Dutch Trade Trends Improve Goods Balance—for Now

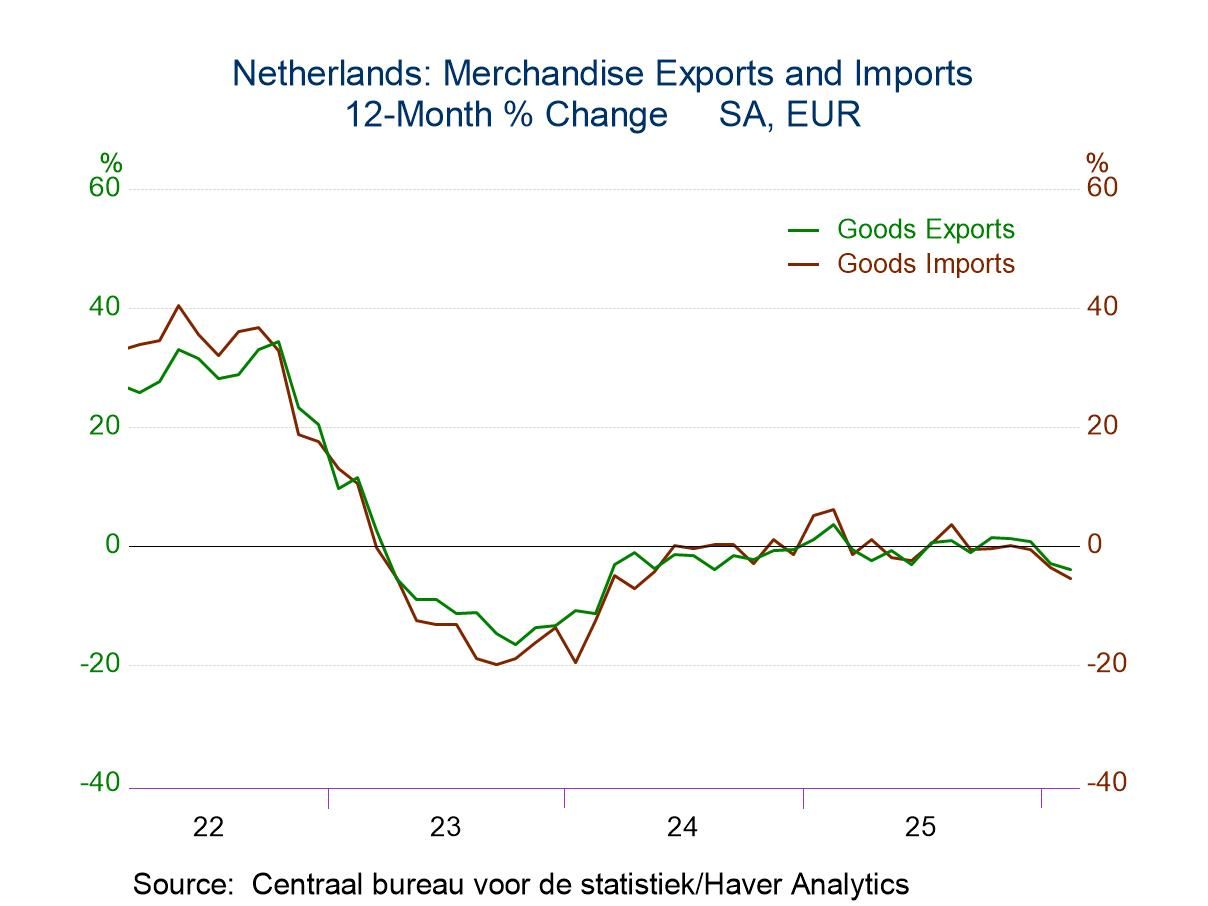

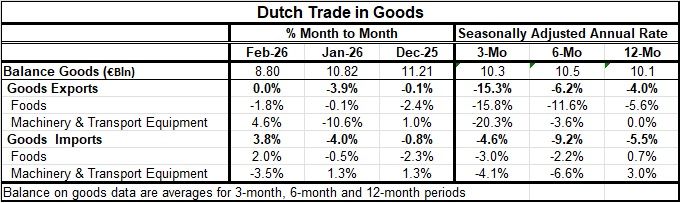

As the chart makes clear, Dutch exports and imports are driven by very complementary forces and tend to track one another closely. Both flows boomed when COVID ended, slowed to a contraction in 2023, and then recovered to maintain steady levels (growth rates that hugged a zero-percent growth rate) from mid-2024 to late-2025. Recently, exports and imports have begun to weaken, with both flows showing contraction over 12 months. Goods imports are falling at a 5.5% pace as exports are falling at a 4% pace.

As for intra-year trends, the sequential growth rates show exports have transitioned into a progressively more contractive mode, while imports have declined over 12 months, six months, and three months, but without a clear signal on whether the trend is getting better or worse.

Of course, the trade flow depends on price trends and economic trends; both are under strain and uncertainty.

The S&P Global PMIs had been tracing improvement through February, but their March values showed a broad weakening globally. We have yet to see the March number for Dutch trade in that window, but it’s coming, and we should brace for things to get worse. Oil prices, of course, will be rising sharply, and there are concerns about the knock-on effects of higher oil prices on activity. Already there are supply chain disruptions for goods other than oil, with fertilizers and helium frequently cited. It is the planting season for farms, and fertilizer is in strong demand. Helium is an input into the chip-making process, and a shortage is not good for the tech sector. The largest hub producing helium is in Qatar, and it has been shuttered since the war in Iran began.

If the closure of the Strait of Hormuz drags on—and the newest development is that the U.S. has put an embargo on that passage—we will have to see what other shortages develop and how bad the oil shortage becomes. It is a difficult time; it comes during a period in which central banks have largely been missing their inflation targets, leaving them less flexibility to deal with shortages and fallout. The Bank of England and the European Central Bank have put markets on notice that, if the Iran conflict drags on, at their next meeting rate hikes are quite possible. In the U.S., the Fed has given markets no guidance.

So far, the Baltic dry index has held up and does not show any clear evidence of global trade slowing. But that is something else to watch for. In economics, there is an expression about how things happen. And it says: first things take longer than you expect to occur, and then they progress at pace much faster than expected. There may not be a good warning period if these conditions worsen.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia