Asia| Dec 15 2025

Asia| Dec 15 2025Economic Letter from Asia: Balancing Risks

This week, we assess Asia through a risk lens, given the recent flare-ups across the region. Japan–China tensions, following Japanese Prime Minister Takaichi’s recent remarks on Taiwan, have prompted some retaliatory measures from China, including travel advisories against visiting Japan. This raises the risk of a dent to Japan’s tourism income this year, given the significance of aggregate Chinese tourism expenditure (chart 1), although any such impact would come at a time when Japan is already grappling with the effects of overtourism. Beyond Japan–China relations, investors are also bracing for the Bank of Japan’s (BoJ) final scheduled policy decision of the year, where a rate hike is expected despite Takaichi’s pro-growth fiscal stance. This expectation reflects ongoing yen weakness (chart 2), alongside encouraging results from Japan’s Q3 Tankan survey, among other factors. While the anticipated hike is not, in itself, a risk, the associated increase in financing costs—coupled with the likelihood of higher government bond issuance to support growth objectives—adds to investor concerns.

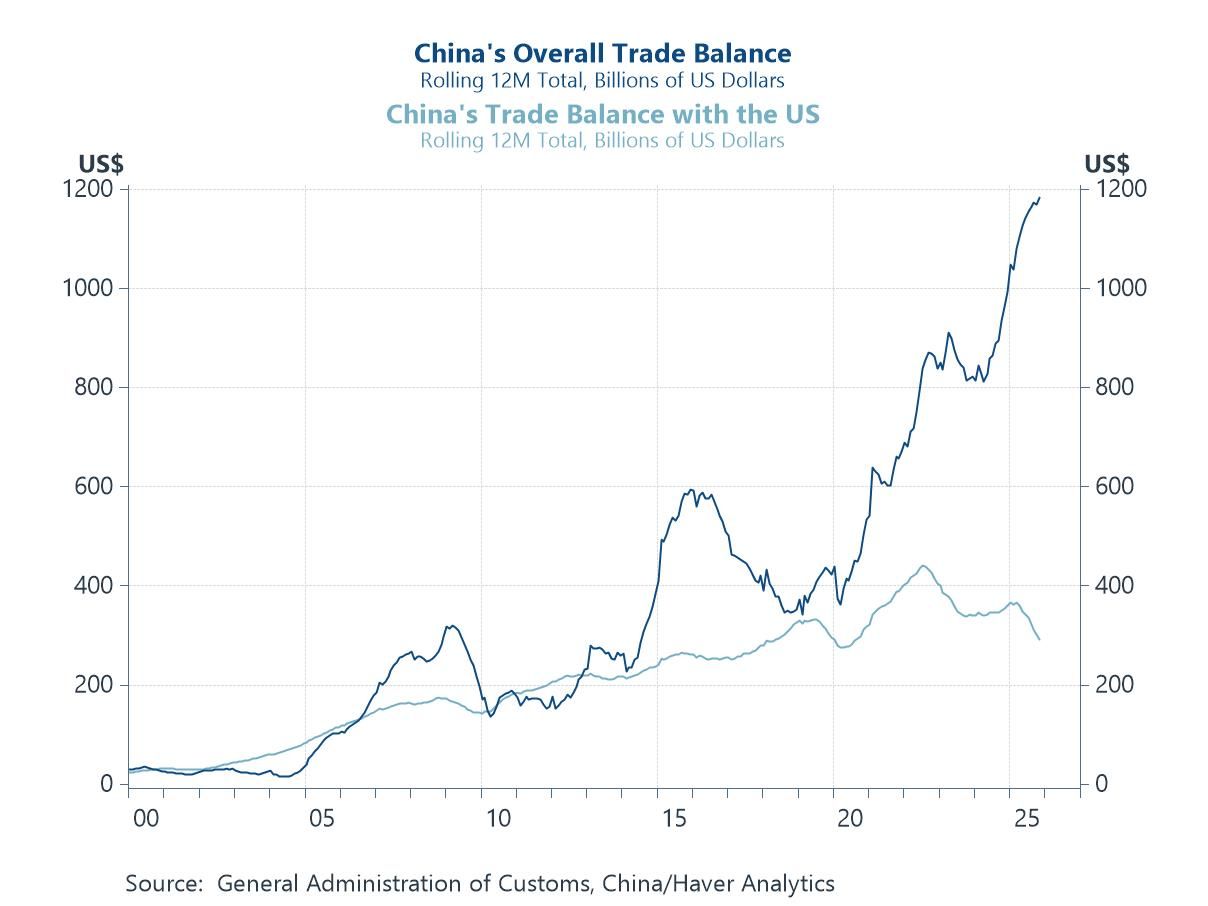

Risks are also evident in China, particularly after the November data docket showed a continued deterioration in growth across multiple sectors (chart 3). While China’s 5% growth target for the year remains within reach, achieving it appears to hinge on a narrow set of growth drivers, notably trade. On this front, China has defied earlier investor concerns to record a substantial widening of its trade surplus this year, despite a worsening bilateral trade balance with the US (chart 4). However, while supportive of growth, this development risks drawing increased pushback from non-US trading partners that have been absorbing China’s excess capacity.

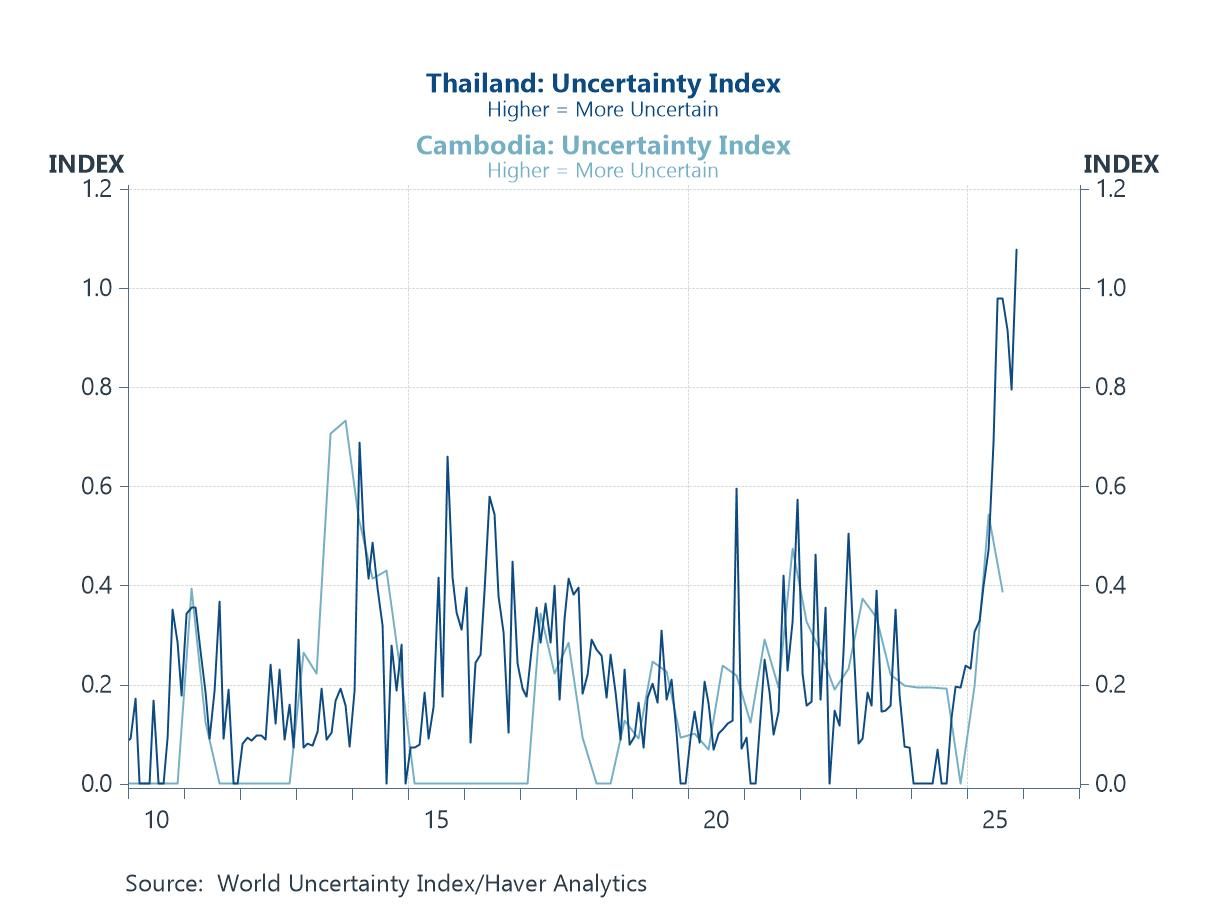

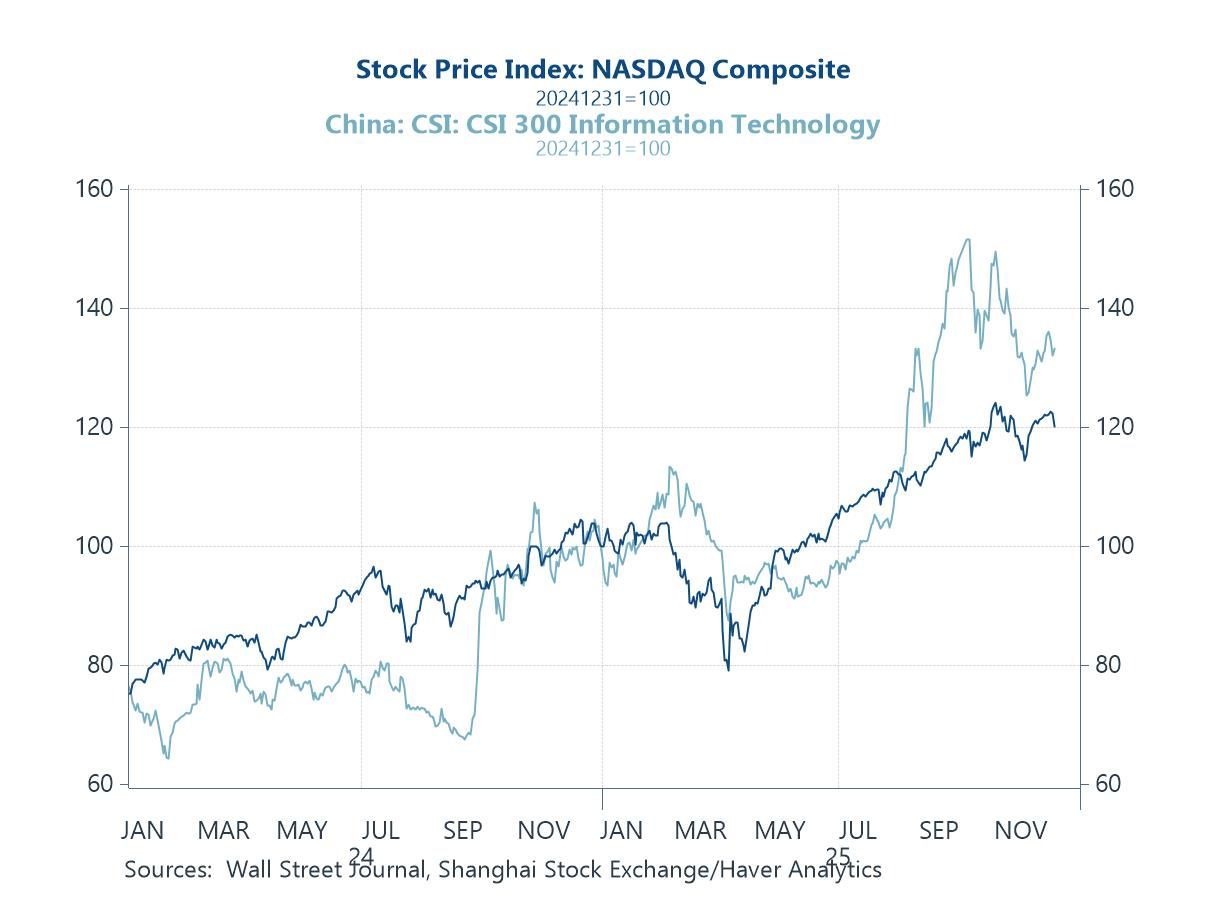

Elevated risks are also present elsewhere in Asia, particularly in Southeast Asia, where renewed military clashes between Thailand and Cambodia have once again pushed bilateral tensions to the fore (chart 5). Thailand additionally faces political uncertainty ahead of early elections, following Prime Minister Anutin’s dissolution of parliament last week. Lastly, we turn to semiconductor- and AI-related risks, which are especially pertinent to Asia given the dominance—and reliance—of Taiwan and South Korea in the sector. A key risk lies in the current extent of market optimism surrounding future AI-related earnings (chart 6), suggesting greater scope for disappointment than for further upside surprises.

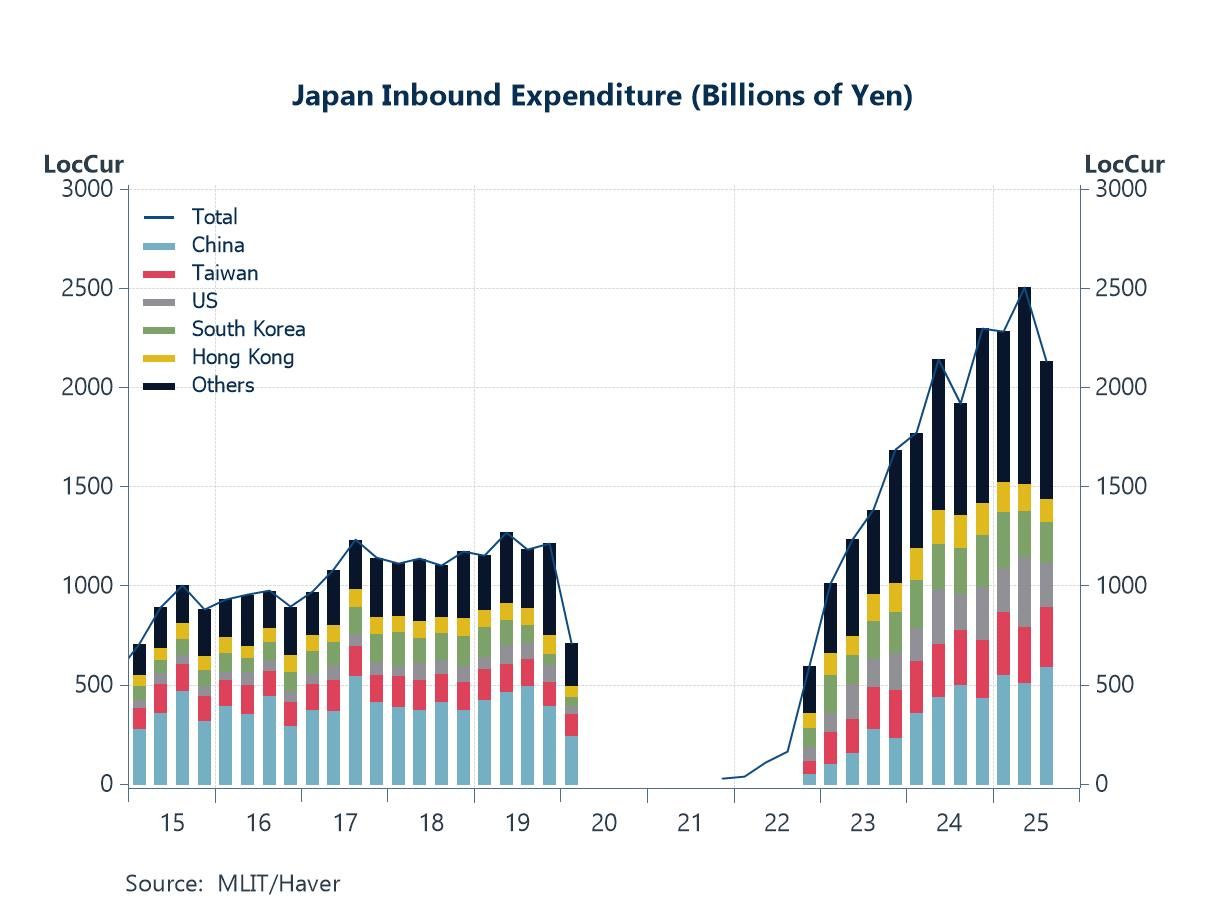

Japan-China tensions Geopolitics will likely remain front and centre in Asia heading into the new year, with several flashpoints carrying the risk of broader regional spillovers. One such case is the recent flare-up in tensions between China and Japan, following new Japanese Prime Minister Takaichi’s parliamentary remarks on Taiwan. Since then, Chinese authorities have rolled out a series of measures — urging Chinese citizens to avoid travelling to or studying in Japan, reinstating an import ban on Japanese seafood, among others. While none of these steps are particularly substantial on their own, they underscore a rapidly deteriorating bilateral dynamic. The economic implications are not trivial. As shown in chart 1, spending by Chinese tourists has historically made up a significant share of Japan’s total inbound tourism receipts — roughly a quarter in recent quarters — with especially strong concentrations in certain regions such as Osaka. Although the absence of Mainland Chinese tourists has been keenly felt since tensions escalated, early indications suggest that increased arrivals from other countries have helped offset some of the shortfall. More recently, a series of close military encounters between China and Japan has further heightened concerns. The risk of miscalculation has grown, raising the possibility of an inadvertent escalation at a time when geopolitical sensitivities in the region are already elevated.

Chart 1: Japan inbound expenditure

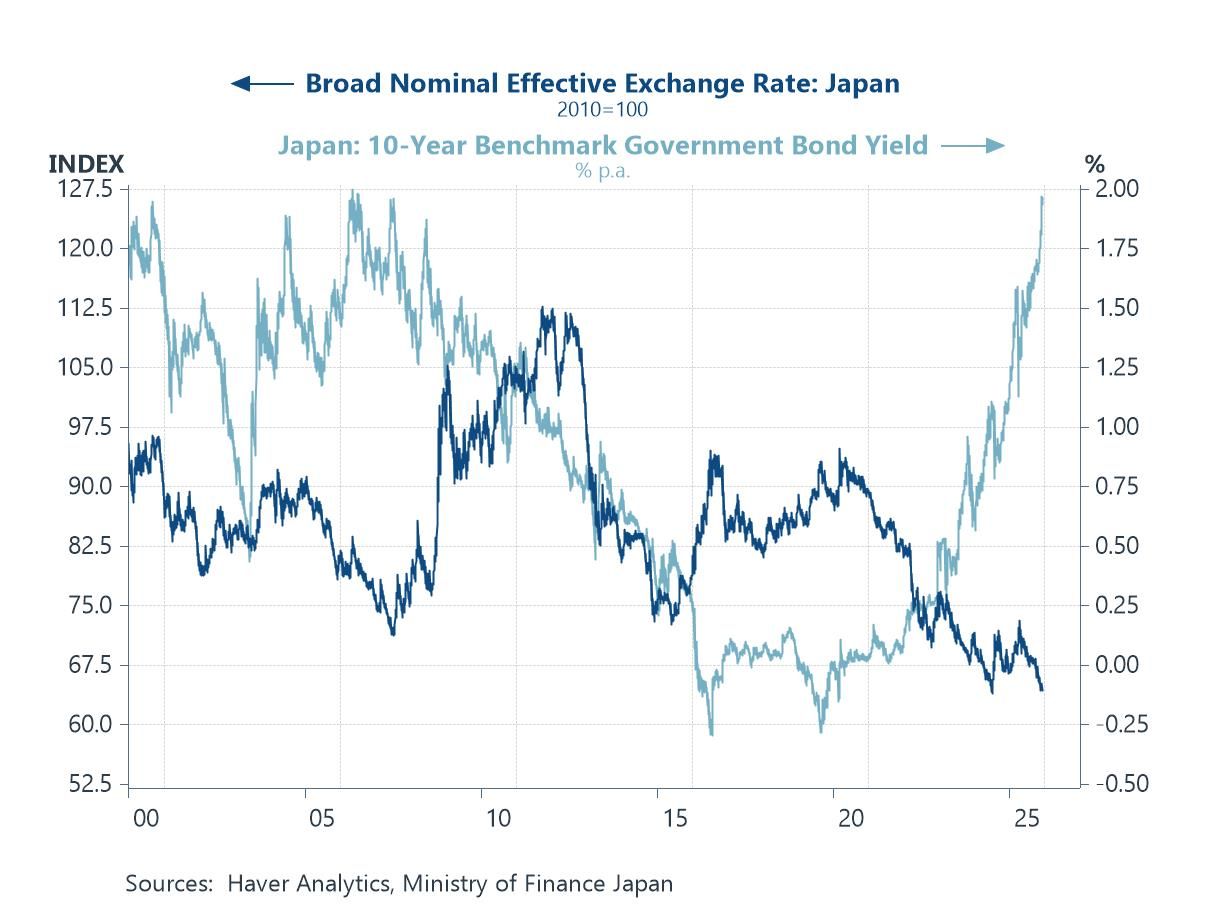

Japan Japan–China tensions aside, investors will also be focused on the Bank of Japan’s upcoming monetary policy meeting this week, the last of the year. After Governor Ueda’s recent remarks, markets are now expecting a 25 bps rate hike. This has been especially evident in the bond market, where yields have risen sharply in recent weeks (chart 2). The move partly reflects expectations of tighter policy, but also concerns Prime Minister Takaichi’s more expansionary fiscal stance. The recently submitted supplementary budget points to increased government bond issuance, adding supply pressure, weighing on bond prices, and pushing yields higher. The rise in yields also poses a risk when combined with increased bond issuance, as this implies higher financing costs for the government. A hike this month is still expected despite the government’s loose fiscal tilt, given yen weakness and recent readings of softer inflation. However, the outlook for any additional tightening beyond December remains uncertain. With the new year approaching and annual spring wage negotiations on the horizon, the BoJ will need further confirmation on wages and inflation before moving again. Meanwhile, the ongoing Japan–China frictions, while not yet generating major economic spillovers, remain a meaningful downside risk. Any material escalation could weigh on Japan’s outlook and complicate the case for further policy tightening.

Chart 2: Japanese yen and yields

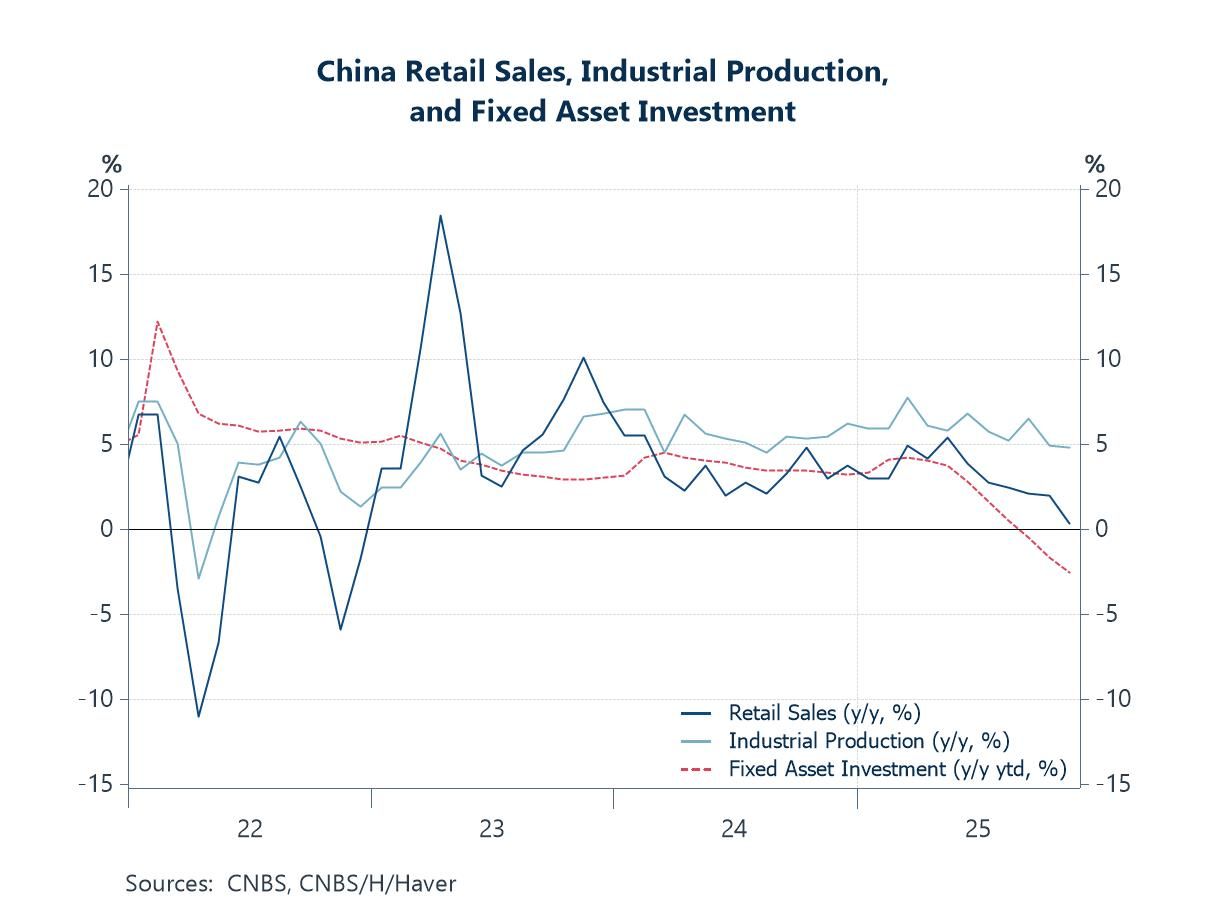

China Moving to China, the latest monthly data point to a broad-based slowdown in growth in November. Year-on-year retail sales growth slowed to its weakest pace since 2022, while year-to-date year-on-year fixed asset investment growth fell to its lowest level since the outbreak of the COVID-19 pandemic in 2020 (chart 3). Industrial production growth also eased, albeit to a lesser extent. In addition, house price declines accelerated, reversing the easing trend seen in previous months. Overall, the latest data extend the pattern of deteriorating growth observed in recent months. That said, it remains to be seen whether the November readings will ultimately cause China to miss its 5% growth target for the year, given the substantial head start accumulated over the first three quarters. Moreover, China has enjoyed a bumper year in trade, which we discuss in the next section.

Chart 3: China retail sales, industrial production, and fixed asset investment

Looking more closely at China’s trade performance, it has become clear that earlier fears of a trade-driven collapse in China’s growth have not materialised. Instead, China’s overall trade surplus has continued to widen, having topped $1 trillion this year, even as its bilateral surplus with the US has fallen sharply (chart 4). This suggests that China’s surplus expansion has been driven by other trading partners, which have effectively been absorbing China’s excess capacity. The stronger-than-expected trade outturn has also been a key factor behind the upward revisions to China’s GDP outlook for the year, with growth still on track to meet the 5% target barring any major setbacks. While this dynamic is not a direct risk in itself, surging exports to these partner economies could become problematic if domestic industries in the receiving countries are unable to absorb the inflow or begin to feel crowded out. Such pressures may eventually provoke a policy response. Still, it remains uncertain whether these countries — many of them smaller economies — would adopt measures similar to those taken by the US, given the asymmetric nature of their economic relationships with China.

Chart 4: China’s goods trade balance

Thailand-Cambodia tensions Moving beyond Japan and China, region-specific tensions elsewhere in Asia also warrant attention, though their broader impact remains limited. Notably, renewed military clashes between Thailand and Cambodia have resurfaced despite an earlier peace deal brokered by Malaysia and the US. While the likelihood of these clashes escalating into a wider regional conflict is low — given their primarily border-specific nature — external pressures on both countries remain a latent risk. The previous ceasefire appeared to have been secured only after US President Trump threatened to withhold trade deals unless fighting ceased, suggesting that a similar “carrot-and-stick” approach may be used again to encourage another ceasefire, although nothing is certain. Domestically, Thailand faces additional near-term uncertainties. Prime Minister Anutin must contend with a range of issues, including preparations for early elections following his dissolution of parliament just last week, adding another layer of unpredictability (chart 5). The Thai government’s popularity has also dipped recently, partly due to criticism over its handling of floods in southern Thailand.

Chart 5: Thailand and Cambodia uncertainty index

Semiconductors and AI Lastly, we turn to semiconductor and AI-related risks in Asia. As in markets outside the region, this year’s tech rallies are increasingly seen as overextended (chart 6), with some arguing they have entered bubble territory. Many now believe that much of the upside in future earnings has already been priced in, leaving more room for disappointment than for positive surprises. Geopolitical and competitive considerations remain important too, as highlighted by the recent US approval to sell Nvidia’s high-end (though not top-tier) H200 chips to China. However, this approval may not generate the expected enthusiasm among Chinese consumers. If the reaction mirrors that seen after the earlier approval of Nvidia’s lower-end H20 chips, China may use these openings to promote domestic chipmakers such as Huawei. This could help local firms catch up to US peers and gradually reduce reliance on imported semiconductors. Also, if US chipmaker earnings disappoint due to a lukewarm reception of the H200 chips, while local Chinese chipmakers see increased upside potential, this could translate into a divergence in equity price trajectories between the sector’s stocks in the respective markets.

Chart 6: US and China technology stocks

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief