Asia| Jan 12 2026

Asia| Jan 12 2026Economic Letter from Asia: A Bumpy Start

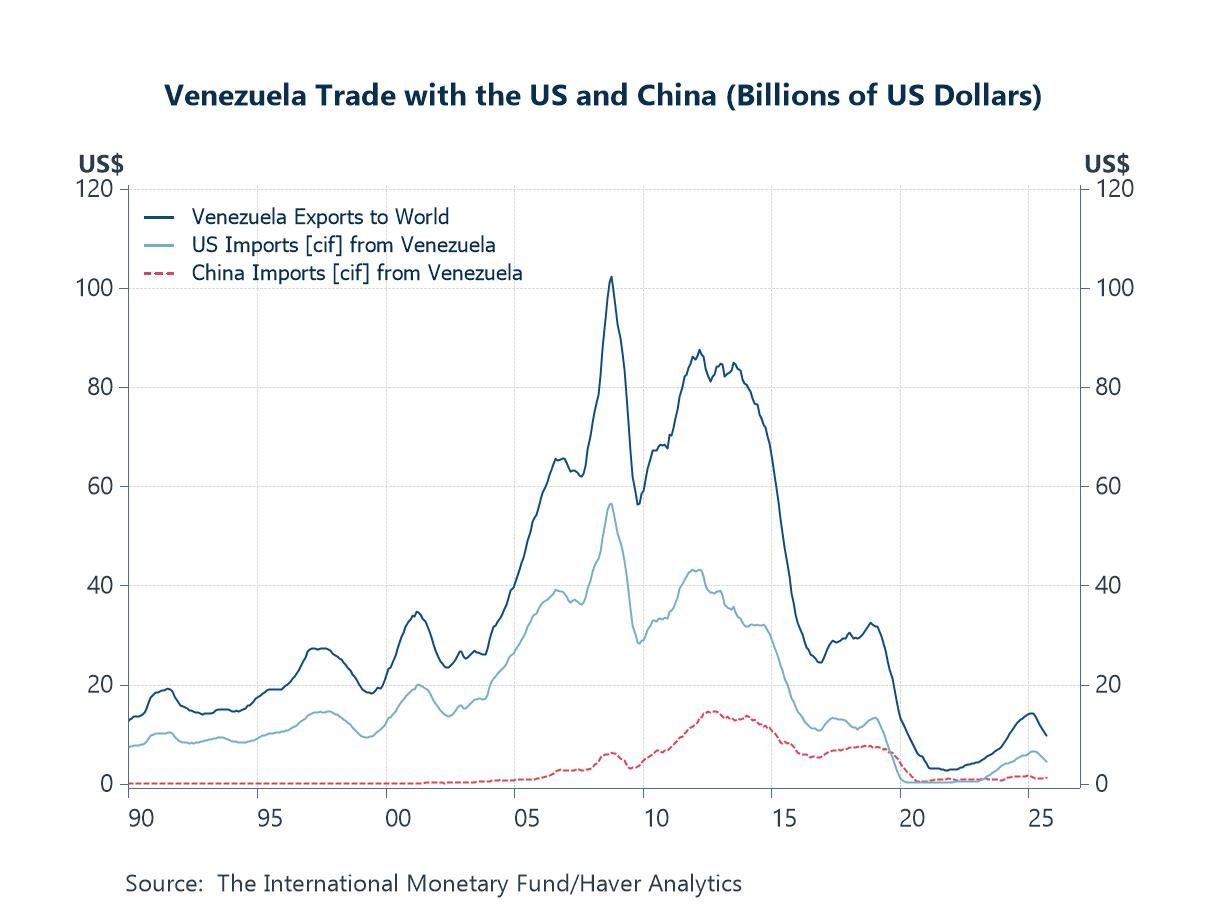

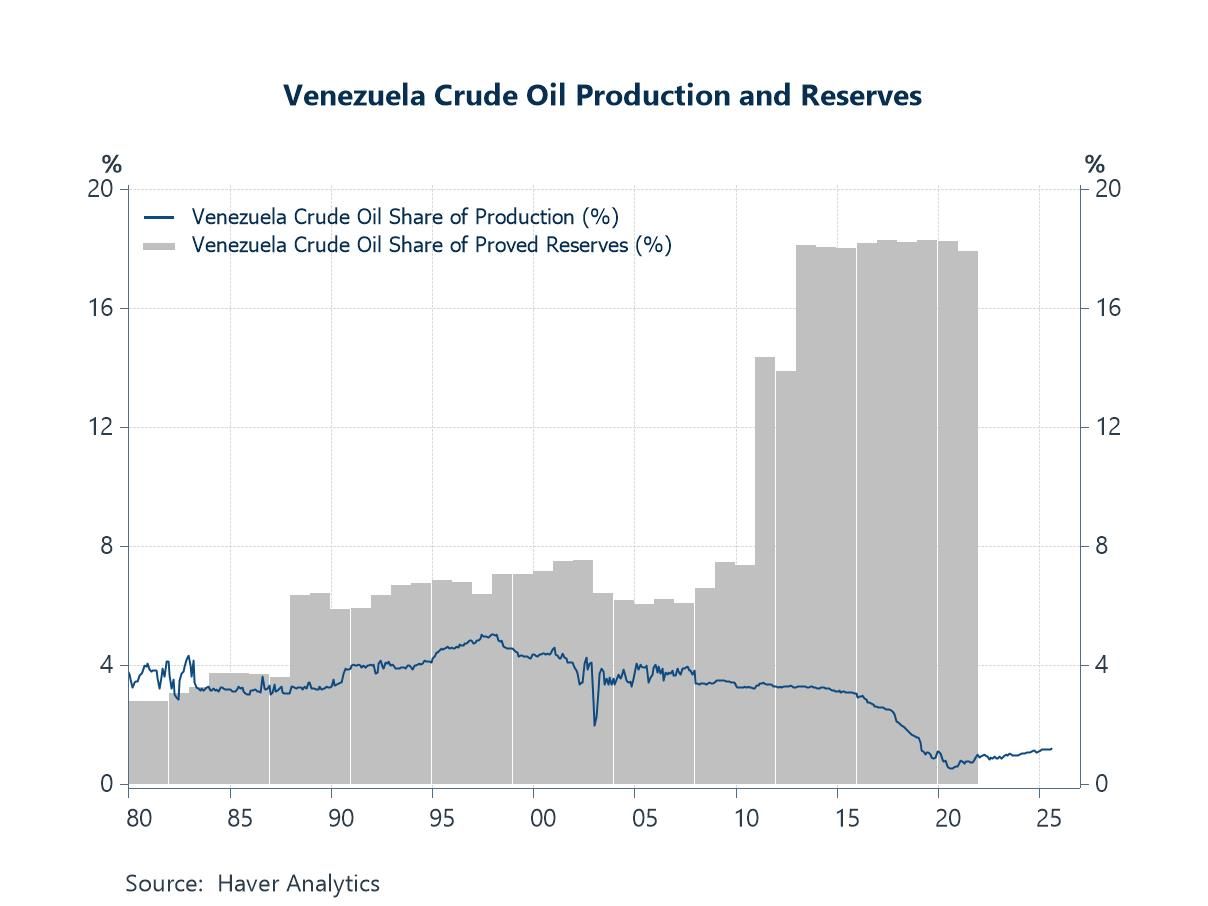

This week, we highlight several pertinent developments that have shaped the start of the year and may carry longer-lasting implications. To begin with, the recent capture of former Venezuelan President Maduro by the US authorities and the subsequent crude oil trade deal could have far-reaching effects—potentially altering China’s imports of Venezuelan crude and broader bilateral trade dynamics (chart 1), as well as global energy supply considerations (chart 2).

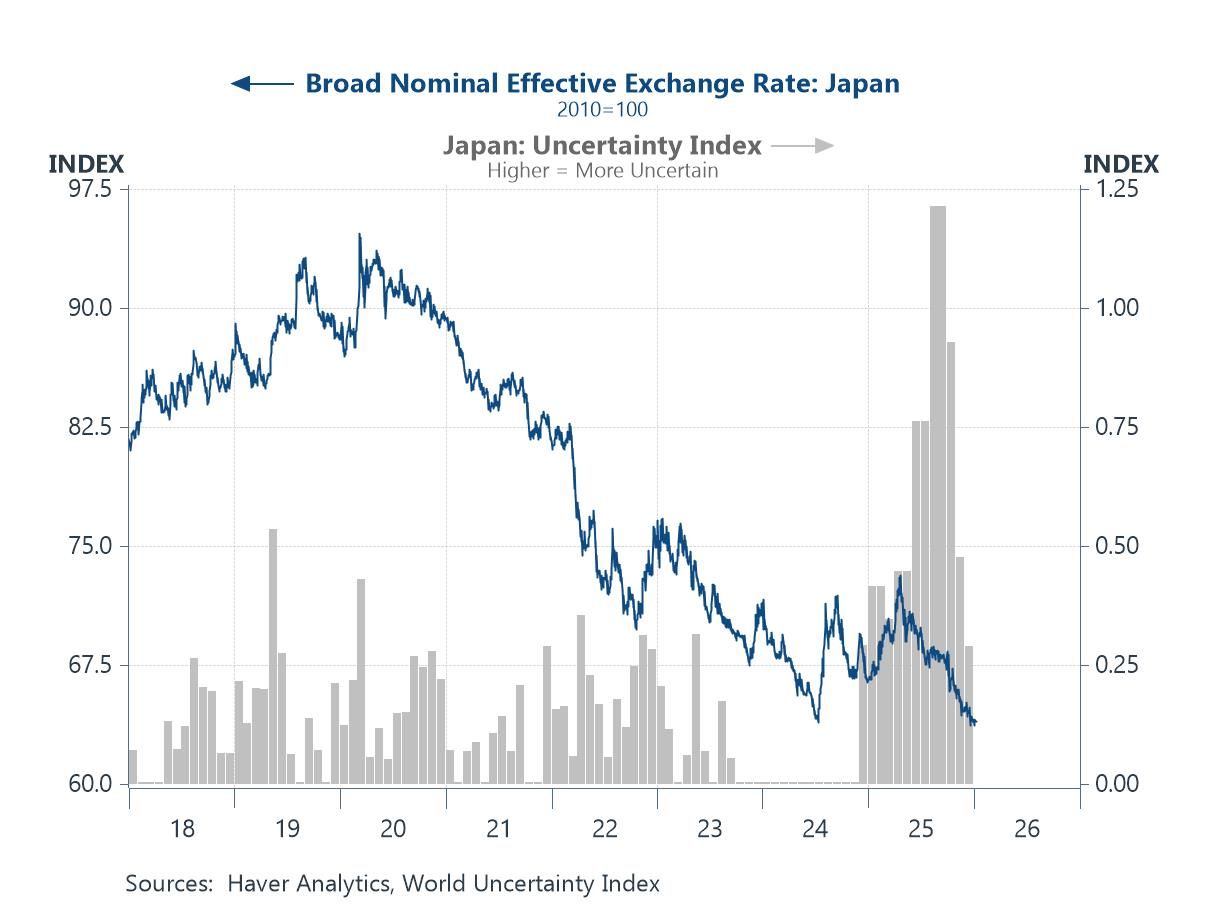

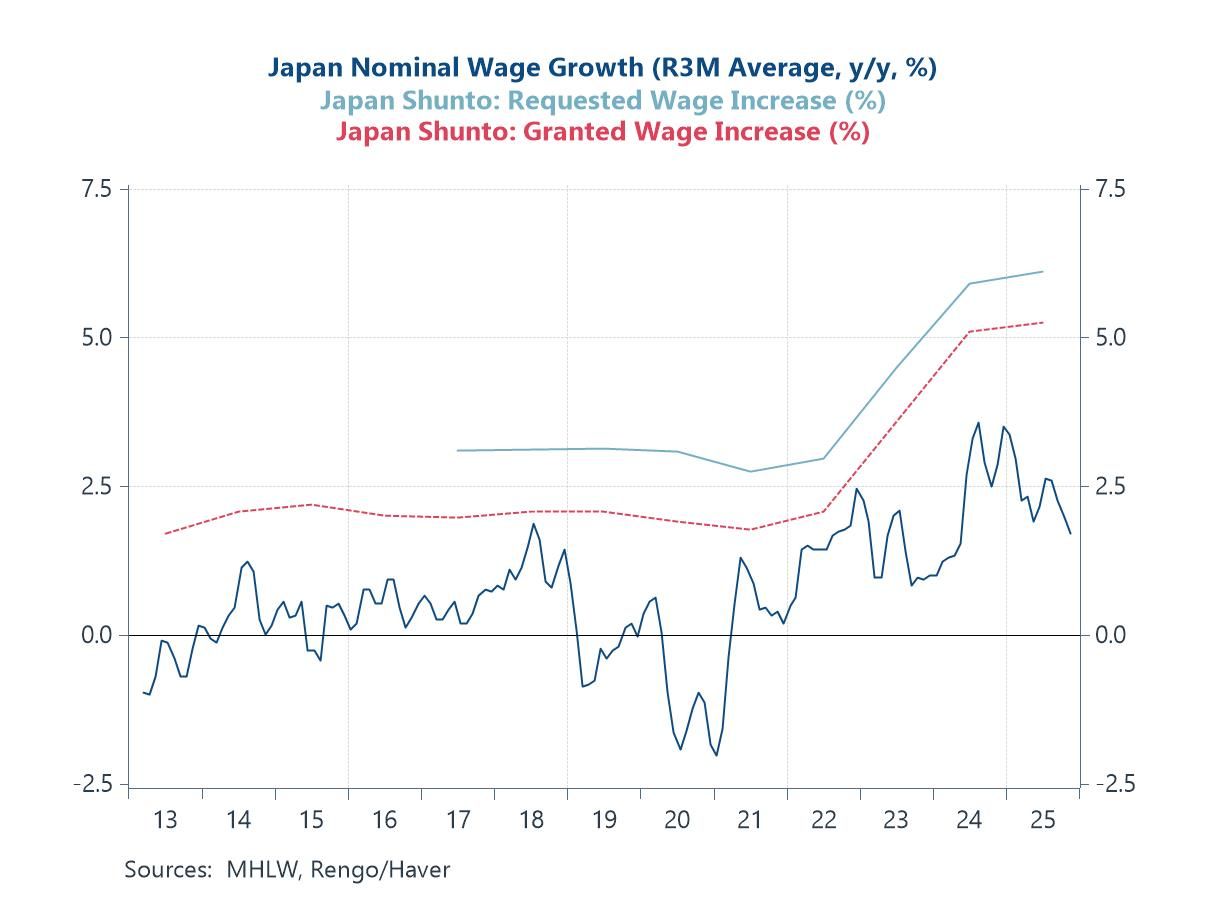

In Japan, Prime Minister Takaichi’s reported consideration of early snap elections, if enacted, would likely inject near-term political uncertainty (chart 3). However, should her gambit succeed, it could reduce policy uncertainty and pave the way for more fiscal policy activism. Against this backdrop, it is unsurprising that investors remain divided over the timing of the Bank of Japan’s next policy tightening, although the upcoming Spring wage negotiations (chart 4) ought to provide clearer signals for the monetary policy outlook.

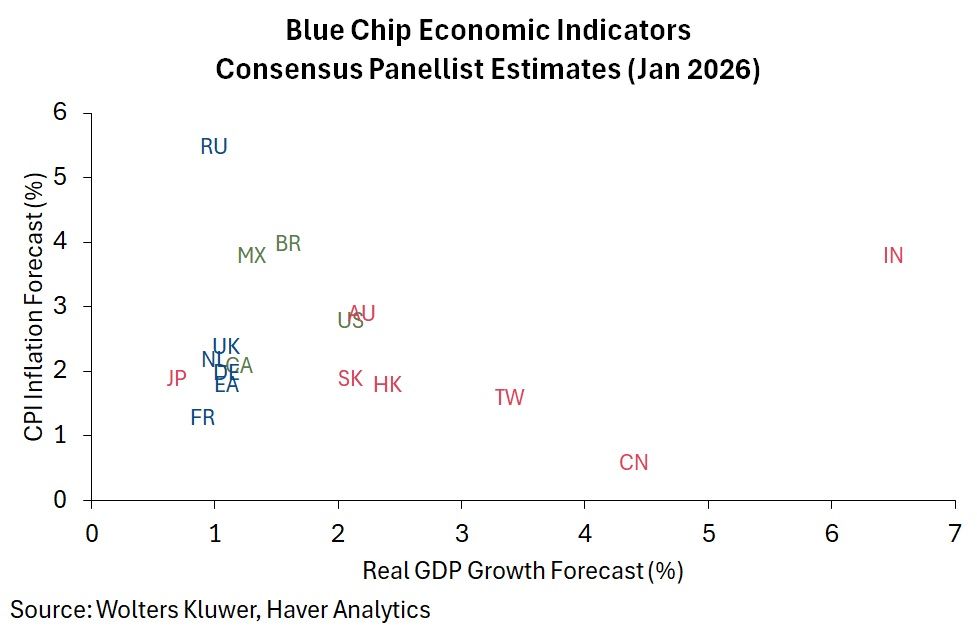

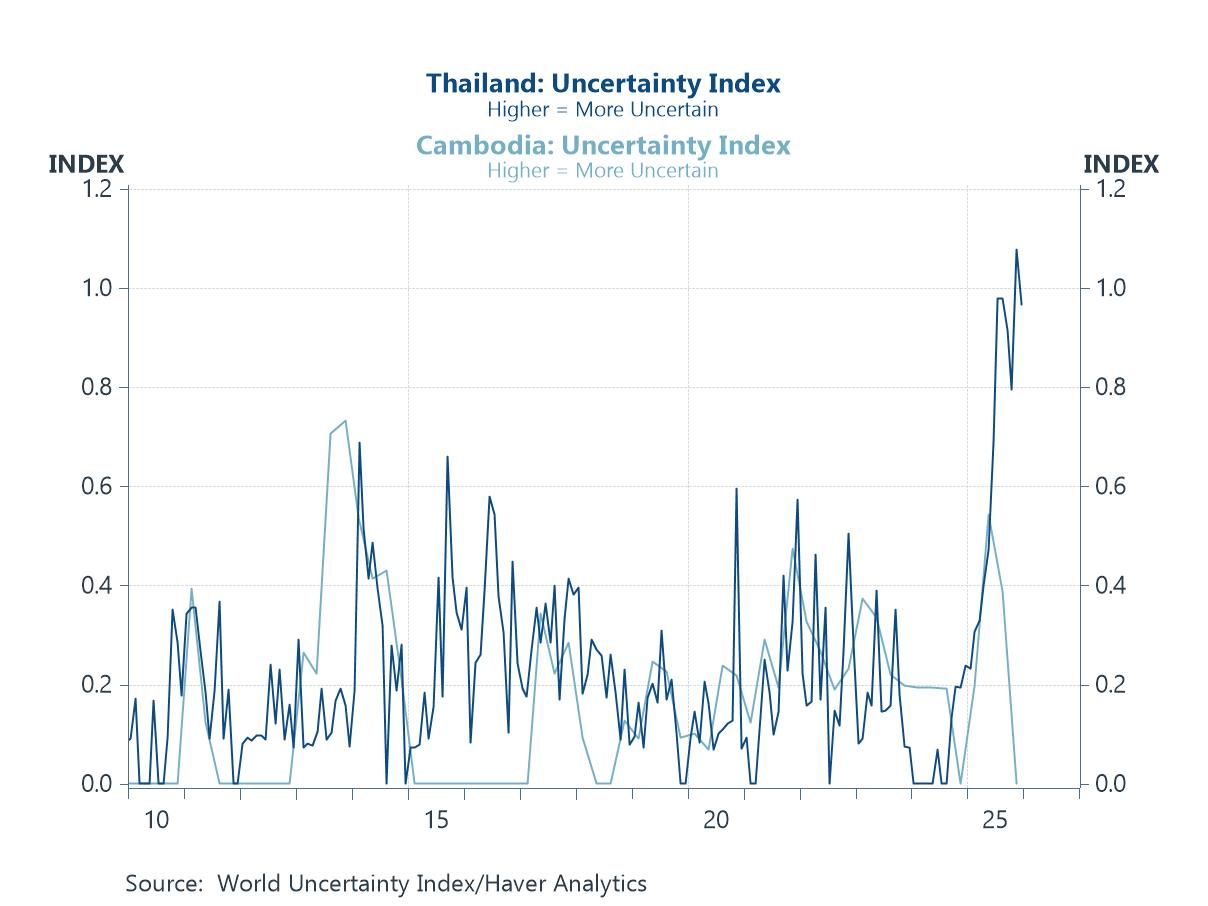

Turning to investor expectations from the latest Blue Chip survey, India is once again seen as the growth leader among major Asian economies, while also poised to record the highest inflation (chart 5). China, by contrast, is expected to deliver sub-5% growth this year alongside muted inflation. Lastly, in Southeast Asia, pockets of geopolitical tension persist—notably between Thailand and Cambodia (chart 6)—as Thailand prepares for snap elections next month.

The US, Venezuela, and China 2026 got off to a turbulent start following a recent US military operation in Venezuela that resulted in the capture of former President Maduro and his transfer to the US to face drug-related charges. In the aftermath, Venezuela’s former vice president (Delcy Rodriguez) was sworn in as interim leader, while US and Venezuelan authorities have reportedly already reached a new crude oil deal. Under the agreement, Venezuela would sell 30–50 million barrels of crude to the US at market prices, with the proceeds controlled by the US. These developments have several potential implications. First, some Venezuelan crude initially destined for China would likely be diverted to the US. China has been the main buyer of Venezuelan oil in recent years, although this is likely underreported in official data (chart 1), which would tighten conditions for the crude-import-dependent country. Second, an eventual increase in Venezuelan crude supply—previously constrained by heavy US sanctions—would likely exert downward pressure on global oil prices, all else equal, although significant challenges remain, as discussed below.

Chart 1: Venezuela trade with the US and China

To illustrate the potential significance of Venezuela’s crude oil industry, chart 2 shows that the country holds nearly a fifth of the world’s proved crude oil reserves. However, output remains disproportionately low relative to reserves, possibly reflecting years of US sanctions as well as mismanagement and chronic underinvestment. Given the current state of the industry, substantial investment will likely be required for Venezuela to restore production to historically high levels and to more fully tap its deep proved reserves. As a result, any meaningful surge in Venezuelan crude output is likely to take time, which may help explain the muted market response to recent US–Venezuelan developments. Also of note, China has been a major lender to Venezuela, including through “oil-for-loan” arrangements in which repayments are made in crude oil. It remains to be seen how these existing and future agreements may be affected by recent developments.

Chart 2: Venezuela crude oil production and reserves

Japan Setting aside the interplay between the US, Venezuela, and China, another economy worth watching early this year is Japan. Developments continue to unfold following renewed China–Japan tensions after Prime Minister Takaichi assumed office. With her approval ratings having remained consistently high since taking the helm, Takaichi is reportedly considering snap elections as early as next month to strengthen her ruling coalition’s parliamentary position. While a stronger mandate could reduce policy uncertainty, near-term political uncertainty would be the likely case. This interim uncertainty may be weighing on the yen. It is being compounded by expectations of upcoming pro-growth measures, including the $118 million supplementary budget passed last December and the prospect of additional fiscal stimulus next fiscal year, contingent on an electoral win (chart 3).

Chart 3: Japanese yen and uncertainty

Turning back to Japan and the monetary policy outlook, investors remain divided over the timing of the Bank of Japan’s (BoJ) next policy move following its December rate hike. This uncertainty is understandable given the multiple moving parts shaping the BoJ’s path, including the factors discussed above. Looking ahead, the upcoming annual wage negotiations and broader trends in wage growth (chart 4) will be closely watched by the BoJ as key preconditions for further rate hikes. Reflecting this uncertainty, our latest Blue Chip Economic Indicators survey shows investors split between expectations for a hike in March and views that the next move will only come after April.

Chart 4: Wage growth in Japan

Blue Chip Economic Indicators Delving into the latest Blue Chip survey results, chart 5 summarizes panellists’ expectations for growth and inflation this year. Focusing on major Asian economies, and as in 2025, India is seen to be leading the pack in terms of both real GDP growth and CPI inflation. That said, the inflation outlook may be subject to further revisions should India’s currently muted inflation—driven by falling food prices—persist for longer. For China, panellists currently expect sub-5% growth this year, implying a likely miss should a 5% growth target again be pursued. Inflation in China is once again expected to remain subdued. Japan, meanwhile, is forecast to post sub-1% real GDP growth, while CPI inflation is expected to hover around the authorities’ preferred 2% level. Looking ahead, attention will also turn to the IMF’s upcoming World Economic Outlook forecasts, due later this month.

Chart 5: January 2026 Blue Chip Economic Indicators consensus panellist estimates

Southeast Asia Last but not least, turning to Southeast Asia, promising AI- and tech-related growth continues in economies such as Malaysia and Vietnam. However, pockets of geopolitical tension persist, notably between Thailand and Cambodia, where border clashes have occurred despite previous attempts at peace, including one co-brokered by US President Trump. Against this backdrop, Thailand’s Prime Minister Anutin is preparing for snap elections in early February, amid a reported rise in nationalist sentiment linked to the ongoing clashes. These developments create latent risks for both Thailand and Cambodia (chart 6), while the uncertainty surrounding the elections also clouds the implementation of longer-term policies aimed at addressing Thailand’s deeper structural challenges.

Chart 6: Uncertainty in Thailand and Cambodia

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief