Asia| May 26 2026

Asia| May 26 2026Economic Letter from Asia: Fiscal Strains

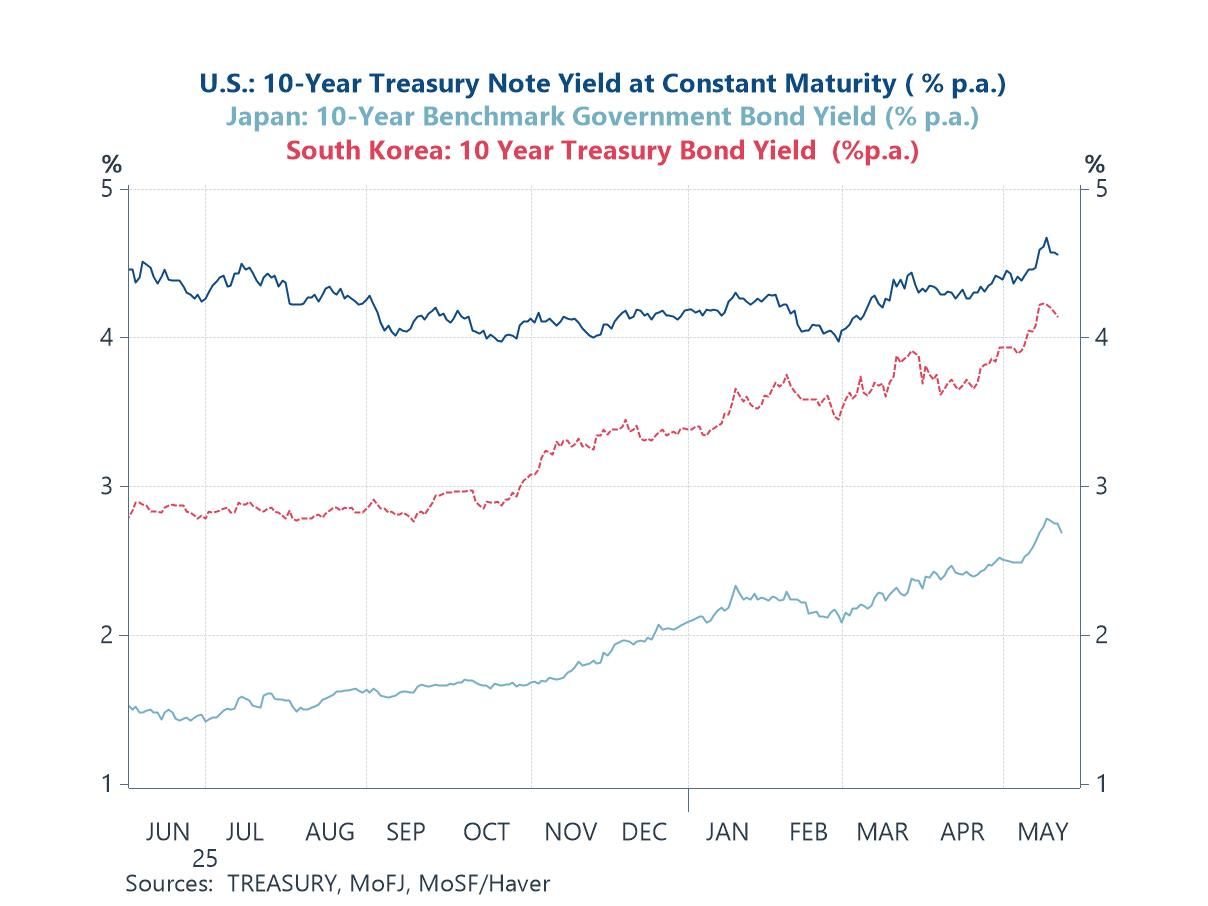

In this week’s Letter, we examine the ongoing Middle East situation through another lens — namely, the fiscal costs it has imposed on Asian economies and the strains that are already beginning to emerge. While the recent surge in bond yields has largely been attributed to inflation-related concerns, yield spikes in some Asian economies have also arguably been driven by fiscal concerns, as governments step up bond issuance to finance support measures (chart 1).

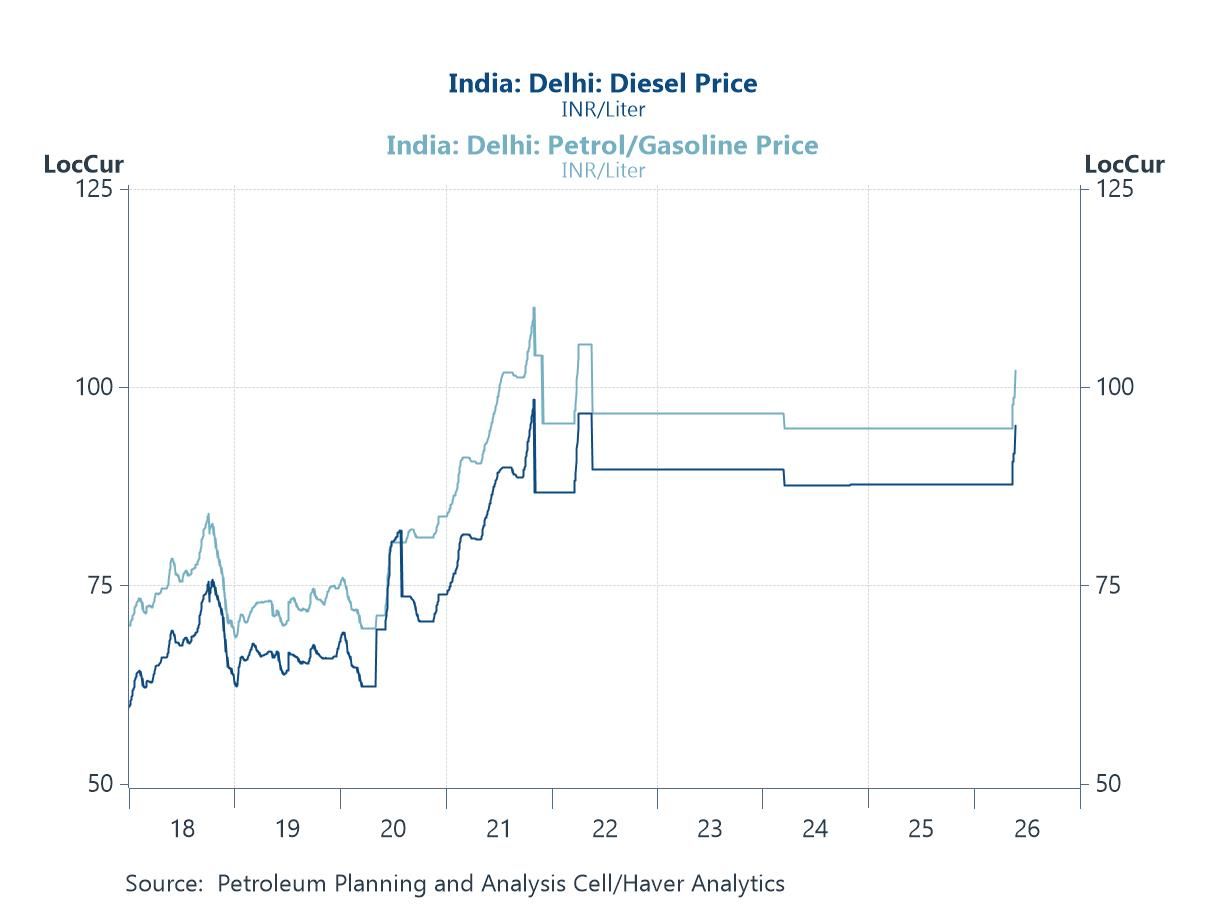

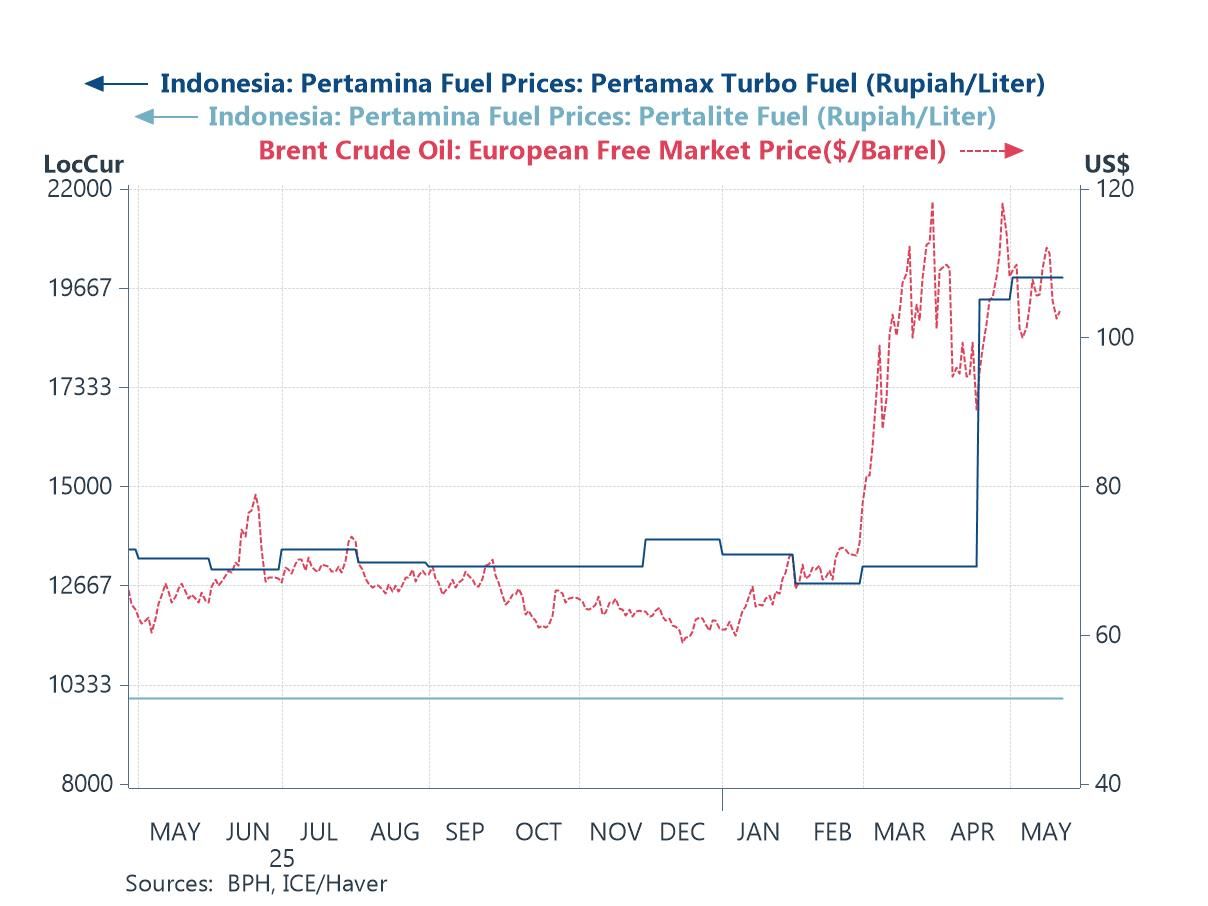

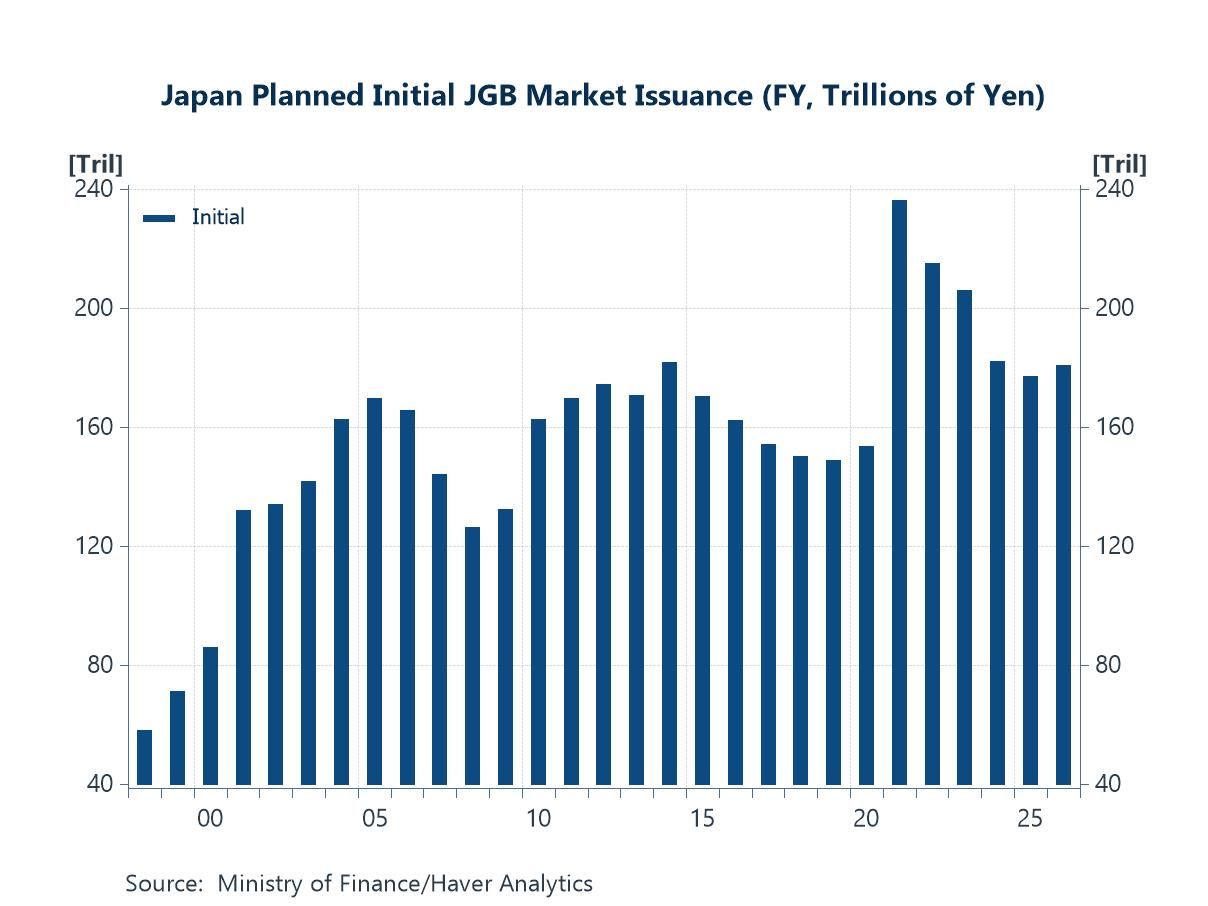

In India, cracks are beginning to show in its fuel subsidy programme, with fuel prices now being raised as previously subsidised rates appear increasingly unsustainable, underscoring the inherently finite nature of such measures (chart 2). While Indonesia continues to hold the line by keeping Pertalite fuel prices unchanged, hikes in more premium fuel grades, coupled with the government’s broader slate of spending initiatives, have left investors increasingly on edge over the country’s fiscal sustainability (chart 3). In Japan, the cabinet is reportedly seeking to put together an additional budget to help cushion inflationary pressures stemming from the Middle East conflict. Although the Prime Minister has sought to allay concerns over additional bond issuance, broader fiscal concerns remain (chart 4).

Against this backdrop of fiscal strain , inflation risks, and geopolitical instability, it is also important to keep in mind the growth-supportive factors still in place across parts of Asia. In particular, the ongoing AI upcycle continues to support exports in several regional economies (chart 5). Taking these crosscurrents into account, we then turn to the week ahead, where central banks will continue to navigate the trade-off between growth and inflation amid a heavy slate of upcoming data releases, particularly across East Asia (chart 6).

Bond markets Global yields have remained elevated, although some pullback has been seen in recent days (chart 1). Inflation-related concerns arising from elevated oil prices linked to the Middle East conflict remain front and centre and are still widely cited as the main driver of the recent spike in nominal yields. However, other factors are also at play, particularly in certain economies. Contributing to the rise in yields in some economies are fiscal concerns. Regarding the US-Iran situation, hopes for a peace deal have once again been raised in recent days, only to be subsequently dampened, underscoring how little concrete progress has ultimately been made. In addition, fresh US strikes on Iranian missile launch sites and boats highlight the continued fragility of the situation. On balance, the world remains stuck in a state of limbo, holding its breath for a positive peace outcome — particularly the reopening of the Strait of Hormuz — while the economic effects of its closure continue to weigh on the global economy.

Chart 1: US, Japan, and South Korea 10-year yields

India Given the fallout from the closure of the Strait of Hormuz and the subsequent surge in energy prices, several Asian governments have scrambled to contain the strain on household expenses through various measures. In turn, the sharp rise in energy costs has also heightened upside risks to inflation. One common and direct approach has been to cap energy prices, effectively subsidising end-consumers against rising costs. However, as mentioned before, while such measures can provide immediate relief, they are rarely sustainable and often come at significant cost. One example is India, which had largely maintained fixed fuel prices until recently, when state-run refiners started to raising prices for the first time in four years (chart 2) amid extremely elevated oil prices. The move highlighted the limits of fuel subsidies, given their increasingly costly nature especially when the gap between subsidised prices and actual market prices remains excessively wide for a prolonged period, ultimately resulting in sustained financial losses.

Chart 2: India fuel prices

Indonesia Indonesia has taken a similar approach in attempting to shield households from volatile oil prices, particularly through its subsidised Pertalite fuel programme. While the government has pledged to keep prices of Pertalite — the country’s most widely used fuel grade — unchanged through 2026, unsubsidised premium fuel grades such as Pertamax Turbo have already undergone multiple rounds of price hikes, rising by roughly 50% so far, broadly in line with the proportional surge in crude oil prices (chart 3). The persistent fiscal burden of such subsidies, coupled with the current administration’s costly policy ambitions — including its free school lunch programme — has brought renewed attention to Indonesia’s near-to-medium-term fiscal health. Such concerns have, in part, already been reflected in the rupiah’s prolonged weakness and credit outlook downgrades by certain ratings agencies, although other contributing factors are also at play. Adding another layer of policy uncertainty is the government’s recent move to centralise control over commodity exports, which, while arguably well-intentioned, leaves significant room for business uncertainty, particularly regarding how such centralisation will ultimately be implemented.

Chart 3: Indonesia fuel and Brent crude oil prices

Japan Turning to Japan, the government is facing similar challenges in balancing economic support measures against mounting fiscal concerns amid the Middle East conflict. Prime Minister Takaichi’s cabinet is reportedly considering an additional budget worth roughly $19 bn to cushion the economic fallout from higher prices stemming from the crisis, with part of the package expected to fund utility and gas subsidies, among other measures. While such policies may help mitigate some of the growth drag arising from the conflict, they also revive longstanding concerns over fiscal sustainability. That said, Takaichi has stated that the supplementary budget will not lead to additional bond issuance, as some issuance planned under last fiscal year’s budget will likely be cancelled following higher-than-expected tax revenues and unspent allocations elsewhere. Nevertheless, fiscal concerns are likely to persist, given that the existing issuance pipeline remains elevated relative to pre-pandemic levels (chart 4).

Chart 4: Japan planned initial JGB market issuance

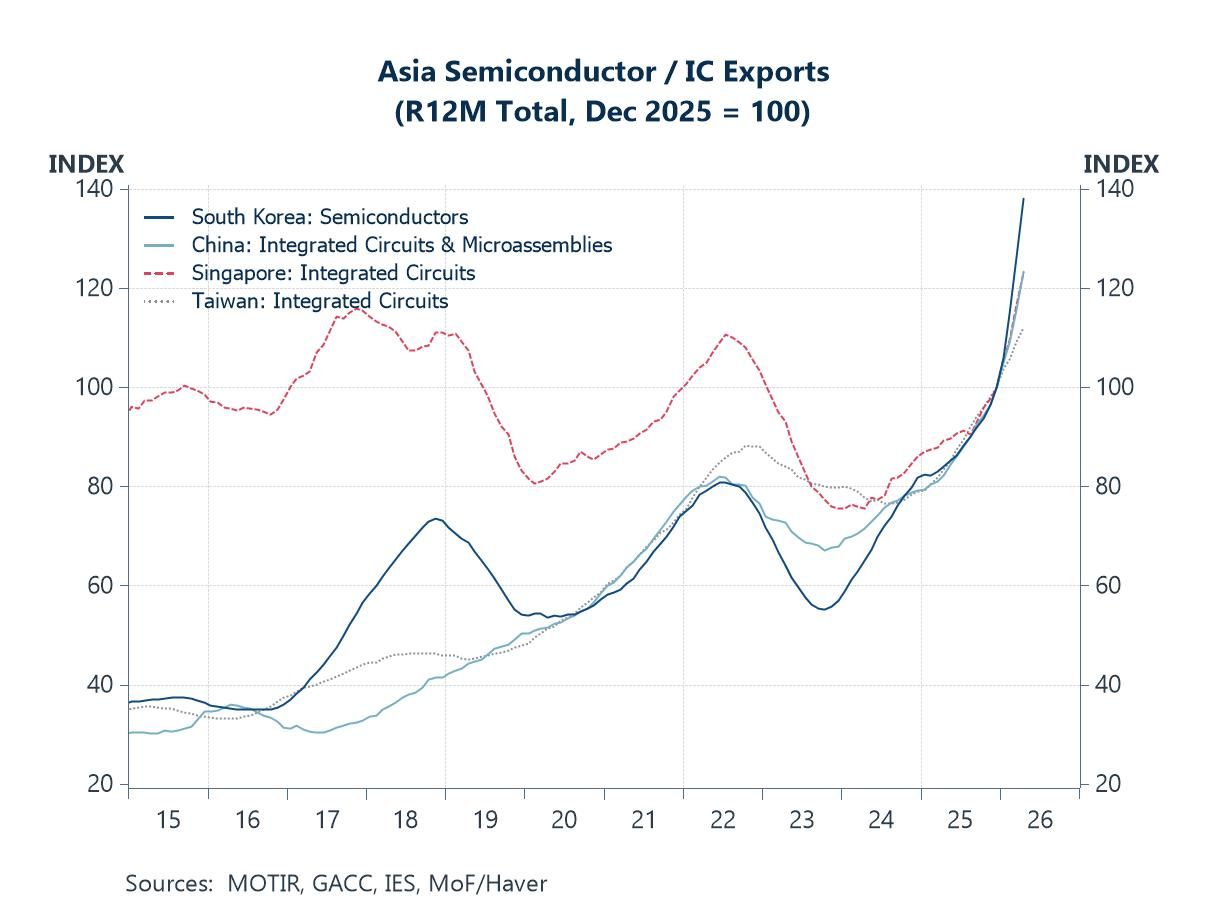

The exports cushion Yet even as the Middle East conflict threatens to impose fiscal strains, lift inflation readings, and push inflation expectations higher, pressure on central banks to maintain tighter monetary policy has also increased. Despite these headwinds, a key driver of growth continues to provide a cushion for several Asian economies in the form of still-robust AI-related demand. Many Asian economies remain well-positioned within the global AI supply chain, allowing them to capture meaningful economic benefits from the ongoing AI investment and buildout cycle. As shown in chart 5, exports of AI-related goods — including semiconductors and integrated circuits — have surged across several Asian economies this year, contributing positively to overall growth as these economies participate in the current AI upcycle. However, this also presents a double-edged dynamic. Economies that become overly reliant on AI-related demand as a primary growth engine may face future vulnerabilities should that demand weaken materially. While the current oil shock has not yet significantly dampened AI-related demand, it remains uncertain whether softer demand for AI goods could eventually emerge as a second- or third-round effect of persistently elevated energy prices.

Chart 5: Asia semiconductor / integrated circuit exports

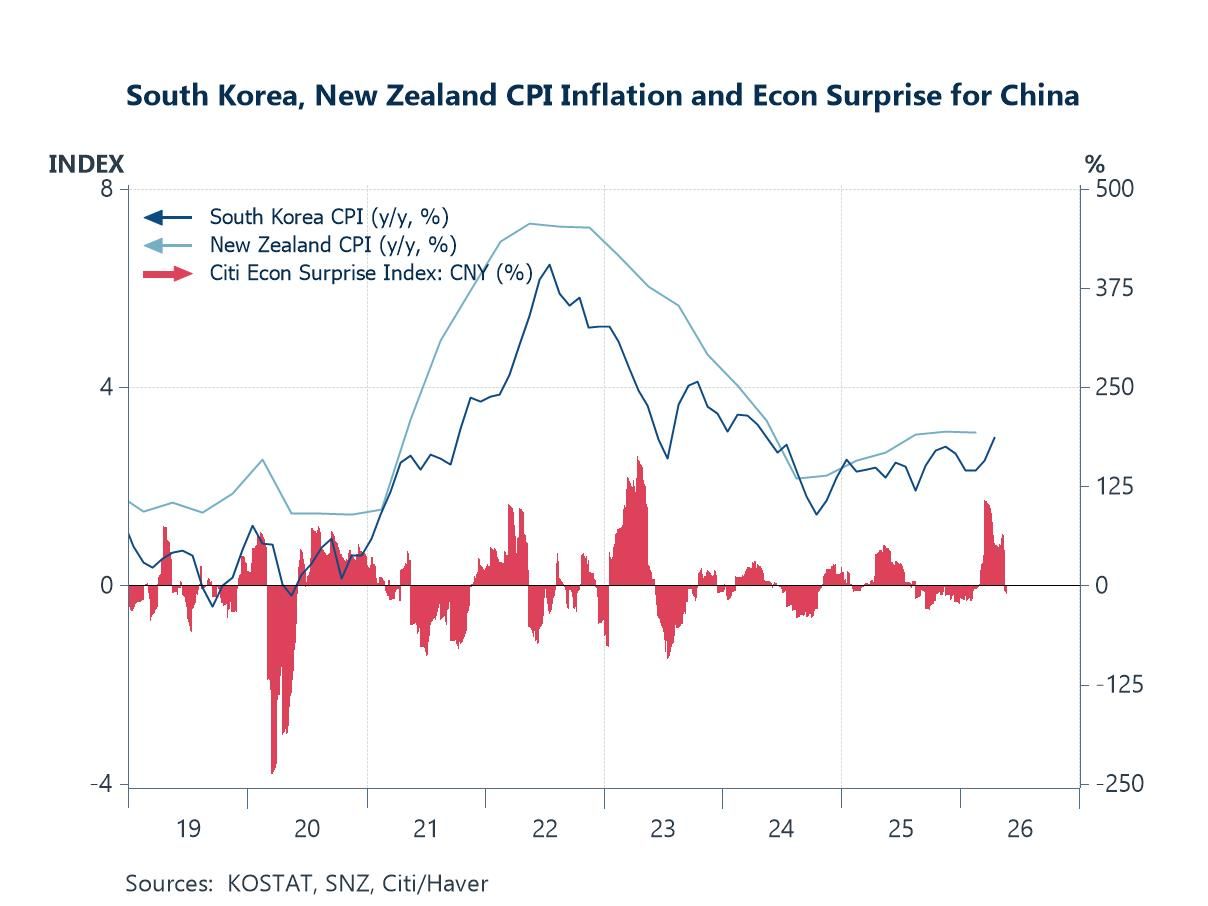

Week ahead Asia faces an exceptionally busy week, with key releases from China and Japan alongside policy decisions from the Bank of Korea and the Reserve Bank of New Zealand. In China, markets will closely watch the official May PMIs and April industrial profits data for signs of whether the recent run of disappointing economic releases is persisting. Japan’s calendar includes industrial production, retail sales, and household spending figures, all of which should provide further insight into the state of domestic demand and broader economic momentum. The week also brings several key interest rate decisions, most notably from New Zealand and South Korea. Like many central banks across Asia, both the Reserve Bank of New Zealand and the Bank of Korea are facing growing pressure to place greater emphasis on upside inflation risks and elevated inflation expectations, even at the potential expense of growth, thereby increasing the case for further policy tightening. Several public holidays across the region may also thin market activity at various points during the week.

Chart 6: South Korea and New Zealand CPI inflation, China economic surprise

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief