Asia| Jun 02 2026

Asia| Jun 02 2026Economic Letter from Asia: Two Halves, Emerging Risks

In this week’s Letter, we examine a tale of two halves between China and India, highlighting the contrasting relationship between economic fundamentals and currency performance in Asia’s two largest emerging economies. In China, a recent run of softer economic data has pointed to slowing growth (chart 1), yet the Chinese yuan has remained one of the region’s strongest-performing currencies this year (chart 2). India presents the opposite picture: economic growth prospects remain among the brightest in Asia, but the Indian rupee has continued to face downward pressure amid persistent foreign investor outflows and a marked decline in central bank foreign exchange reserves (chart 3).

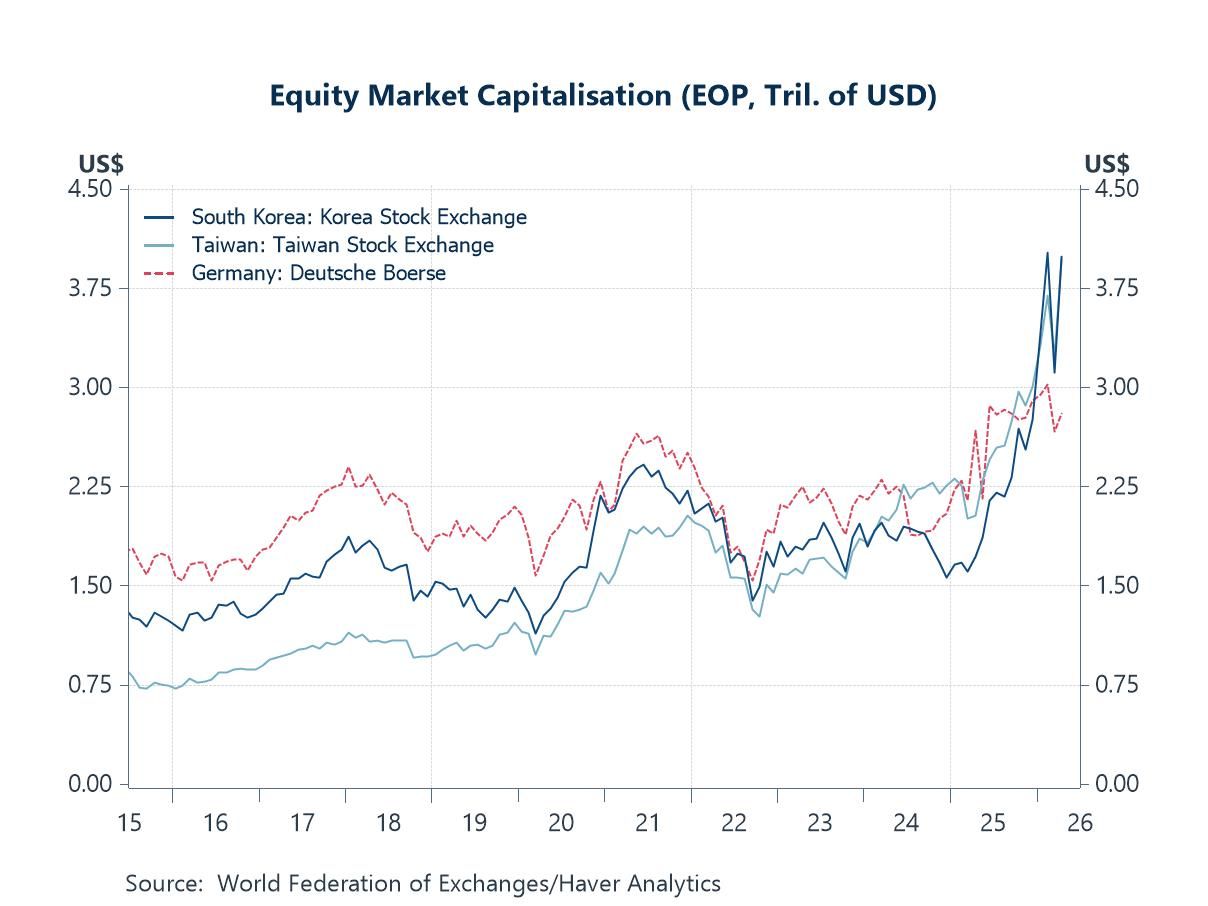

Beyond China and India, the broader region is also confronting emerging inflation risks. In addition to elevated energy prices stemming from the closure of the Strait of Hormuz, concerns are growing over the potential development of a “Super El Niño” event, which could weaken agricultural output and add further inflationary pressure through the food channel (chart 4). At the same time, the battle between inflation concerns and AI-driven optimism continues to shape market sentiment. Equity markets in major AI beneficiaries such as Taiwan and South Korea have seen their market capitalisations surpass those of several larger developed markets, including Germany (chart 5).

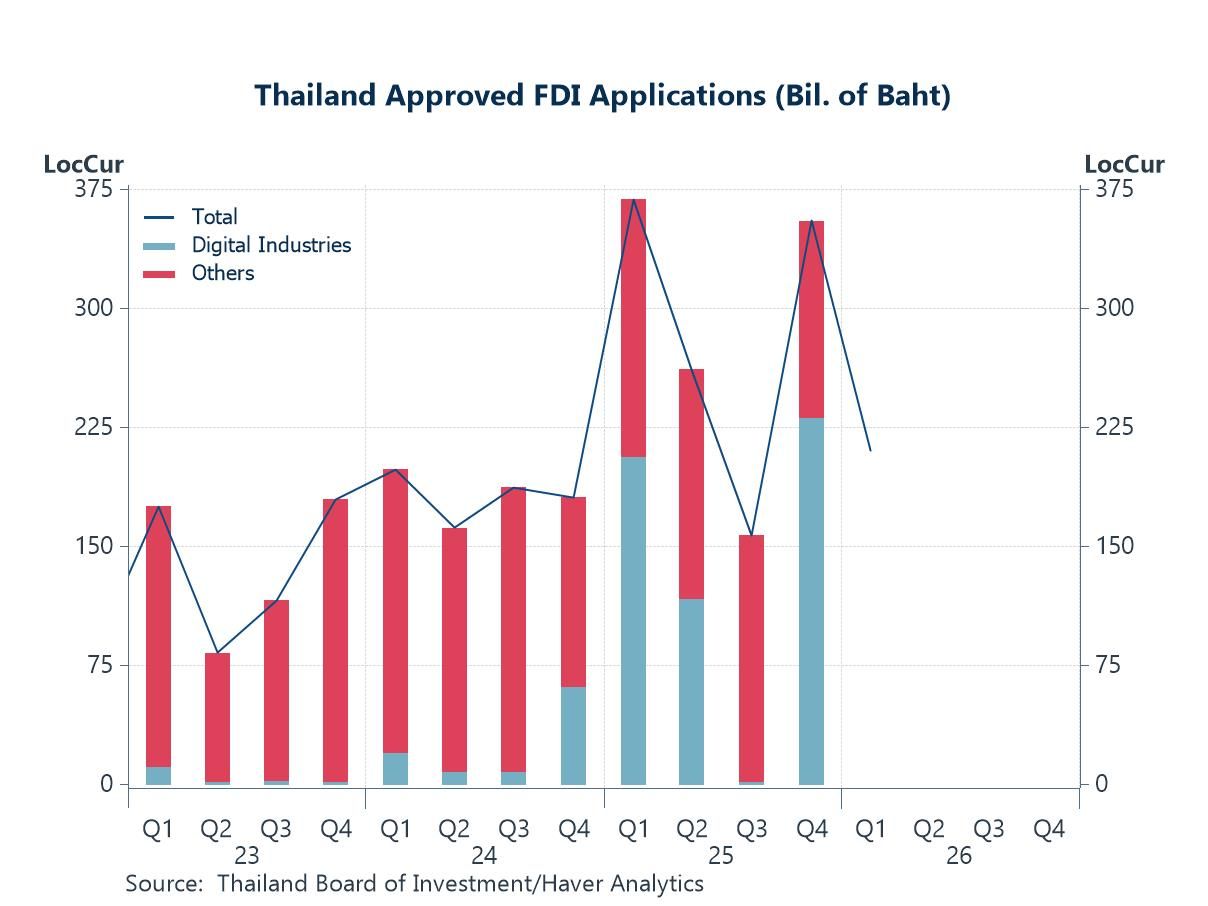

Moreover, the benefits of the current AI investment cycle are not confined to the region’s technology leaders. Economies such as Thailand are also seeing positive spillovers from the current AI investment cycle. In particular, Thailand has recorded a surge in FDI linked to investments in digital infrastructure and AI-related industries (chart 6). Countries across the region are increasingly positioning themselves to participate in the ongoing buildout phase.

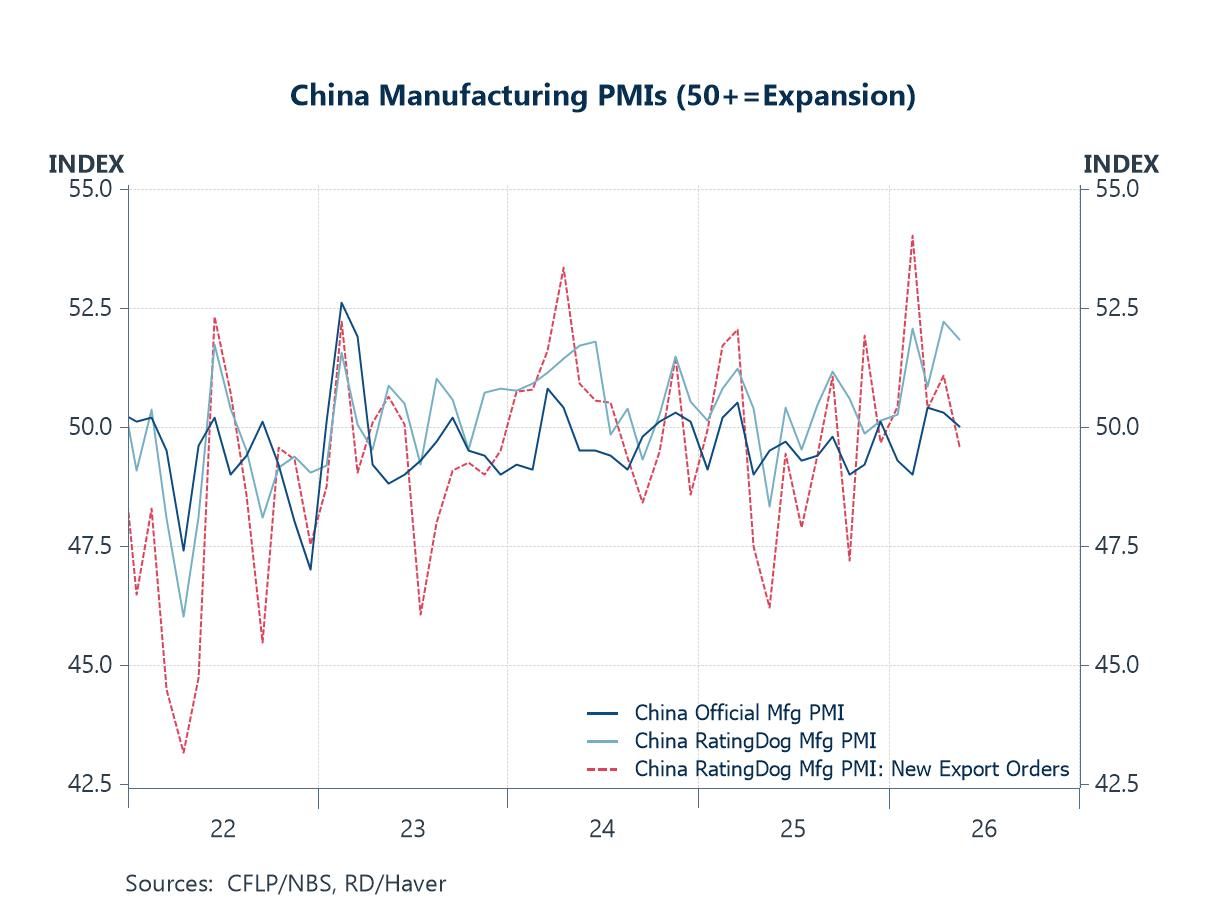

China China’s unofficial manufacturing PMI was released earlier in the week, showing a pullback to 51.8 in May (chart 1), though it remained in expansionary territory. The decline mirrors the weakness seen in the official PMI readings and was accompanied by a sharp drop in new export orders, which fell into contractionary territory for the first time in months. These developments come amid a run of disappointing economic data from China, with growth slowing even in the export-oriented industrial sector, generally regarded as a stronger driver of activity than more domestically focused sectors. This perhaps suggests that while China may be relatively insulated from the effects of the Strait of Hormuz closure compared with other Asian economies, such insulation is not complete, and some adverse spillovers are nonetheless becoming apparent.

