Factory Orders: Lots of Noise, but Also Firm Trends in Recent Months

Summary

- Aircraft bookings fueled durable bookings in April, accenting solid gains in prior months.

- Petroleum prices inflated nondurable orders in April, but orders ex-petrol advanced as well.

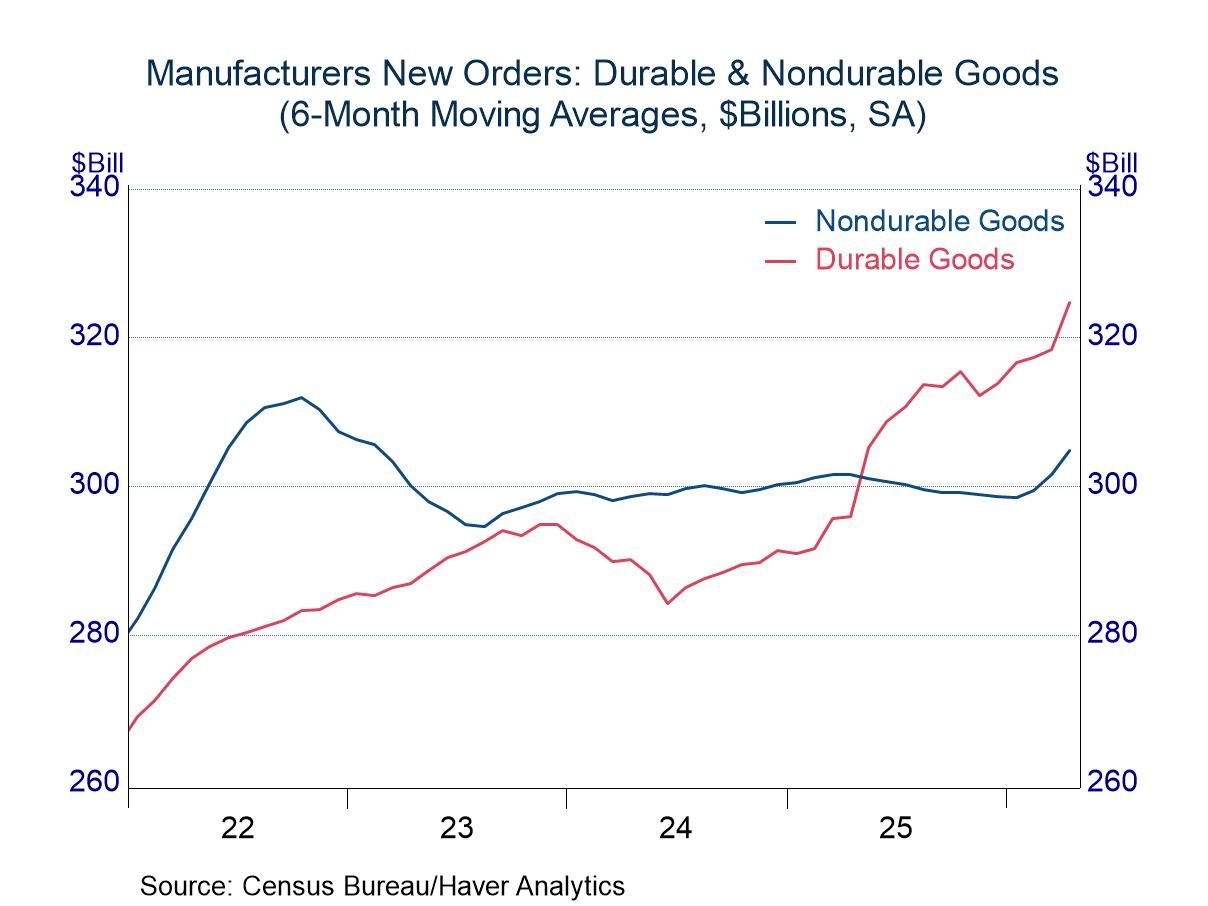

New orders for manufactured goods jumped 4.8 percent in April, led by a surge of 8.0% in the durable-goods sector and reinforced by an advance of 1.4% in orders for nondurable goods.

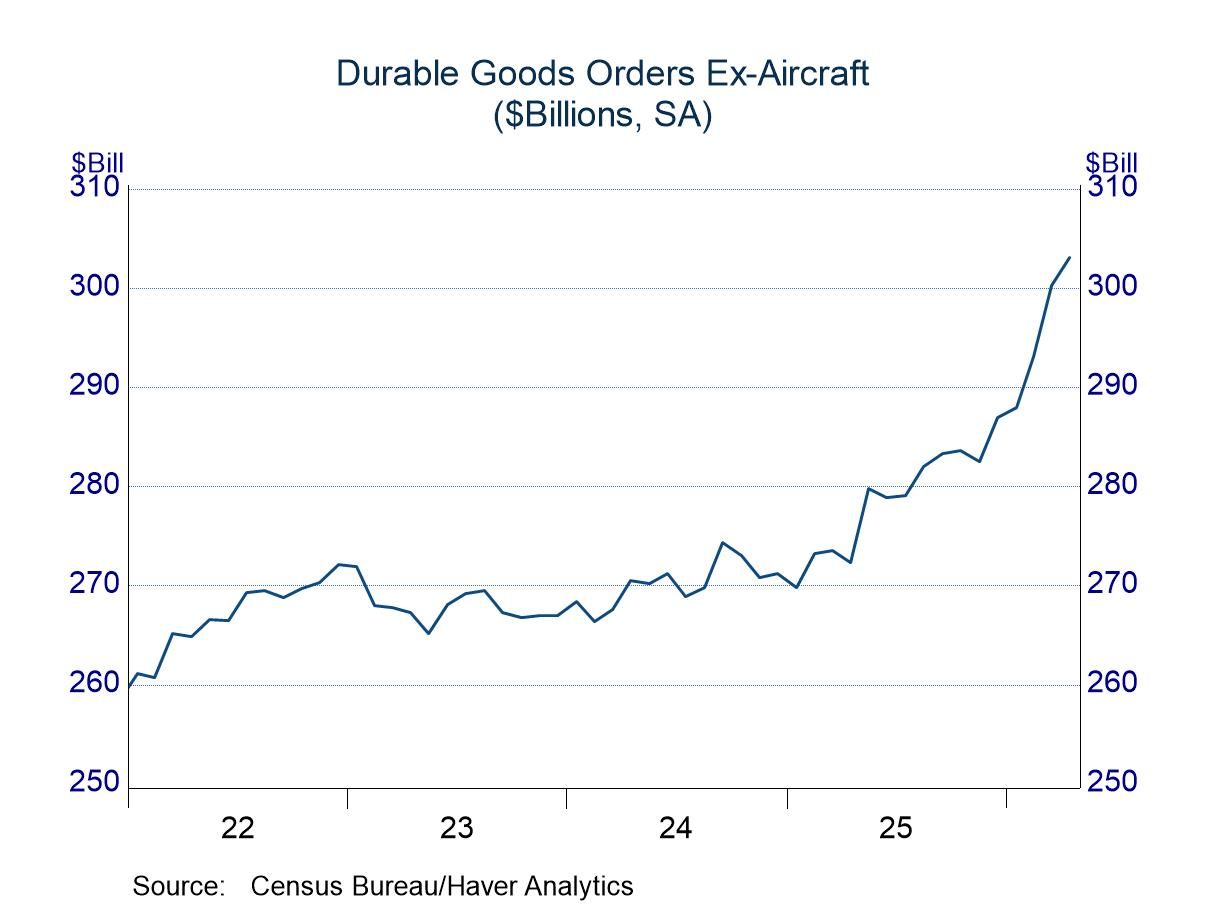

The increase in orders for durable goods was heavily influenced by the volatile aircraft category, which posted a striking advance of 113.3%. However, the jump did little to influence the underlying trend, as it followed a cumulative decline of 51.6% over the prior four months. Excluding aircraft orders, the durable component rose 0.9%, reinforcing a strong upward trend that began late last year (chart, above right). Bookings for computers, despite a dip in April, have been a force behind the advance excluding aircraft, but other areas have been firm as well (machinery, primary metals, fabricated metals). The results in the durable sector were in line with the preliminary estimate released last week, which showed an increase of 7.9% overall and 0.8% ex-aircraft.

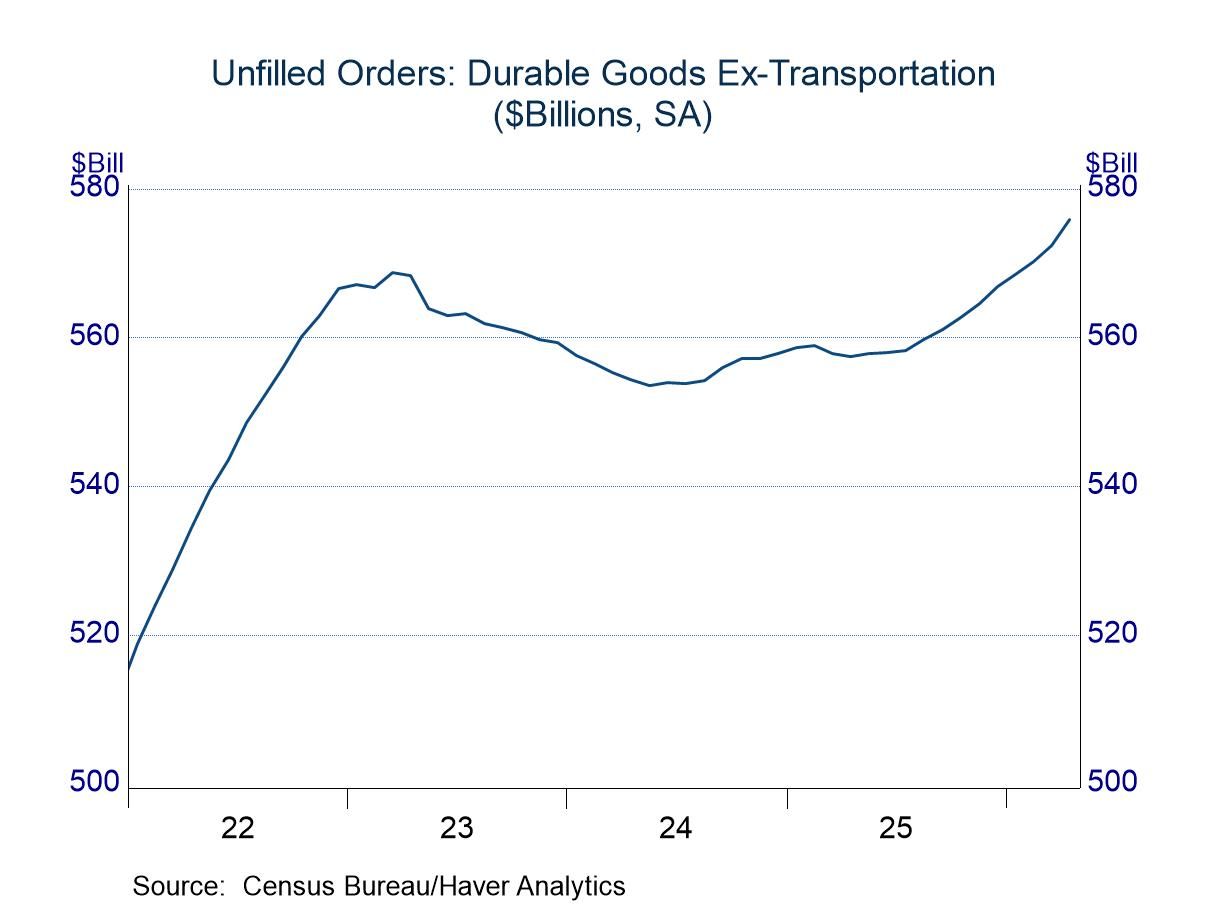

The strong performance in new orders for durable goods has generated an upward trend in unfilled orders. Backlogs started to move higher in the second half of last year, and they added to that trend with an increase of 0.6% in April (chart, lower left).

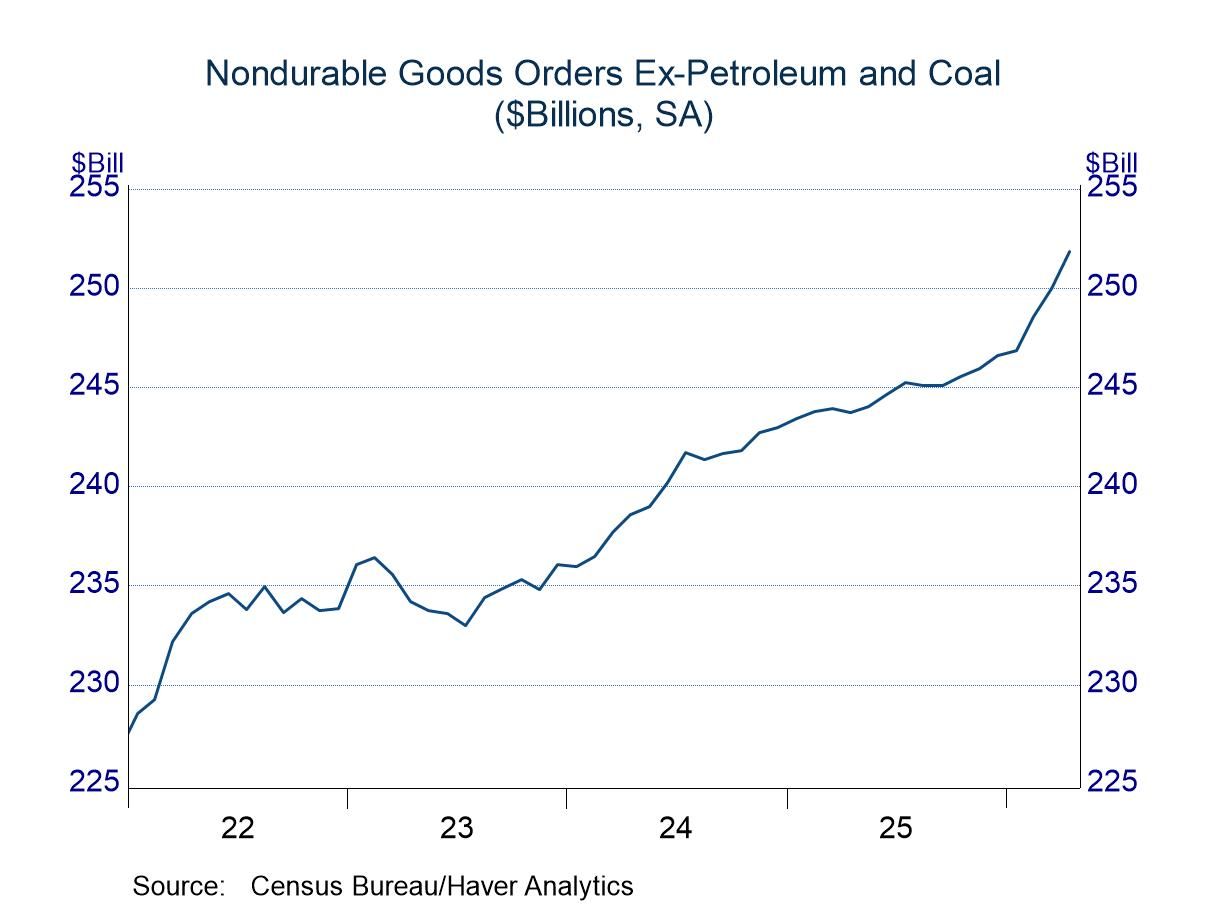

The increase of 1.4% in the nondurable sector was led by a jump of 4.0% in the petroleum and coal category, which followed an average increase of 6.8% in the prior three months. These increases, of course, primarily reflected price changes rather than shifts in real activity. However, bookings outside of petroleum and coal have been firm on balance, increasing 0.8% in April after advances of 0.6% and 0.7% in the prior two months (chart, lower right). Nondurable orders also rose in the four months before this recent burst, but the changes were small. Orders for nondurable goods are typically shipped upon arrival, and thus backlogs are not tracked, but the recent flow of bookings certainly represents a solid trend.

The factory sector data are available in Haver’s USECON database. The Action Economics Forecast Survey is in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global