Asia| Jun 08 2026

Asia| Jun 08 2026Economic Letter from Asia: Risk Reversal

In this week’s Letter, we take stock of the latest Blue Chip Financial Forecast (BCFF) survey results and connect them with recent regional developments across Asia. Panellists have raised their policy rate forecasts relative to the pre–Middle East conflict baseline (chart 1), as inflation concerns intensify and several Asian central banks tighten policy (chart 2). Meanwhile, stronger US jobs data have strengthened the higher-for-longer rate narrative, tempering AI-driven equity gains in the US and Asia (chart 3).

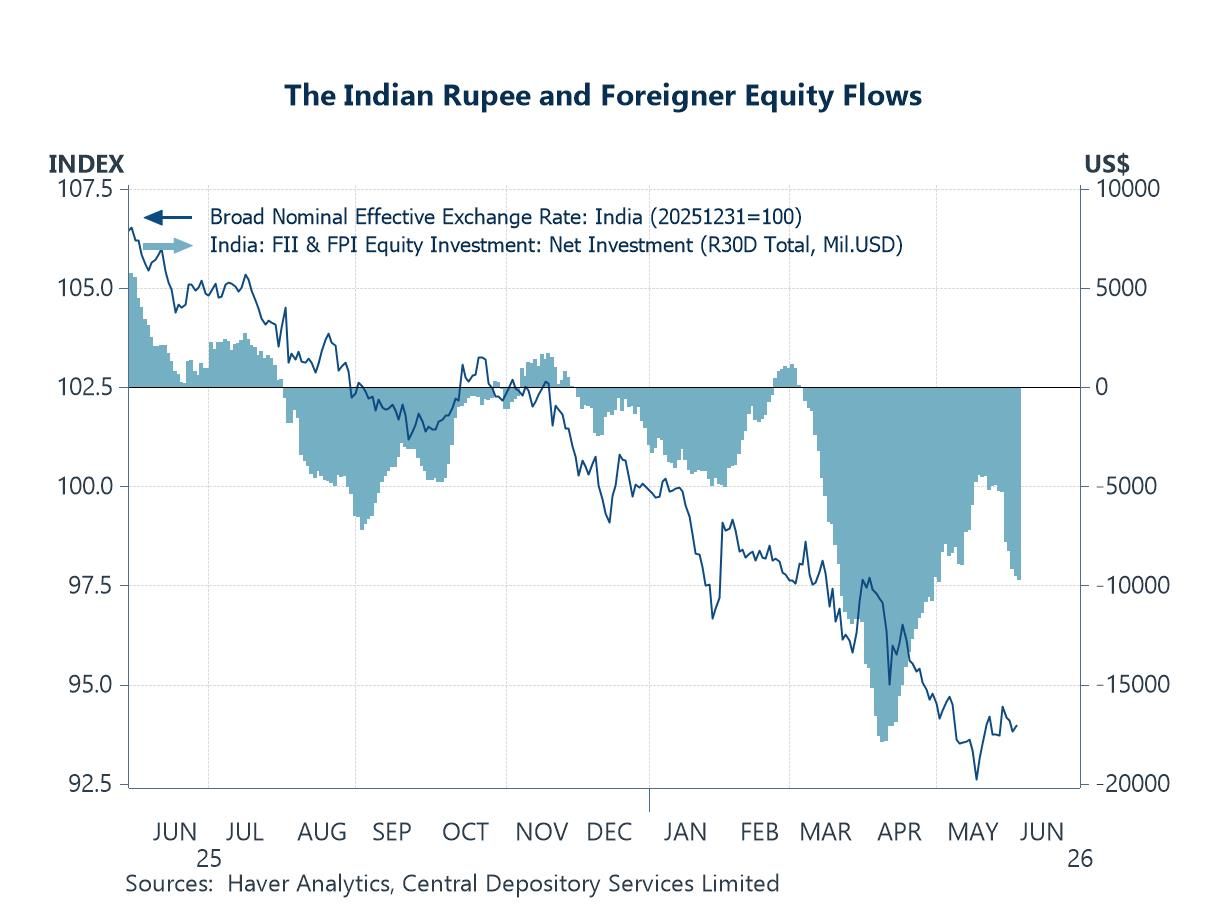

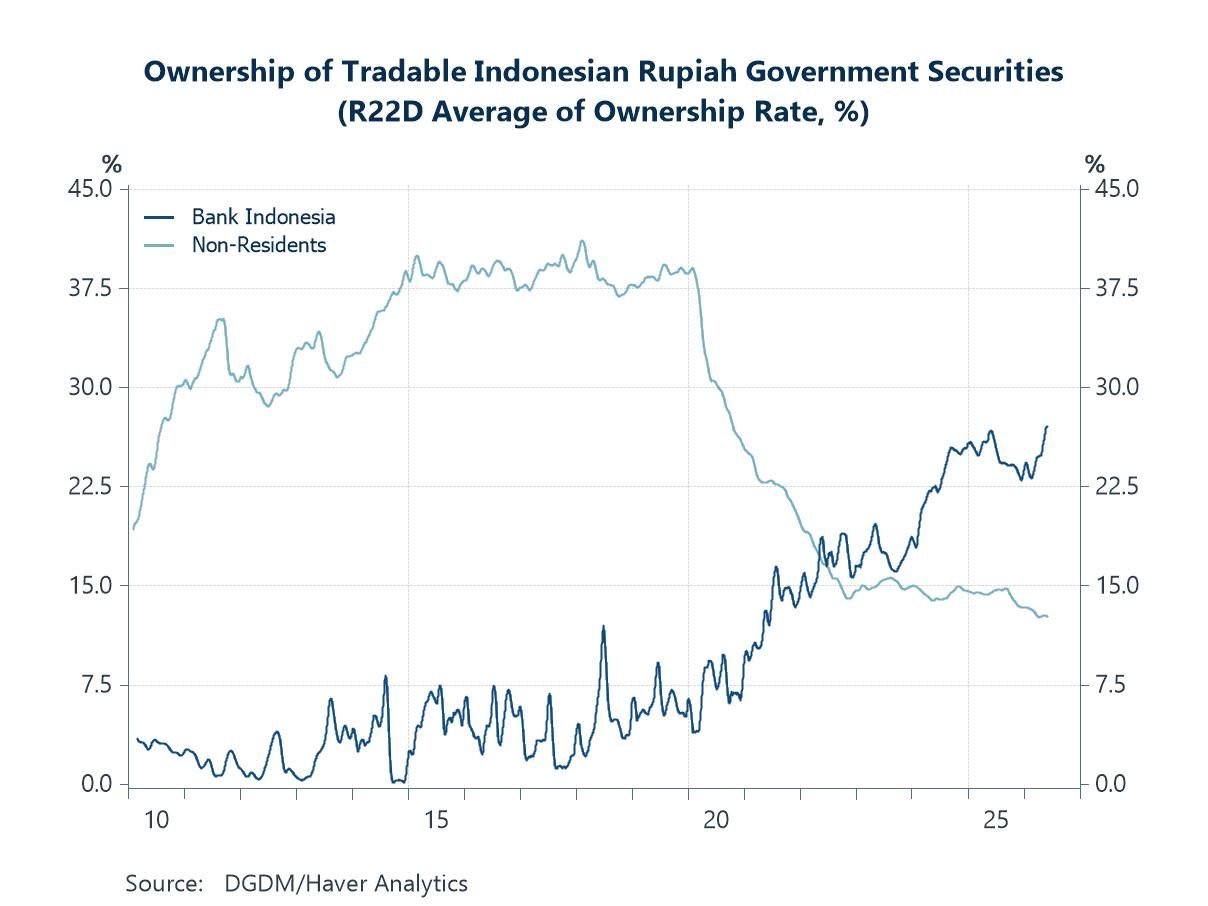

Turning to country specifics, the sharp rise in South Korean equities masks a more nuanced picture, where sustained foreign investor outflows have eventually weighed on the market and contributed to weakness in the South Korean won (chart 4). India has experienced a similar pattern, with a range of rupee supportive measures already introduced, although their effectiveness remains too early to assess (chart 5). Indonesia has likewise seen persistent foreign capital outflows alongside a weakening rupiah, with foreign participation in its government bond market declining to a worrying trickle (chart 6).

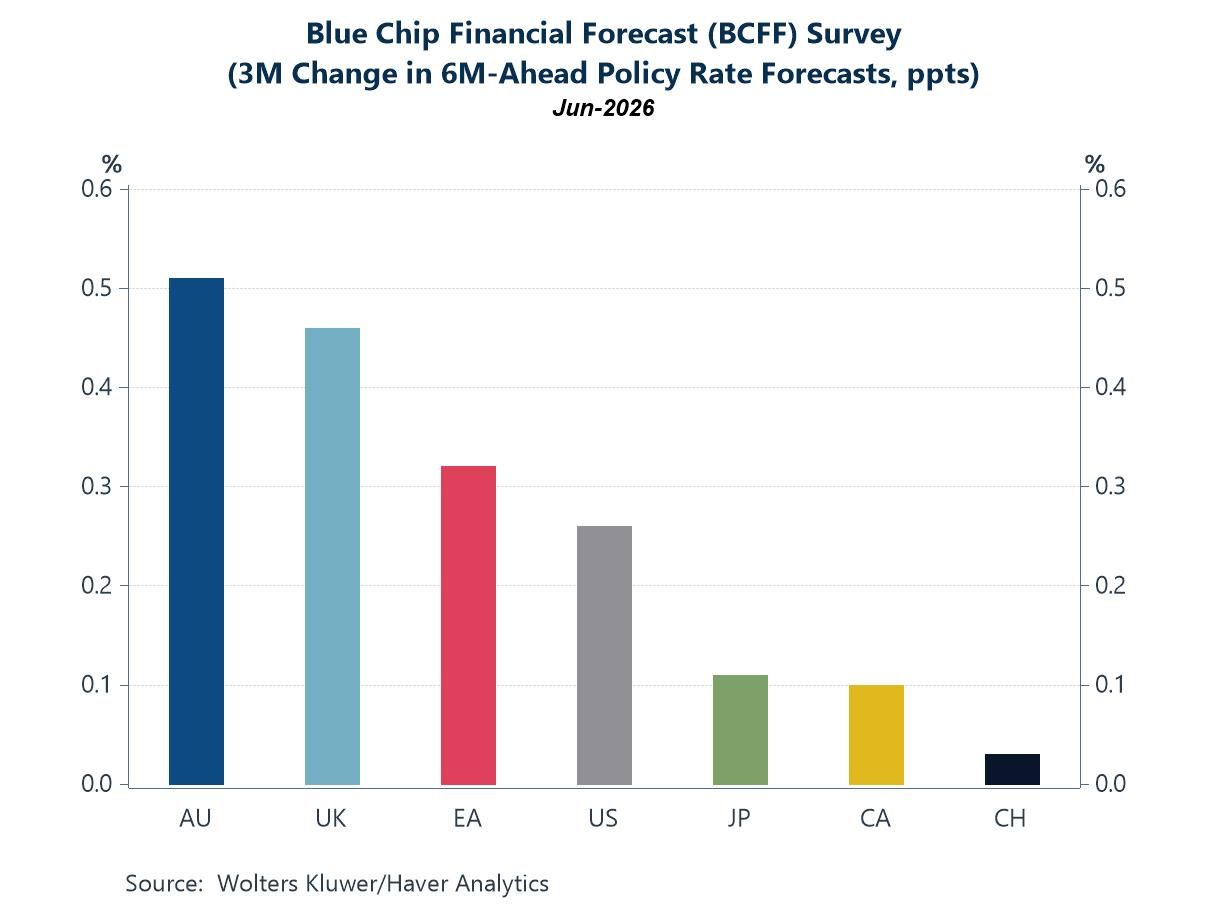

Blue Chip Financial Forecast (BCFF) survey Looking at the latest Blue Chip Financial Forecast (BCFF) survey results, chart 1 shows that panellists have significantly revised upward their policy rate forecasts since the March survey (conducted at the end of February), reflecting the inflationary implications of the ongoing conflict in the Middle East and the continued closure of the Strait of Hormuz. Such revisions are understandable, as the disruption to one of the world's most important oil shipping routes has constrained global oil supply. With supply reduced while demand remains broadly unchanged, oil prices have risen sharply, feeding through to higher inflation and increasing the likelihood of further monetary policy tightening, or at the very least, a slower pace of policy easing. Among the economies covered by the survey, panellists have revised up their policy rate expectations for Australia by the largest margin, followed by the United Kingdom and the euro area.

Chart 1: Blue Chip Financial Forecasts – Policy Rates

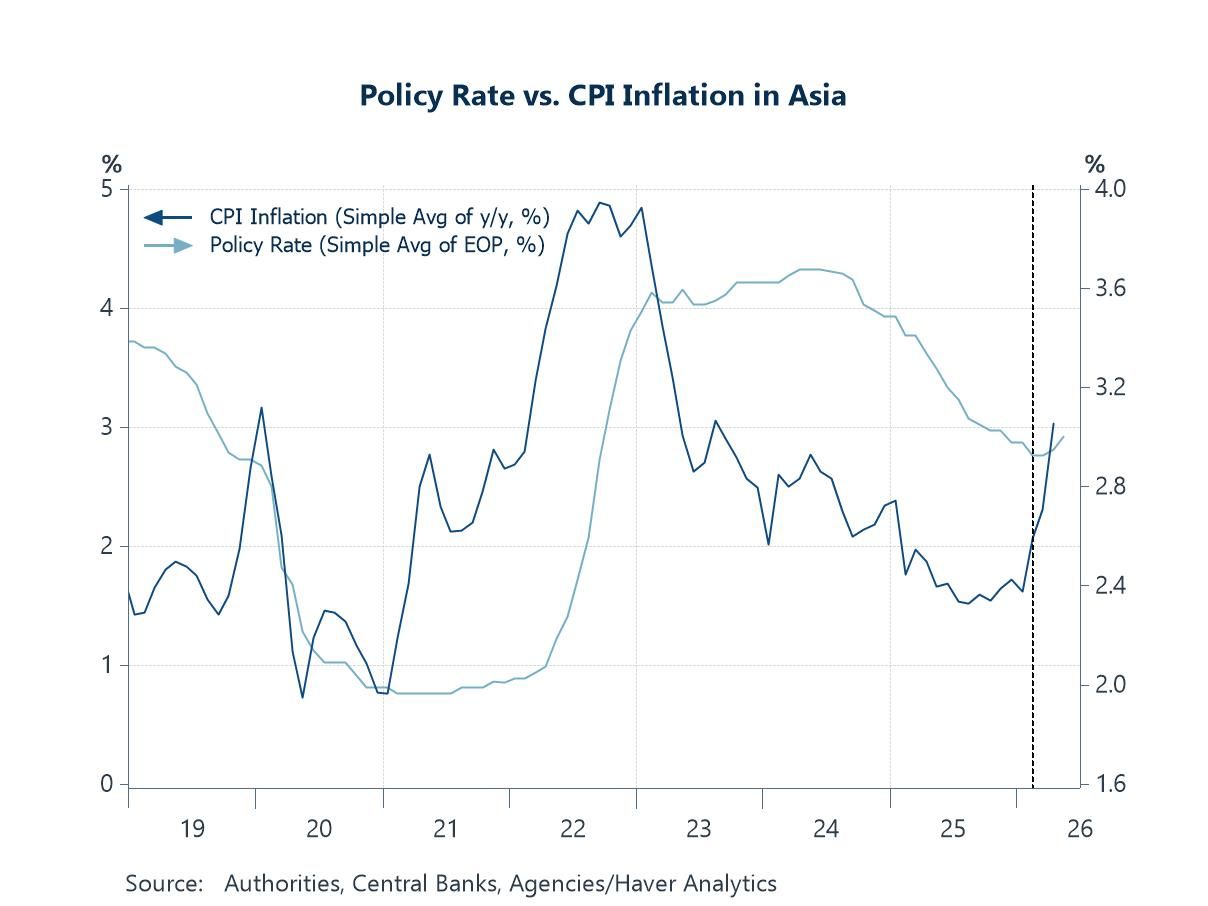

Sure enough, these higher policy rate expectations have largely been borne out across Asia, where inflation has accelerated alongside rising oil prices, prompting many regional central banks to tighten monetary policy in an effort to contain price pressures (chart 2). Moreover, while reports of an imminent US-Iran peace agreement and the reopening of the Strait of Hormuz have surfaced repeatedly, the reality remains quite different. Shipping traffic through the Strait continues to be severely constrained, leaving global oil supplies under significant strain and keeping upward pressure on energy prices. Looking ahead, further inflation signals will emerge from this week's inflation releases in China and India. Should inflation continue to accelerate, regional central banks are likely to face increasing pressure to tighten monetary policy further rather than maintain a more growth supportive stance.

Chart 2: Asia average CPI inflation and policy rate

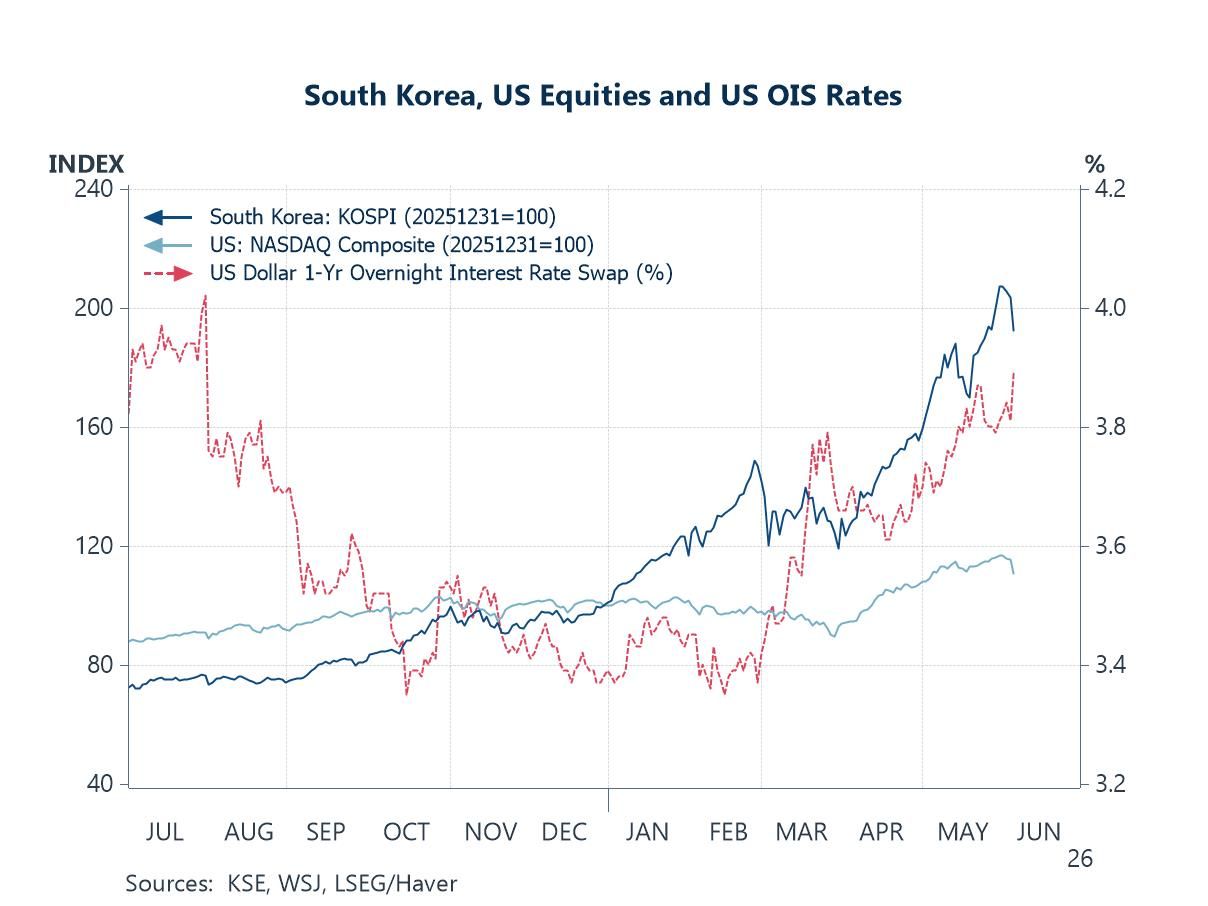

Rate hike prospects and market sentiment Just last week, stronger-than-expected US employment data prompted investors to raise the probability of further Federal Reserve tightening, taking some of the shine off the AI-driven rally in global equities. The increased prospect of further US policy tightening, reflected in higher US dollar overnight index swap rates (chart 3), has since weighed on market sentiment and dampened risk appetite in recent days. That said, equity rallies rarely proceed uninterrupted, and interim bouts of profit taking are a natural feature of financial markets, with major news events often serving as the catalyst. The softer market sentiment has also spilled over into Asian markets, as evidenced by the pullback in South Korean equities, although country specific factors have also played an important role.

Chart 3: South Korea & US equities and US OIS rates

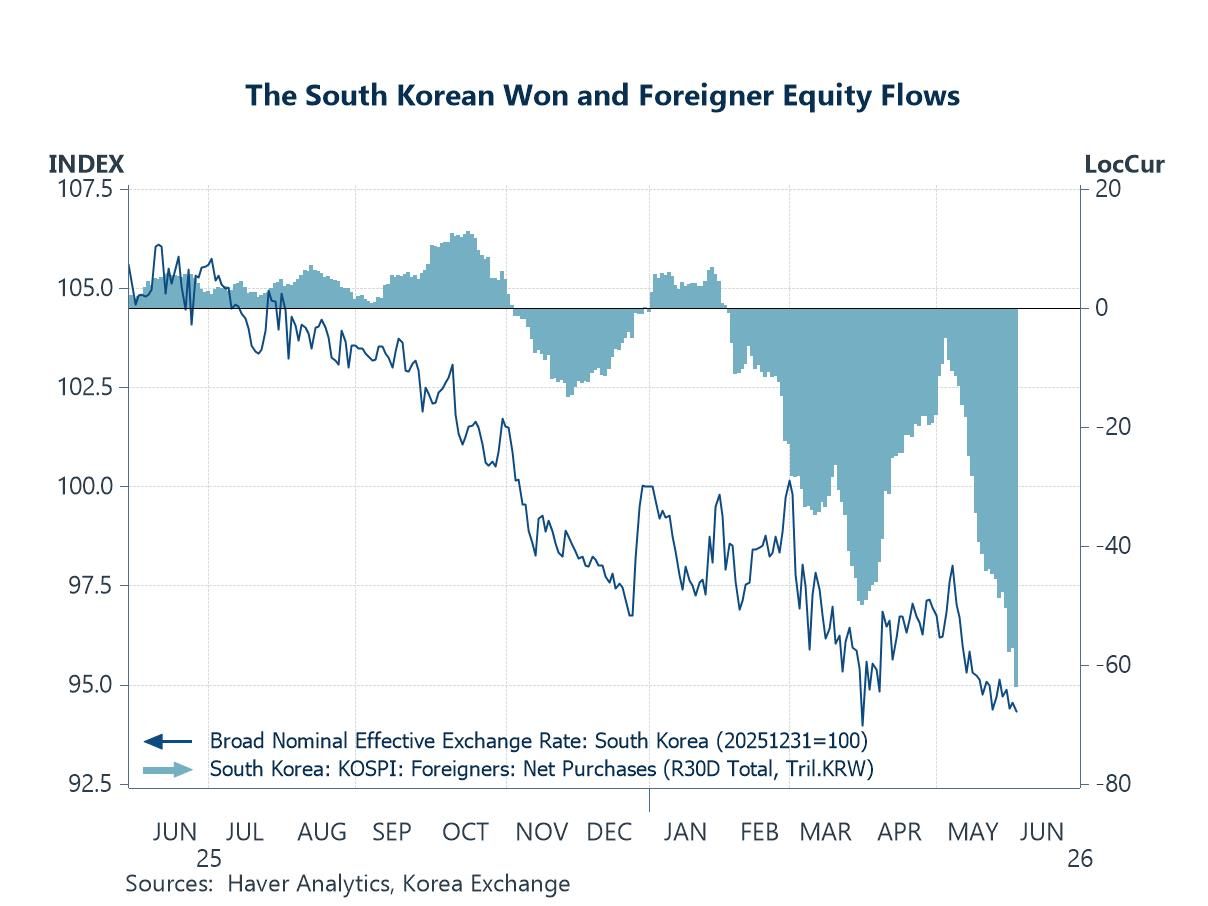

South Korea There is, however, a disconnect between the meteoric rise in South Korean equities this year and the persistent depreciation of the South Korean won (chart 4). In many economies with significant foreign investor participation in equity markets, rising stock prices are often accompanied by some degree of domestic currency appreciation. A closer look at South Korea's equity flow data, however, reveals a different story: foreign investors have been net sellers of South Korean equities, partly explaining the won's continued weakness, while domestic individuals, together with financial investment firms, have accounted for the bulk of net purchases this year. The sustained outflow of foreign capital likely reflects several factors, including a broader risk-off environment following the outbreak of the Middle East conflict and the erosion of currency-adjusted equity returns caused by won depreciation. The latter, in turn, creates a feedback loop, as currency weakness further discourages foreign inflows and reinforces downward pressure on the won.

Chart 4: South Korean won and foreigner equity flows

India India has been experiencing a similar dynamic, with persistent foreign equity outflows weighing heavily on the rupee (chart 5) and prompting authorities to intervene to stabilise or support the currency. The initial catalyst for these sustained outflows arguably came from the steep US trade tariffs imposed last year amid the absence of a concrete US–India trade agreement. More recently, the flare-up in the Middle East has added to investor concerns, given India's status as a major oil importer. Higher oil prices increase the country's import bill and, in turn, its demand for foreign currency, placing additional downward pressure on the rupee. While a weaker rupee can provide some support to exports and increase the local currency value of remittances, which are an important source of income given India's large overseas workforce, it also has its drawbacks. A persistent and rapid depreciation of the currency can create broader macroeconomic challenges, particularly for a net importer such as India. In response, the authorities have introduced a range of measures aimed at attracting foreign capital and supporting the rupee, although it will take time to assess their effectiveness. These measures include exempting interest and capital gains on foreign investments in government bonds from tax and expanding the pool of government bonds eligible for unrestricted foreign investment, among others.

Chart 5: Indian rupee and foreigner equity flows

Indonesia Indonesia has been facing a similar dynamic, with foreign investors having substantially unwound their holdings of tradable Indonesian rupiah-denominated government securities. As a result, the foreign ownership share has fallen to below 13%, from a peak of more than 40% before the pandemic (chart 6). This sharp decline reflects both a deterioration in foreign investor sentiment and the rapid expansion in government bond issuance, underscoring the significant funding needs of the current government as it pursues its ambitious policy agenda. In the meantime, a large share of this additional bond supply has been absorbed by Bank Indonesia itself, effectively invoking the concept of seigniorage—the use of central bank money creation to help finance government spending. These persistent foreign investor outflows have also been mirrored in the weakness of the rupiah.

Chart 6: Ownership of tradable rupiah government securities

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief