Asia| Jan 19 2026

Asia| Jan 19 2026Economic Letter from Asia: Shifting Gears

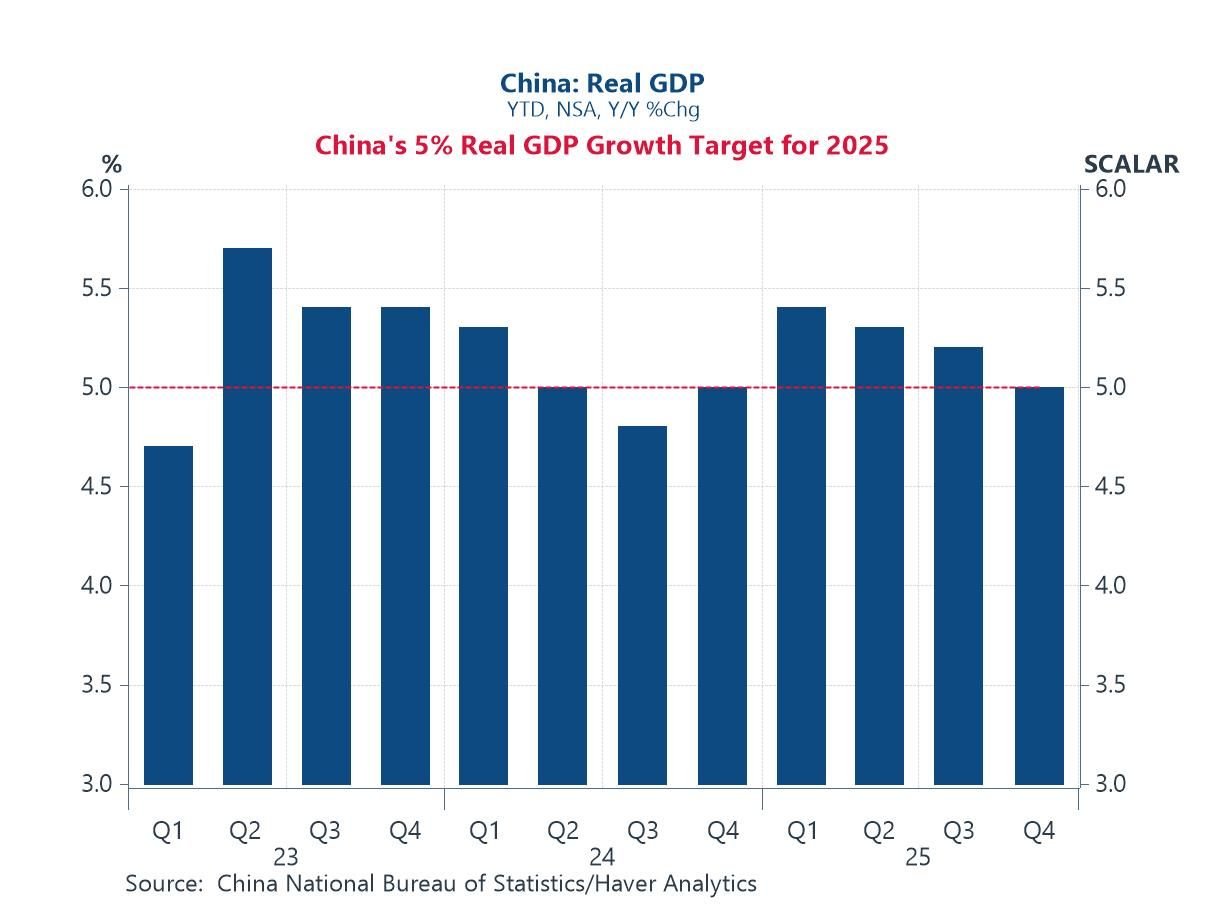

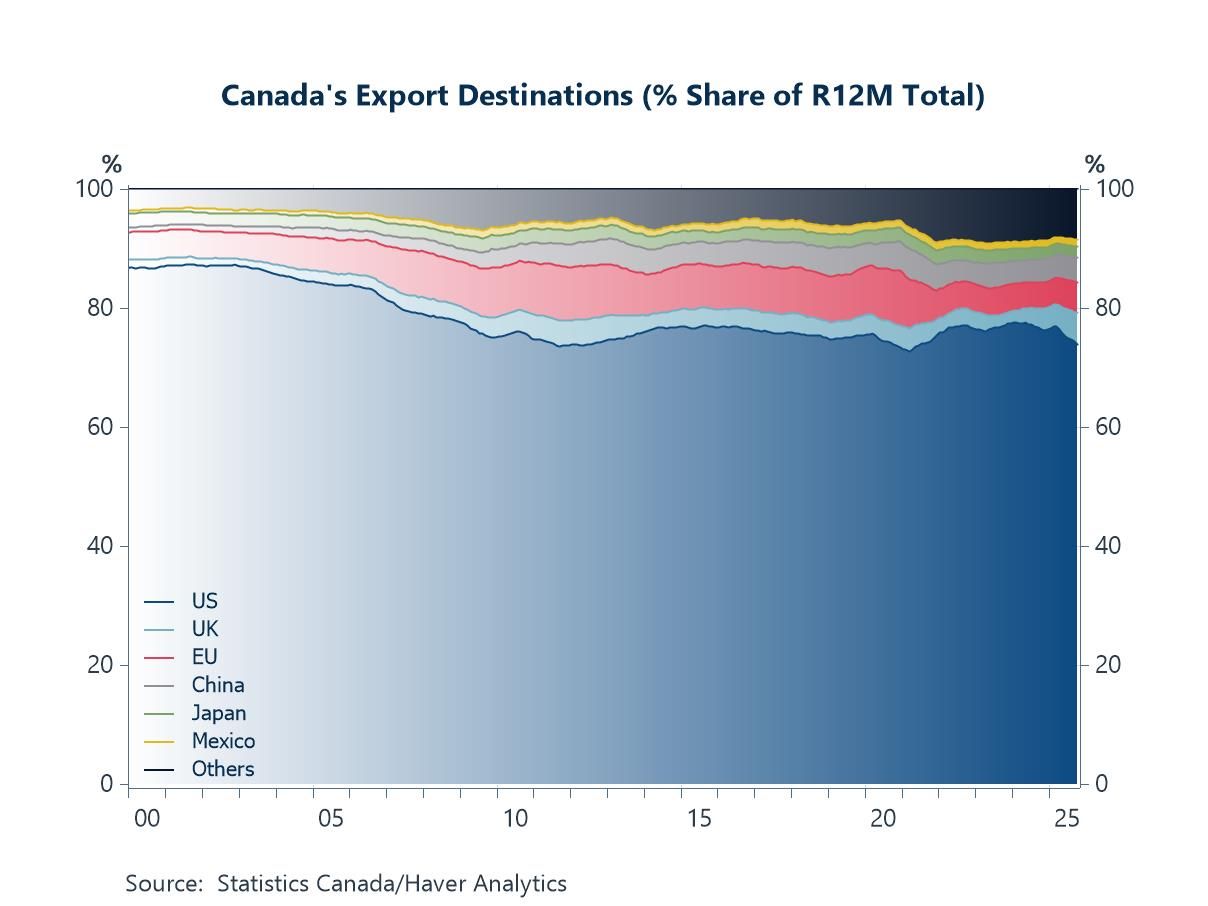

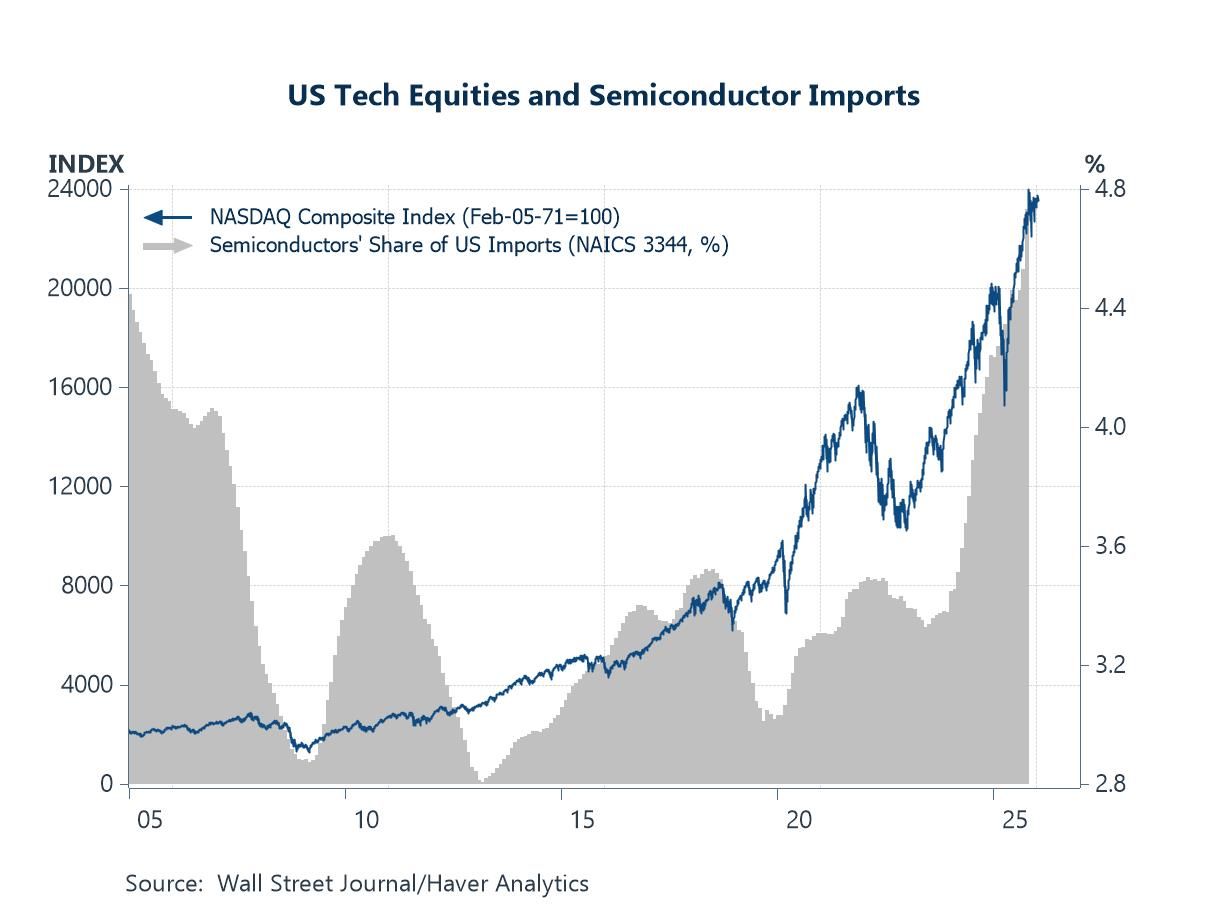

This week, we dive into several key developments across Asia. China’s Q4 GDP marked a further extension of its recent growth slowdown, yet full-year growth still came in exactly at the government’s 5% target for 2025 (chart 1). That said, the road ahead remains challenging, as December’s data delivered a mixed set of outcomes. Encouragingly, new external inroads, starting with Canada’s opening up of EV trade with China, could pave the way for additional opportunities (chart 2). In semiconductors, the latest US tariff measures proved far more limited in scope than initially feared, helping to explain the muted market reaction to the announcement (chart 3). Relatedly, commitments by major Taiwanese chipmakers to expand investment in the US have brought Washington and its largest chip supplier closer together, culminating in a US–Taiwan trade deal (chart 4).

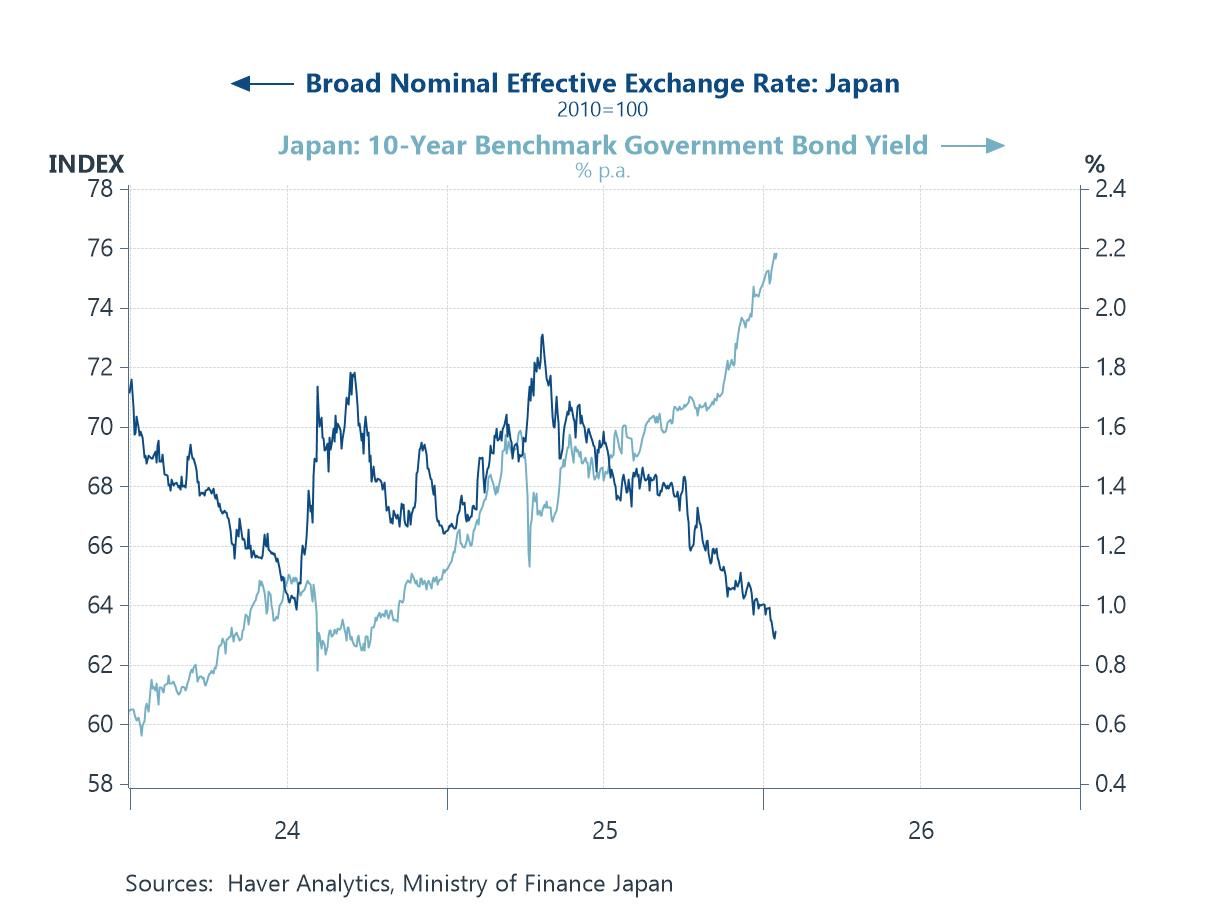

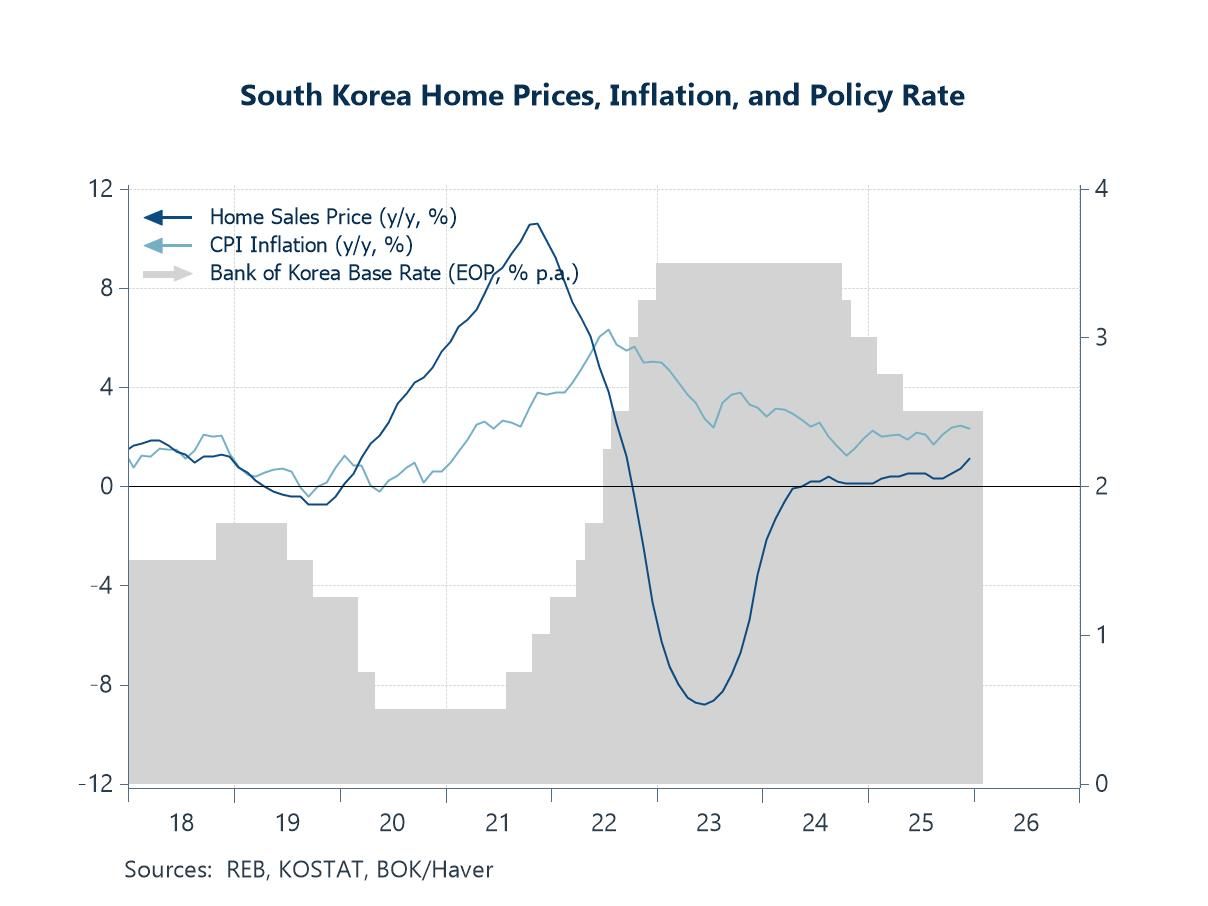

In Japan, attention has turned to the possibility of a snap Lower House election in February. The interim political uncertainty, alongside expectations around future policy, has weighed on the yen and pushed Japanese yields higher (chart 5), with some observers increasingly concerned about the narrowing window to pass the FY2026 budget by April, given the likely dissolution of the Lower House. In South Korea, President Lee’s recent visits to China and Japan point to improving bilateral ties, although he continues to navigate a delicate balancing act amid still-elevated China–Japan tensions. Domestically, elevated house prices and high household debt continue to limit the scope for further monetary policy easing (chart 6).

China Alongside its regular slate of monthly economic releases, China unveiled its Q4 GDP figures earlier today, with the economy expanding by 4.5% y/y during the quarter. While Q4 growth continues the recent trend of deceleration seen over the past few quarters, the outcome brings China’s full-year growth for 2025 right in line with the government’s 5% target (chart 1). This defied expectations among some investors that the economy would fall short. This outcome aligns with earlier discussions that China remained within reach of its growth target despite slowing momentum. That said, the outlook ahead remains challenging. December’s monthly data painted a mixed picture, with declines in fixed asset investment accelerating and retail sales growth cooling further, even as industrial production growth remained relatively resilient.

Chart 1: China’s real GDP growth

On China’s external developments, another high-profile outcome followed Canadian Prime Minister Carney’s visit to Beijing. Canada and China unveiled a trade deal lowering tariffs on Canada’s imports of 49,000 Chinese EVs to 6.1% from 100%, in exchange for China easing tariffs on Canadian agricultural products. Carney remarked that China is now a “more predictable” trading partner than the US and that “a new world order” is taking hold. These comments likely reflect longstanding trade frictions between the US and Canada, as US President Trump has sought to renegotiate what he views as unfair trade arrangements. The new Canada–China agreement is also expected to catalyse significant Chinese joint-venture investment in Canada over the coming years. The move marks a notable shift for Canada, which has traditionally been an exceptionally close partner of the US, not only economically (chart 2). That Ottawa has inked a trade deal with Beijing while US–China tensions remain elevated represents a clear break from its previous stance and has, unsurprisingly, drawn criticism from Washington.

Chart 2: Canada’s export destinations

US semiconductor tariffs Turning to US-originated developments, President Trump signed a proclamation last week imposing a 25% tariff on certain advanced computing chips, including Nvidia’s H200 and AMD’s MI325X. The tariff will not apply to chips imported to support the buildout of the US tech supply chain or to strengthen domestic manufacturing capacity for semiconductor derivatives. The move stops short of a blanket tariff on all AI chips and semiconductor imports, easing—at least for now—initial investor concerns and likely explaining the market’s relatively muted reaction to the announcement (chart 3). A broader tariff would have had far more severe implications, given the US economy’s substantial imports of semiconductor goods. In the case of Nvidia’s H200—designed to comply with US export restrictions and primarily targeted at the Chinese market—the tariff appears intended to capture a 25% levy before the chips are shipped onward to China. That said, China’s demand response remains uncertain, particularly as the H200 is reportedly banned in China.

Chart 3: US technology equities and semiconductor imports

Not long after the tariff announcement, the US and Taiwan — the largest source of US semiconductor imports, as shown in chart 4 — were reported to have reached a trade deal. Under the agreement, Taiwanese chipmakers such as TSMC that expand production in the US will face lower tariffs on semiconductors and related manufacturing equipment, with duty-free treatment applying to some imports. In addition, tariffs on most other Taiwanese exports to the US will be reduced to 15% from 20%. In return, Taiwanese companies will invest $250 billion in the US, including an expanded manufacturing footprint by TSMC in Arizona, aimed at boosting domestic production of semiconductors, energy, and AI. As illustrated in chart 4, Taiwan already dominates US semiconductor imports, with its share having risen sharply in recent years and far outstripping contributions from other major suppliers such as Southeast Asian economies and South Korea.

Chart 4: US semiconductor imports by economy

Japan snap elections Turning to Japan, the country is drumming up for an anticipated February Lower House snap election as Prime Minister Takaichi looks poised to capitalize on her strong approval ratings to secure a firmer parliamentary footing. In reaction, opposition parties have already started galvanizing for the expected upcoming electoral fight, with the opposition Constitutional Democratic Party (CDP) and the ruling party’s former coalition partner, Komeito, having announced a plan to form a new Centrist Reform Alliance (CRA) to fight the current ruling bloc. Given this interim bout of uncertainty, there is now some doubt cast on whether Japan’s budget this year can be debated robustly and passed in time by April 2026 (when the new fiscal year starts), especially if the Lower House gets dissolved soon, meaning less parliamentary time will be available for the purpose. Tracking such developments, the yen had extended its recent slide, whilst Japanese yields have firmed further (chart 5).

Chart 5: Japanese yen and yields

South Korea Lastly, we turn to South Korea, where President Lee has embarked on visits to China and Japan that point to a warming of regional ties. In China, Lee’s meeting with President Xi yielded agreements to restore strategic dialogue channels and deepen cooperation in areas such as critical minerals, with Lee calling for a “full restoration” of bilateral relations. In Japan, his visit similarly signalled a thaw in ties following previous periods of tension. Overall, South Korea appears to be seeking closer relations with its two major Asian neighbours even as China–Japan tensions remain elevated. Domestically, however, while the semiconductor sector has benefited from the AI-driven upswing, South Korea continues to face challenges such as elevated house prices and high household debt. These factors have constrained the scope for further monetary policy easing (chart 6).

Chart 6: South Korea home sales prices, inflation, and policy rate

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief