EMU Inflation and An ECB Rate Hike

Channeling ‘The Who,’ the ECB implemented its 'We Won’t Get Fooled Again' rate hike. During COVID, inflation spiked around the world as central bankers were late with rate hikes. Arguably, too many of them followed the lead of the U.S. Federal Reserve. The ECB leaned against that by hiking its key deposit rate by 25bp today.

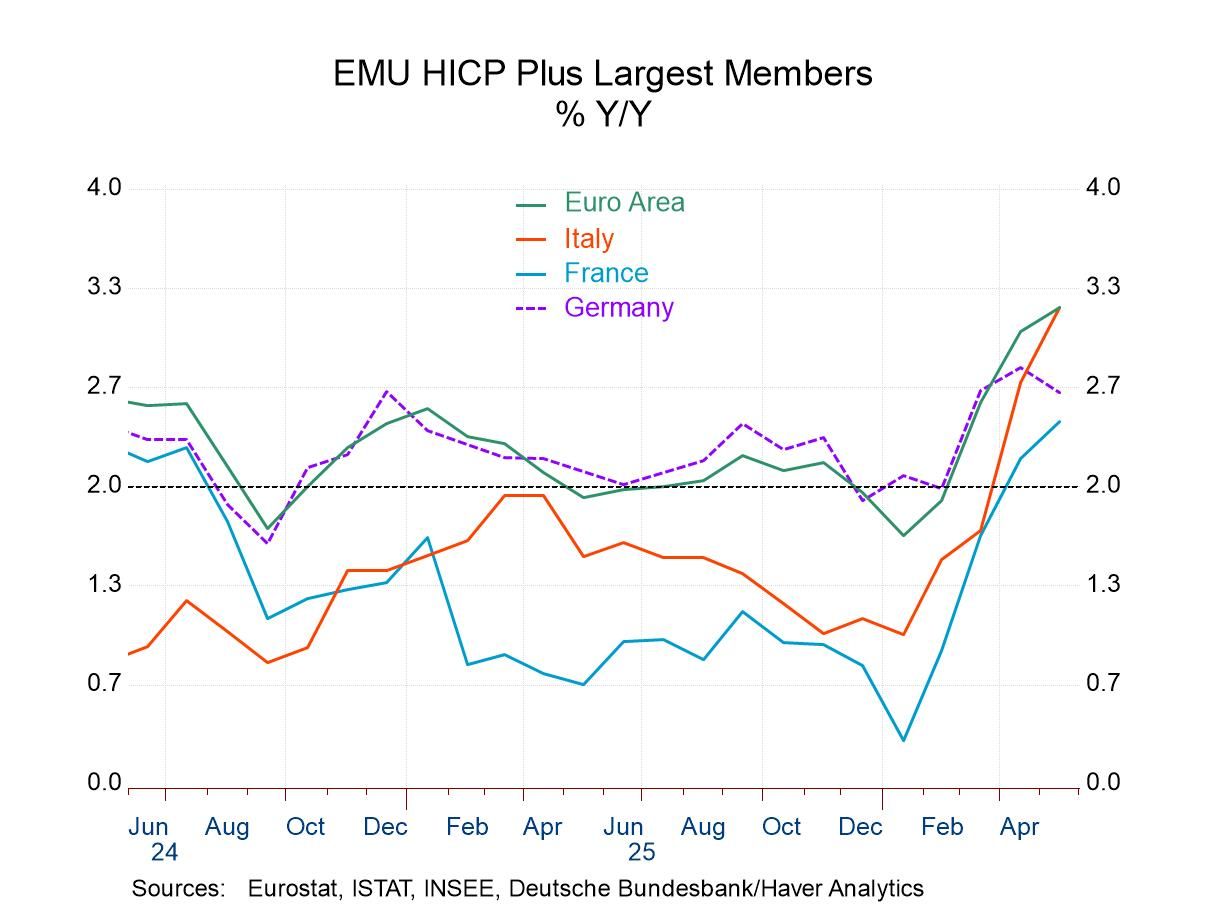

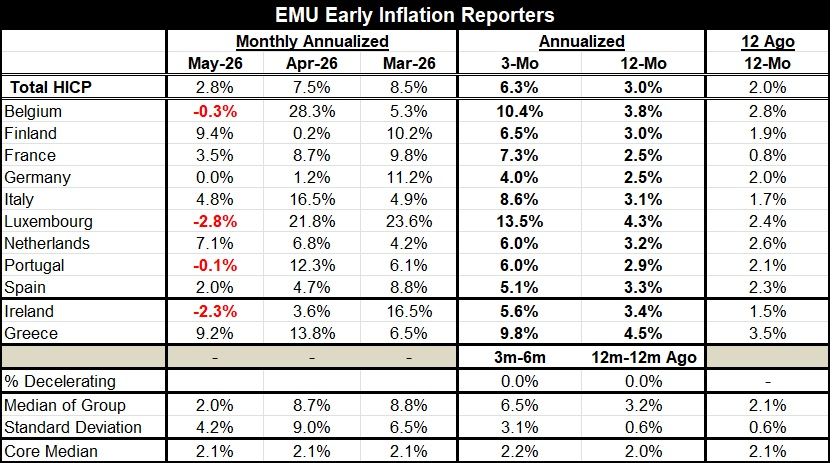

Both the chart and the table show how inflation has recently soared sharply in the countries of the European Monetary Union. However, the price gains are concentrated in the headlines and driven by oil prices. Still, oil price gains this large and persistent—and potentially long-lasting—will permeate the pricing of most goods since there will be knock-on effects through transportation costs. The ECB has therefore taken a step to keep in line with the increase in energy prices.

If there are further impacts from energy prices, the ECB has the door open to move again. But if price pressures wane, the ECB will be under no pressure to act again.

For now, we can see that headline inflation across the European economic area is generally accelerating strongly and somewhat uniformly. The three-month annualized HICP rose at a 6.3% annual rate. With three-month inflation among these 11 long-lived EMU members, the highest three-month pace is 13.5% in Luxembourg. Germany has the lowest inflation over three months, at a 4% pace.

The 12-month inflation pace is better contained, of course, with a top gain of 4.5% in Greece compared to the slowest pace at 2.5% in France and Germany. Over three months and 12 months, headline inflation shows deceleration occurring in none of these countries on these two timelines. So, the ECB action is timely.

The median gain for the group over three months is 6.5%, close to the overall EMU weighted result. The 12-month median is at 3.2%, also close to the 12-month EMU pace.

By comparison, I calculate the median for the core at 2.2% over three months and 2.0% over 12 months—right on the ECB’s inflation objective. Core inflation is never the central bank’s target, but it does strip out the volatility. So, we can understand the ECB’s move as an effort to keep up with what might be a changed trend. And if it is not a changed trend, then the ECB can peel its rate hike back. But for now, it is going to stay close to the short-term impact on the inflation rate to be sure that it will control inflation developments in the future. This is a good way to not repeat past mistakes.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global