Chart 1: China manufacturing PMIs

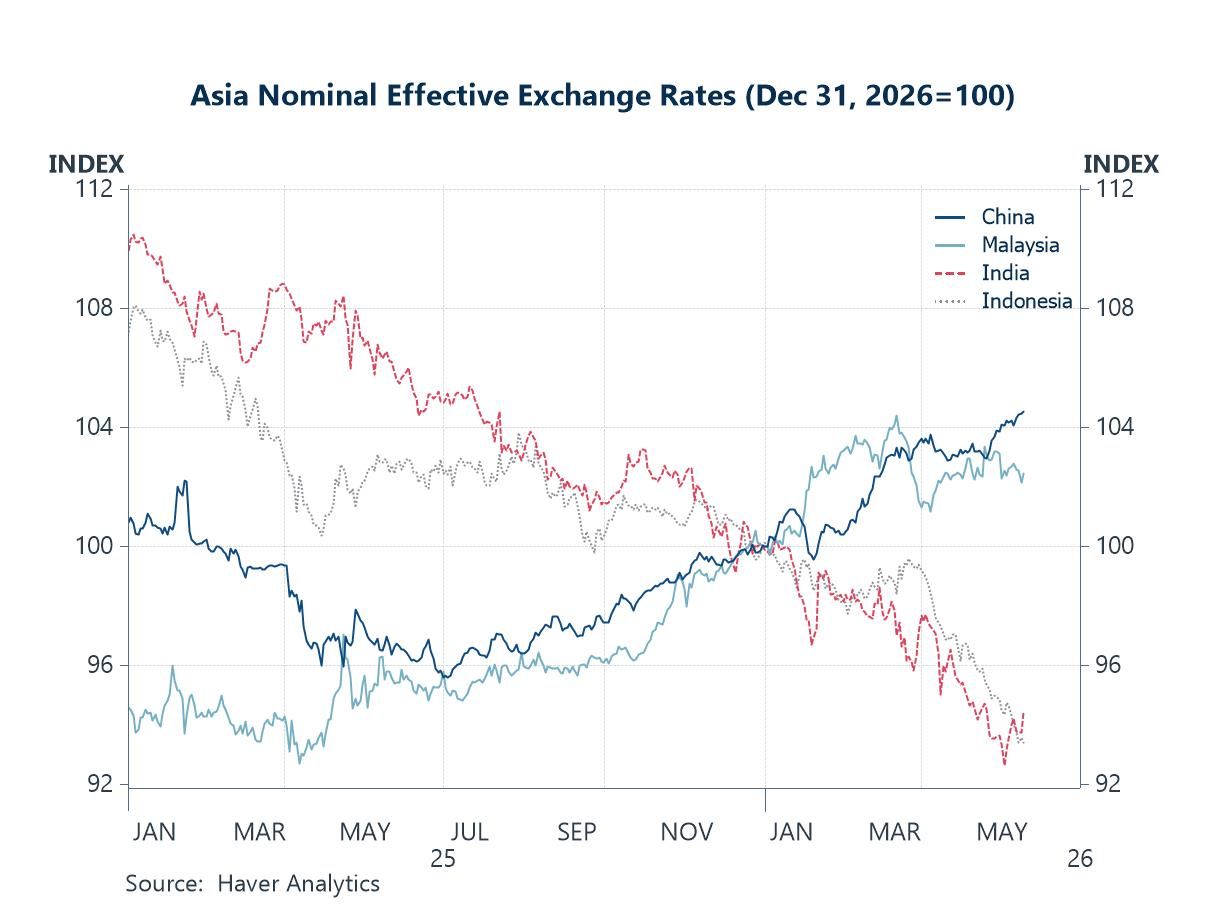

Yet despite signs of slowing growth in China’s recent data releases, the yuan has continued to trend higher (chart 2), making it the best-performing Asian currency year-to-date. Observers have attributed the yuan’s relative strength to several factors. These include resilient export growth, particularly in higher-value-added goods, as well as possible safe-haven inflows amid heightened geopolitical uncertainty. Some have also pointed to weakness in the currencies of several of China’s major trading partners as a contributing factor. In contrast, the Indian rupee and Indonesian rupiah have been among the region’s weakest performers this year. For the rupiah, much of the depreciation has been linked to concerns over Indonesia’s economic outlook, particularly on the fiscal front, as authorities pursue costly policy initiatives alongside broader policy changes that may have unsettled investors. India’s situation is examined in greater detail in the next section.

Chart 2: Asia nominal effective exchange rates

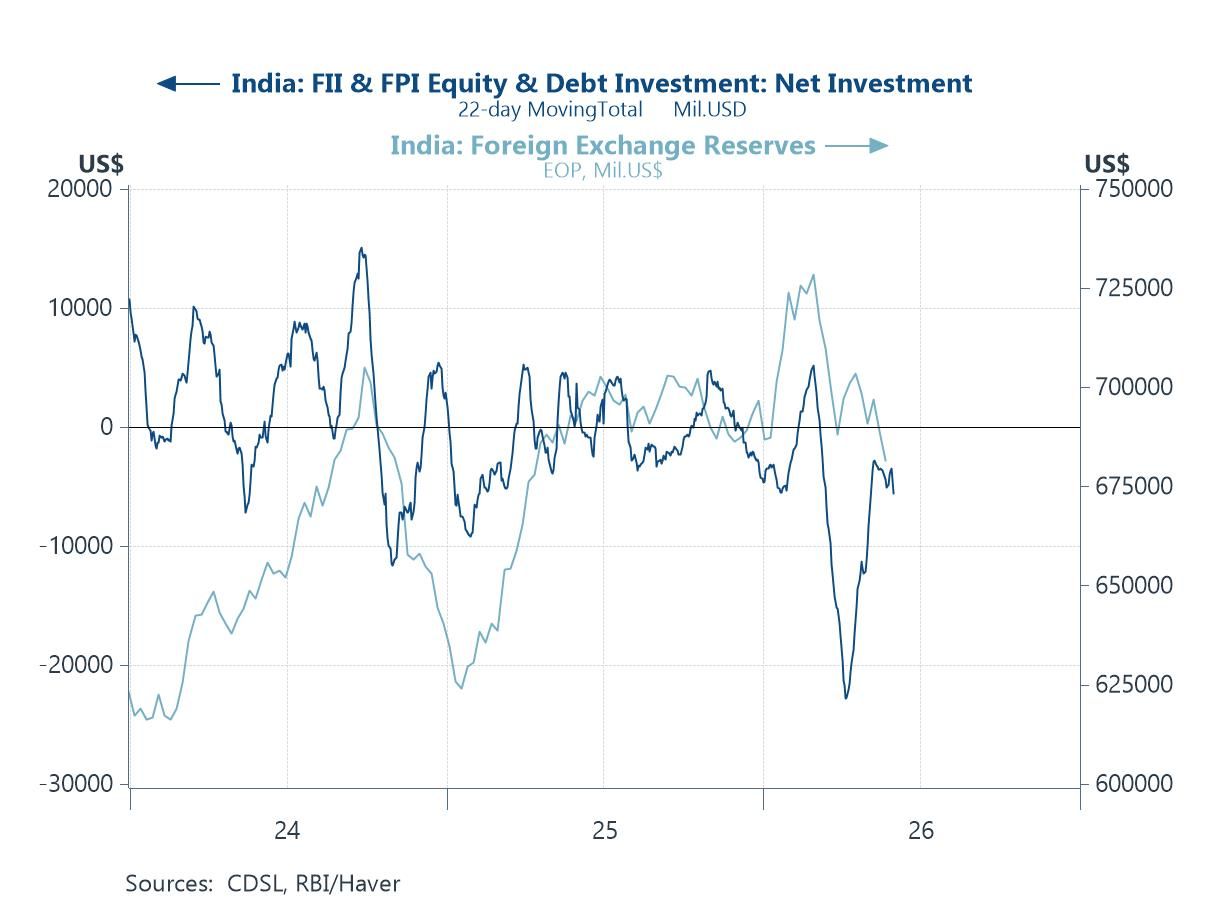

India In contrast to the Chinese yuan, India’s rupee has depreciated. While the yuan has strengthened this year despite recent signs of slowing growth in China, the rupee has remained under pressure despite robust actual and expected growth in the Indian economy. In fact, the rupee’s weakness has been relatively persistent, dating back to the period when US tariff announcements—and the broader threat of escalating trade tensions—first began unsettling financial markets. The currency has remained weak despite a range of measures introduced by Indian authorities, including suspected stabilisation interventions in the foreign exchange market and restrictions on gold imports, among other steps. Even so, continued investor outflows throughout the year (chart 3) have contributed to sustained downward pressure on the rupee. Meanwhile, the central bank’s foreign exchange reserves have fallen markedly from the peaks reached earlier in the year.

Chart 3: India investor flows and foreign exchange reserves

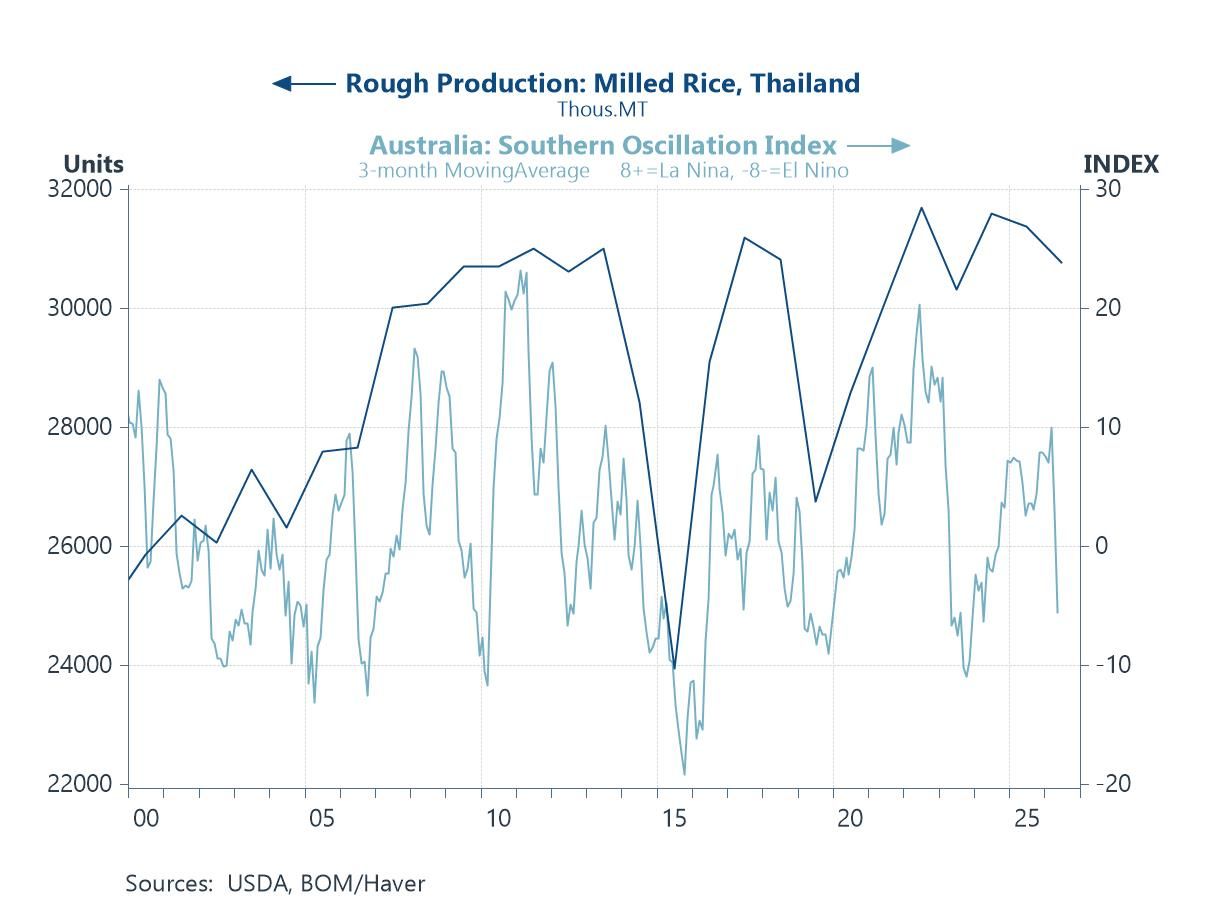

Possible El Nino effects While the world continues to grapple with the inflationary consequences of the prolonged closure of the Strait of Hormuz, new inflation risks are already emerging on the horizon. In particular, concerns have recently grown over the potential development of a “Super El Niño” event in the coming months. Should such an event materialise, higher temperatures and reduced rainfall could weigh on agricultural production across parts of Asia. This would create an additional supply-side shock for the region, exerting upward pressure on food prices at a time when inflation concerns are already elevated. Indeed, food price pressures are beginning to emerge even before any material impact on crop production has been observed, as anticipatory buying has started to lift prices. As shown in chart 4, previous El Niño episodes have been associated with weaker agricultural output in parts of Asia, including lower rice production in Thailand. However, the effects have varied considerably across countries and crops, extending well beyond Thailand and rice alone.

Chart 4: Thailand rice production and El Nino weather conditions

AI optimism Inflationary risks continue to build, whether from elevated oil prices linked to the Strait of Hormuz closure, the prospect of weaker crop yields, or other factors. Yet the tug-of-war between inflation concerns on one side and AI optimism on the other remains ongoing. In some Asian equity markets, notably South Korea and Taiwan, AI-driven enthusiasm has fuelled substantial capital gains, lifting overall market capitalisation to levels that have already surpassed those of several major markets, including Germany’s (chart 5). Much of this rise has been driven by capital appreciation alone, underscoring the sheer scale of the current AI-driven rally and highlighting its potential macroeconomic implications, including possible wealth effects on consumption and investment.

Chart 5: South Korea, Taiwan, and Germany market capitalisation

Nor are the benefits of AI-driven optimism confined to the sector’s largest players and producers. Other parts of Asia, including Southeast Asia, are also benefiting from the ongoing AI investment cycle and infrastructure buildout. As shown in chart 6, Thailand’s Board of Investment recorded a sharp increase in approved foreign direct investment (FDI) last year, driven primarily by digital industries. These investments were concentrated in areas such as data centres and cloud services, underscoring Thailand’s efforts to expand its AI-related infrastructure and increase its exposure to a rapidly growing sector. Notably, investment approvals in digital industries far exceeded those directed towards most other sectors. Thailand is not alone in this regard. Similar AI-related infrastructure buildouts are underway, albeit at different scales and stages of development, across several Southeast Asian economies, including Singapore, Malaysia, and Vietnam.

Chart 6: Thailand approved FDI applications

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief