France: INSEE MFG Weakens as Inflation Expectations Surge

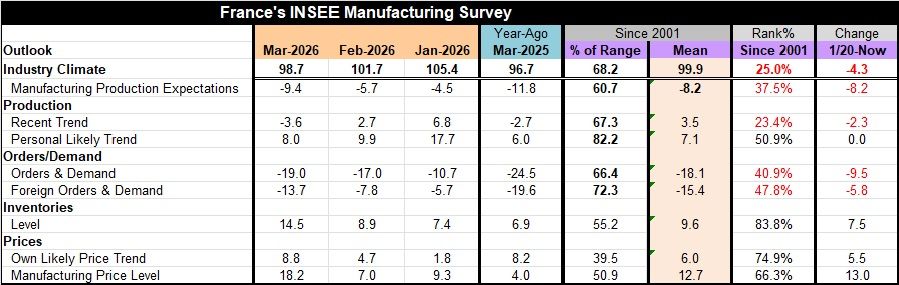

French manufacturing, as assessed by the INSEE survey, fell sharply to a reading of 98.7 in March from February’s 101.7. The industrial sector reading weakened further, having already fallen to 101.7 in February from 105.4 in January. The January reading was the strongest reading since July 2022, as the rebound from COVID had gathered momentum.

Now, events in the Middle East, a dragged-out war in Ukraine, and a long period of inadequate growth in the wake of COVID, and the imposition of Tariffs by the United States are taking a toll on an economy less able to absorb shocks.

Just as inflation had settled down, there is a new oil shock in progress, a result of the attack in Iran, meant to defang it from its nuclear obsessions and its ambitions to dominate geopolitics in the Middle East by supporting various regional militia groups. The European Central Bank had corralled inflation more than controlled it, but now the ECB is more worried about oil and its impact on inflation and is determined not to make ‘the same mistake again’ referring to its procrastinated timeline for raising rates during COVID. Both the BOE and the ECB have said if the war is still in progress at the time of their next meetings, a rate hike is likely.

So, in several ways, it is a different world. In the United States, it is the same old world as the Fed has been uncommunicative about its strategy in the face of war and rising energy prices. The Fed has offered essentially no guidance. But the ECB and BOE have made clear they are not waiting on the Fed this time around.

The French economy’s main industrial indicator has a 25-percentile standing in March, a lower one-quartile ranking. Production expectations slipped to -9.4 in March from -5.7 in February, corresponding to a 37.5 percentile standing. The recent trend and own industrial likely trend both eased on the month, with the overall trend to 23.4 percentile standing and the personal likely trend to a still-above-median 50.9 percentile standing. Industrial respondents see the overall manufacturing situation as worse than their own personal prospect. Is that denial in action or excessive macroeconomic pessimism? That is something to watch for.

Orders and demand as well as foreign orders and demand fell in March. They had also fallen in February relative to January. The March readings show a 40.9 percentile standing for orders and demand against a slightly higher 47.8 percentile standing for foreign orders and demand.

The price survey news is bad. Both the own likely price trend and the manufacturing price level are higher in March and had already moved higher in February relative to January. The price expectations rank in the 74.9 percentile for own likely price trend and at the 66.3 percentile for the manufacturing price level.

Summing up All in all, the manufacturing situation in France is in flux. Monetary policy is hostage to war developments, as seems reasonable. But the war is not concluding quickly, despite a quick miliary emasculation of Iran’s armed forces. The leadership is trying to cling to power in a country where it has brutalized and subjugated its people, knowing full well that if the regime falls, the leadership will be on the run. So, the leadership, decimated as it is, has dug in and moved to be as defiant and possible—hoping that ‘politics’ on the other side will cave in first. The closing of the Strait of Hormuz is its key trump card, but it is not clear how long it will be able to make that threat effective. That is the whole ‘game’ in the Middle East now. It is less about Iran and more about oil and oil supply. Stay focused on that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global