart 4). More importantly, the AI investment boom continues to gather momentum. South Korea's semiconductor exports surged by an extraordinary 169% year-on-year in May, highlighting the strength of global demand for AI-related hardware (chart 5). Unsurprisingly, investors continue to direct capital towards those markets most exposed to these trends, with Taiwan and South Korea attracting substantial equity inflows (chart 6). The bottom line is that inflation concerns and higher-for-longer interest rates remain important risks, but they are increasingly being offset, for now, by a combination of improving economic conditions and one of the strongest technology-driven investment cycles in modern history.

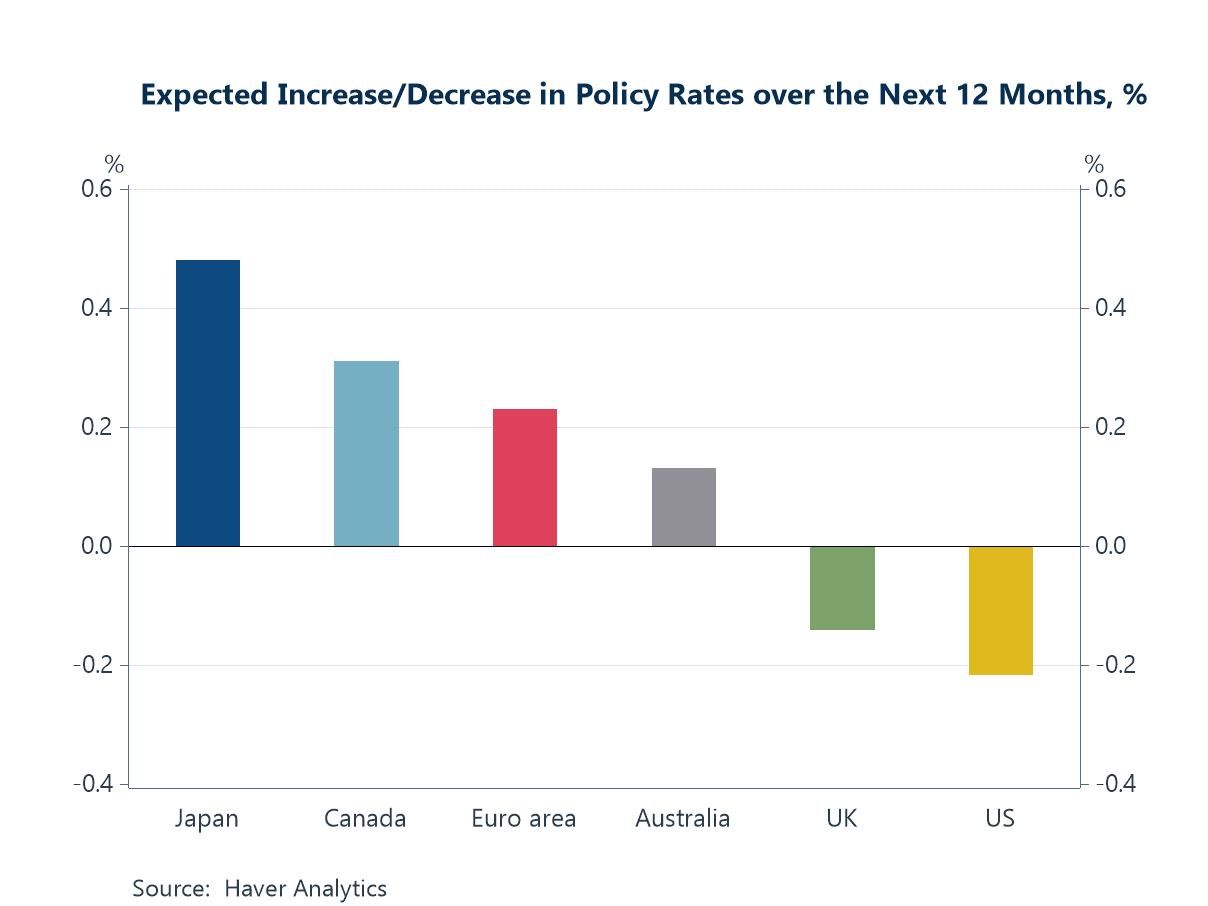

More Hawkish Central Banks One of the most important developments in recent months has been the steady shift in expectations surrounding monetary policy. Earlier this year, investors were largely focused on the prospect of widespread rate cuts as growth slowed and inflation appeared to be moving back towards target. Today, the narrative has changed materially. According to the latest Blue Chip Financial Forecasts survey, economists now expect policy rates to rise modestly over the next twelve months in Japan, Canada, the euro area and Australia. Only the UK and US are still expected to see rate reductions and even these are relatively modest compared with expectations earlier in the year. Perhaps more interesting is the growing divergence between economists and financial markets. While the Blue Chip panel continues to anticipate small reductions in policy rates in both the UK and US, market pricing has increasingly shifted towards the possibility of modest tightening instead. Stronger economic activity, firmer labour markets (in the US) and renewed inflation concerns have all contributed to this reassessment. The result is a global interest rate environment that increasingly looks "higher for longer" rather than one characterised by an aggressive easing cycle.

Chart 1: Expected Change in Policy Rates over the Next 12 Months

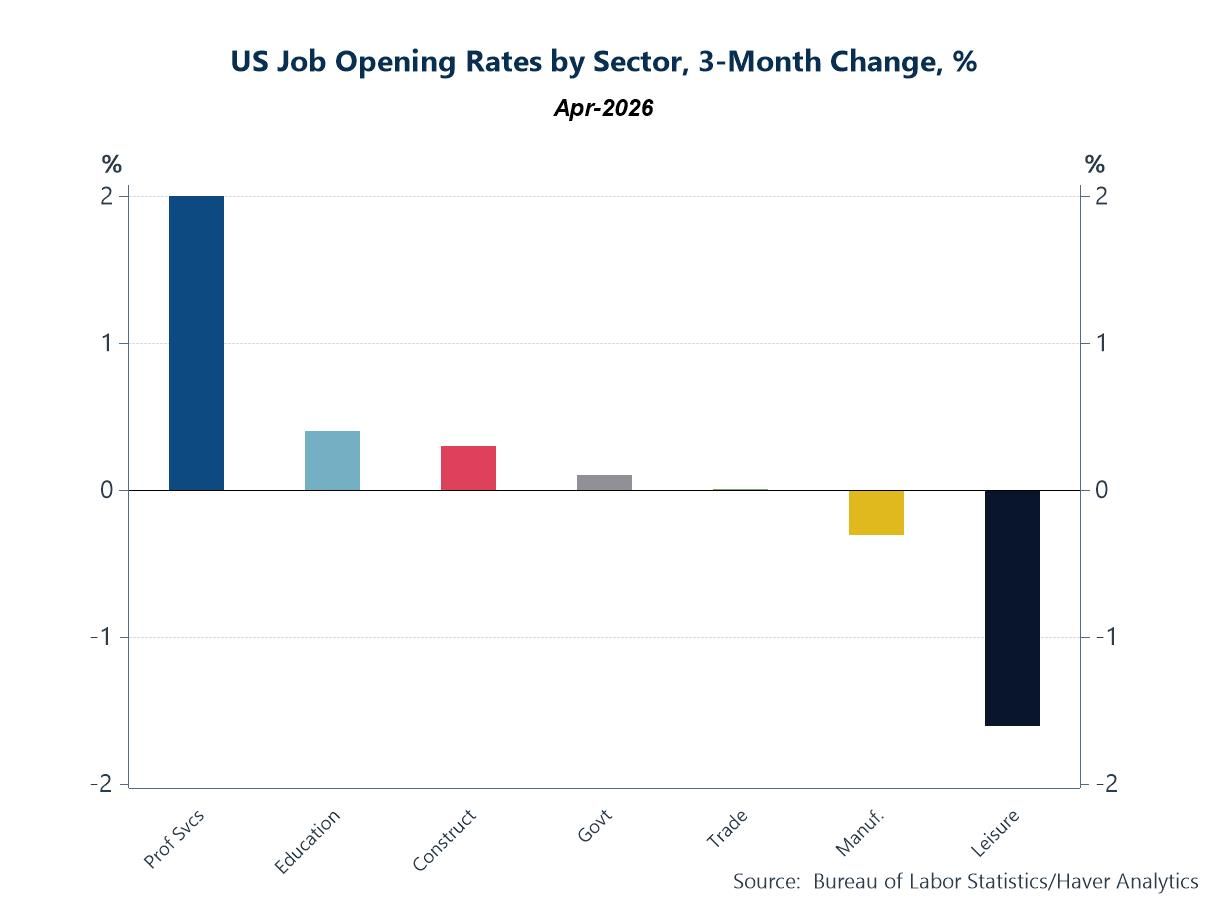

US Labour Demand Remains Surprisingly Resilient As noted, part of the reason markets have become less convinced about future rate cuts is that the US labour market continues to show surprising resilience. Job opening rates have actually risen over recent months, suggesting that labour demand may be reaccelerating despite growing discussion about AI-related job displacement. On that last note, the sectoral detail is particularly revealing. Professional and business services recorded the largest increase in job openings over the past three months, significantly outperforming most other sectors. This is noteworthy because professional services are frequently cited as one of the areas most vulnerable to disruption from generative AI. Rather than reducing hiring demand, however, AI investment may currently be creating additional demand for highly skilled workers involved in software development, consulting, implementation and digital transformation.

Chart 2: US Job Opening Rates by Sector, Three-Month Change

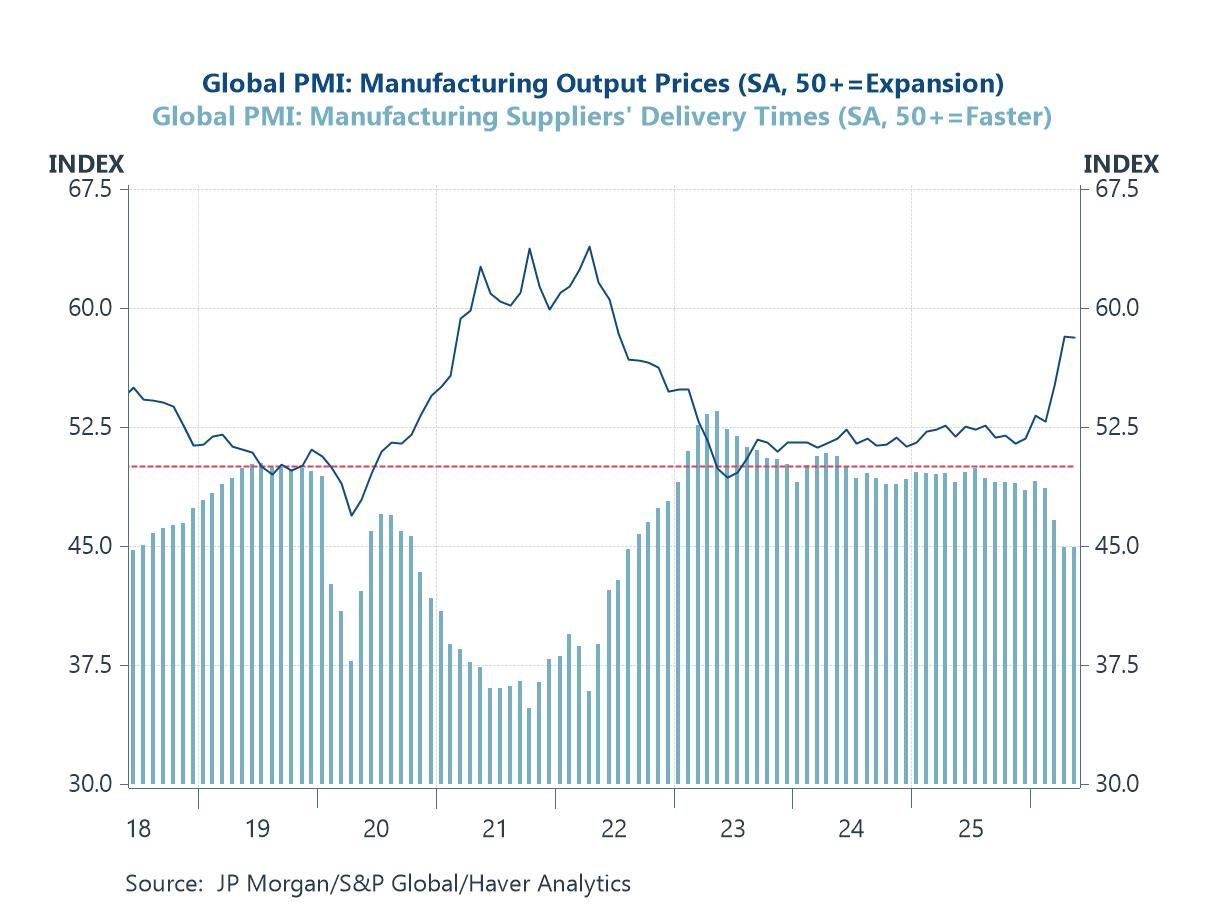

Middle East Tensions Continue to Generate Inflation Risks A second factor contributing to higher bond yields and reduced expectations of monetary easing is the persistence of supply-side inflation pressures. The latest global PMI surveys show that manufacturing output prices are climbing more sharply while supplier delivery times have lengthened compared with earlier in the year. Much of this appears linked to ongoing instability in the Middle East and the associated disruption to global shipping routes. Longer transit times, higher insurance costs and logistical bottlenecks have all contributed to upward pressure on manufacturing costs. There is, however, a modestly encouraging signal in the latest data. While delivery times remain relatively stretched, the most recent PMI survey does not indicate any significant further deterioration at the global level. This suggests that supply chain conditions may be stabilising rather than entering another period of sustained disruption.

Chart 3: Global PMI Manufacturing Output Prices and Suppliers' Delivery Times

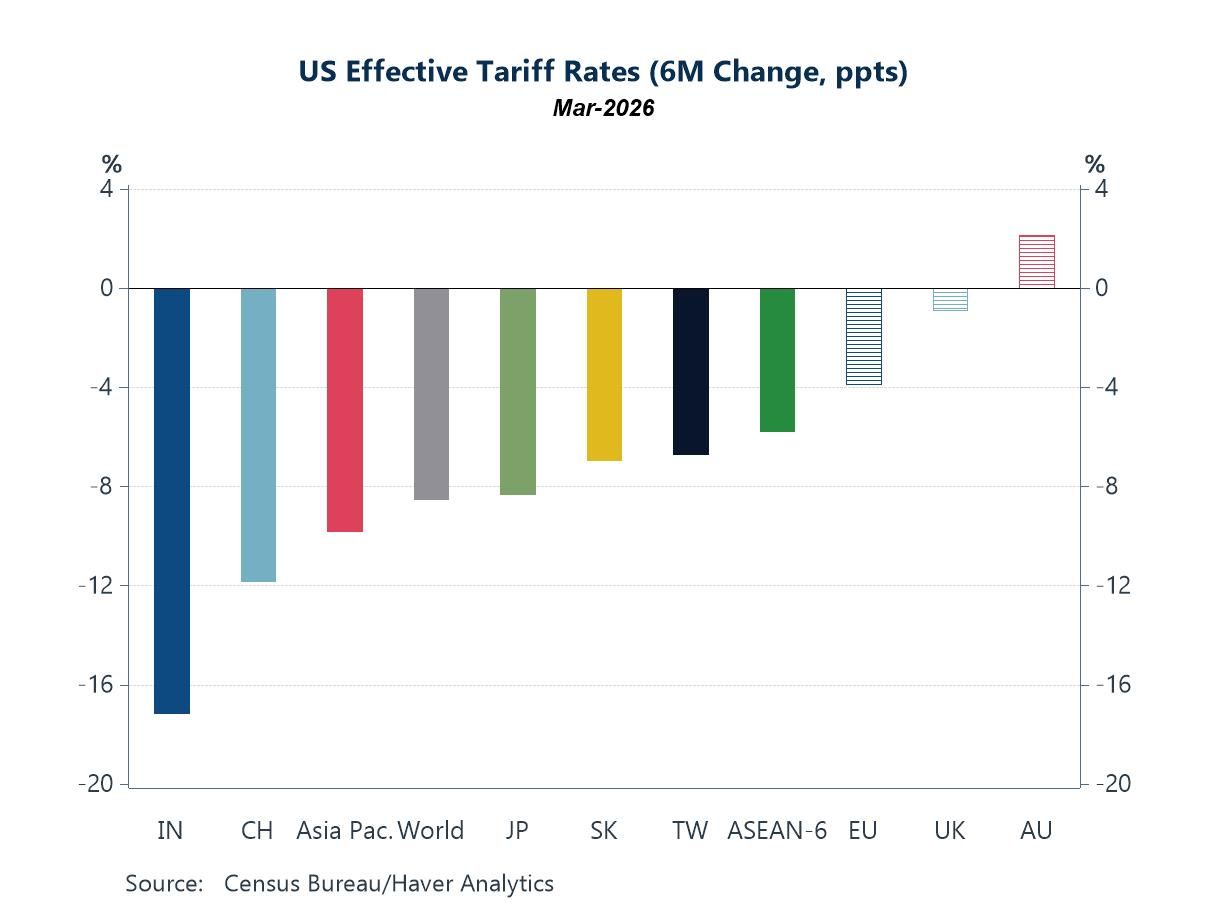

Manufacturing Is Benefiting from a More Benign Trade Environment While supply chain concerns remain important, there are also signs that some of the pressures facing global manufacturers may be easing. Effective tariff rates facing many major US trading partners have declined significantly over the past six months. The largest reductions have occurred across several key Asian economies including India, China, Japan, South Korea, Taiwan and members of ASEAN. Europe and the UK have also experienced some easing, although to a lesser extent, while Australia stands out as one of the few countries facing an increase in effective tariff rates. This chart may help explain some of the resilience visible in recent manufacturing surveys around the world. While trade policy uncertainty remains elevated, the actual tariff burden facing many exporters has become less restrictive.

Chart 4: US Effective Tariff Rates (Six-Month Change)

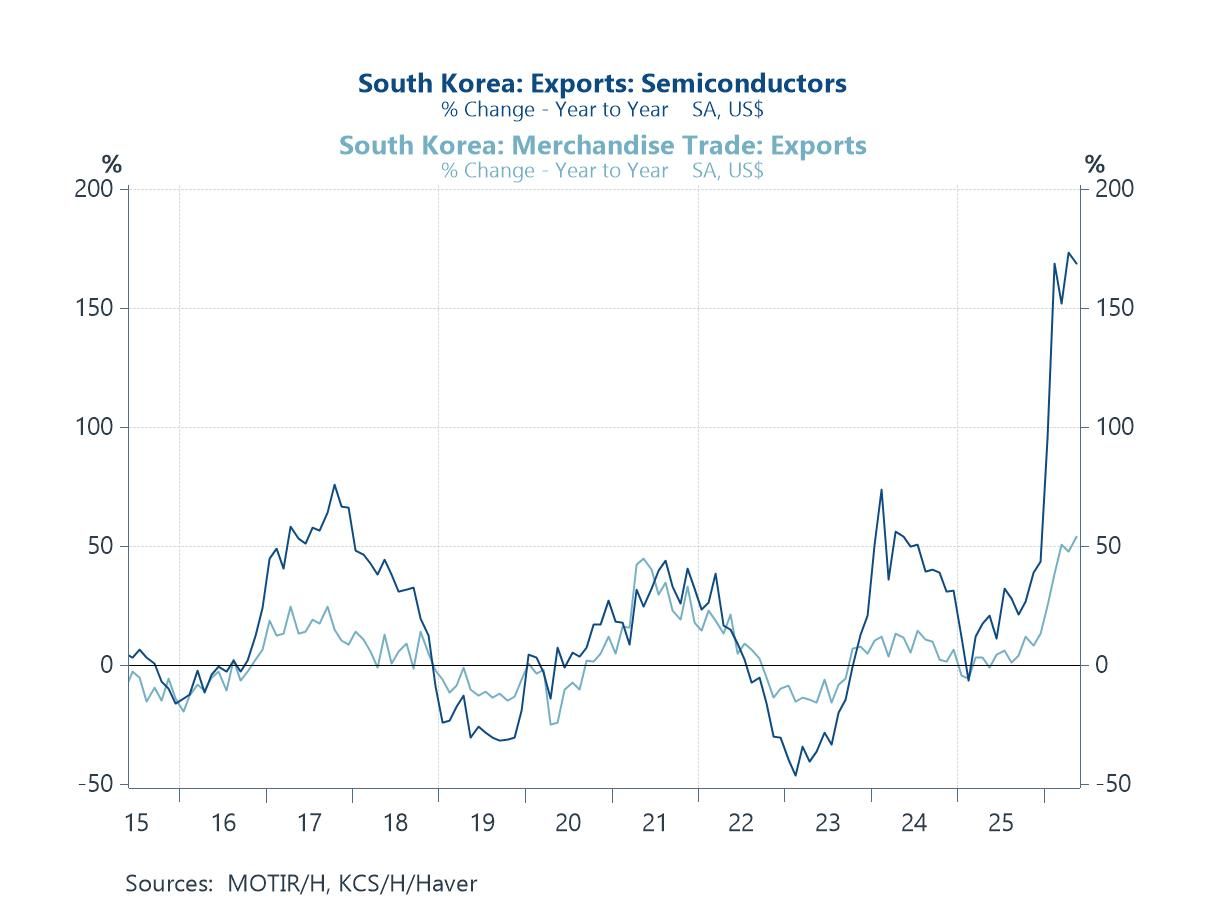

South Korea Highlights the Scale of the AI Boom If there is one chart that captures the extraordinary scale of the AI investment cycle, it is South Korea's semiconductor export data. Semiconductor exports surged by an astonishing 169% year-on-year in May, one of the strongest readings on record and a powerful illustration of the strong demand currently flowing through the global technology supply chain. South Korea occupies a pivotal position within the global semiconductor ecosystem, making its export data one of the most useful real-time indicators of AI-related capital expenditure. The rapid buildout of data centres, cloud infrastructure and advanced computing capacity is generating unprecedented demand for memory chips, processors and other semiconductor components. While concerns about eventual overcapacity remain valid, the near-term momentum remains remarkable. The strength of South Korean exports suggests that AI-related investment spending is continuing to accelerate rather than slow, providing an increasingly important support to global growth and trade at a time when many other sectors are facing cyclical headwinds.

Chart 5: South Korea Exports of Semiconductors

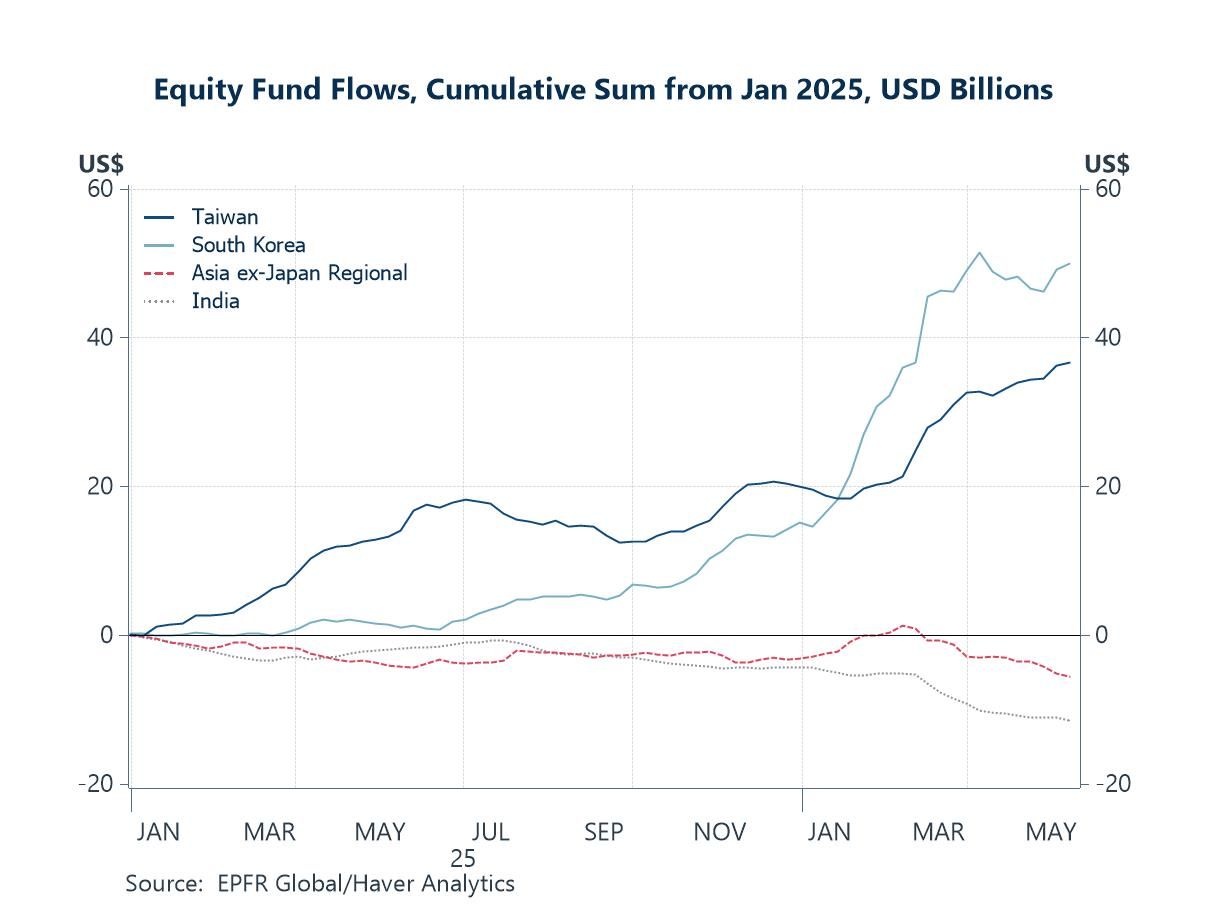

Investors Are Following the AI Money Our final chart this week highlights how investors are positioning for these trends. Equity fund flows since the beginning of 2025 show a striking divergence across Asian markets. Taiwan and South Korea have attracted substantial inflows, while broader Asia ex-Japan regional funds and India have experienced net outflows. The explanation is relatively straightforward. Taiwan and South Korea sit at the centre of the global AI supply chain and are among the largest beneficiaries of surging semiconductor demand. At the same time, both economies have also benefited from the recent easing in tariff pressures highlighted in the previous chart. Investors have therefore become increasingly selective, directing capital towards those markets with the greatest exposure to AI-driven growth. The concentration of flows into a relatively narrow group of markets inevitably raises questions about valuations and positioning. Nevertheless, the broader message remains clear. The AI investment boom continues to dominate both trade flows and capital flows across Asia and remains one of the most powerful forces shaping the global economy today.

Chart 6: Equity Fund Flows – Cumulative Sum Since January 2025

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief