Global| Jun 03 2026

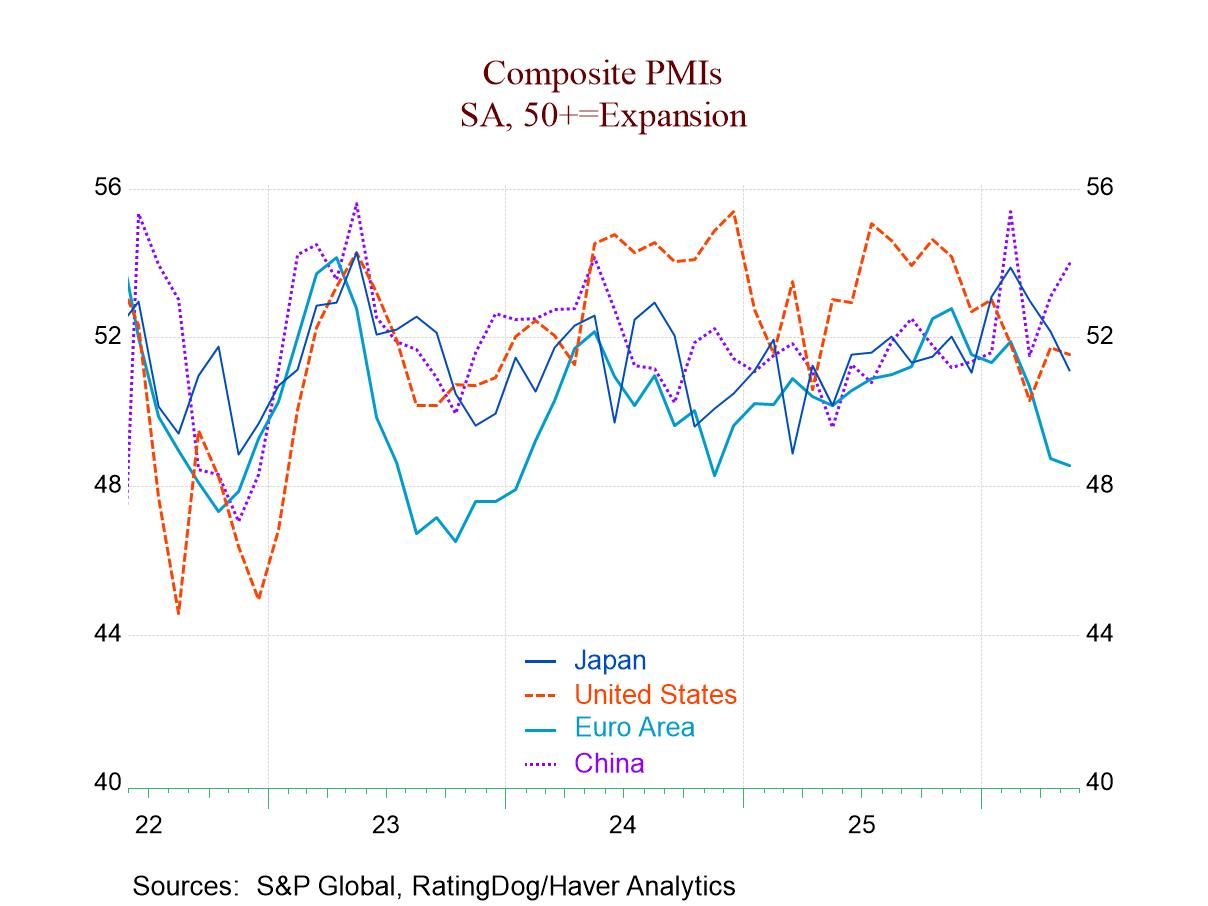

Global| Jun 03 2026Composite PMIs Ride Weakening Trend

With 25 countries in the mix, it can be hard to draw a simple summary statement about the condition of the global economy judging from the S&P composite PMIs. The manufacturing sector has recently been doing better, while the services sector is still in an extreme bout of lethargy globally. Fewer countries issue specific services sector indexes than issue manufacturing or composite PMI results.

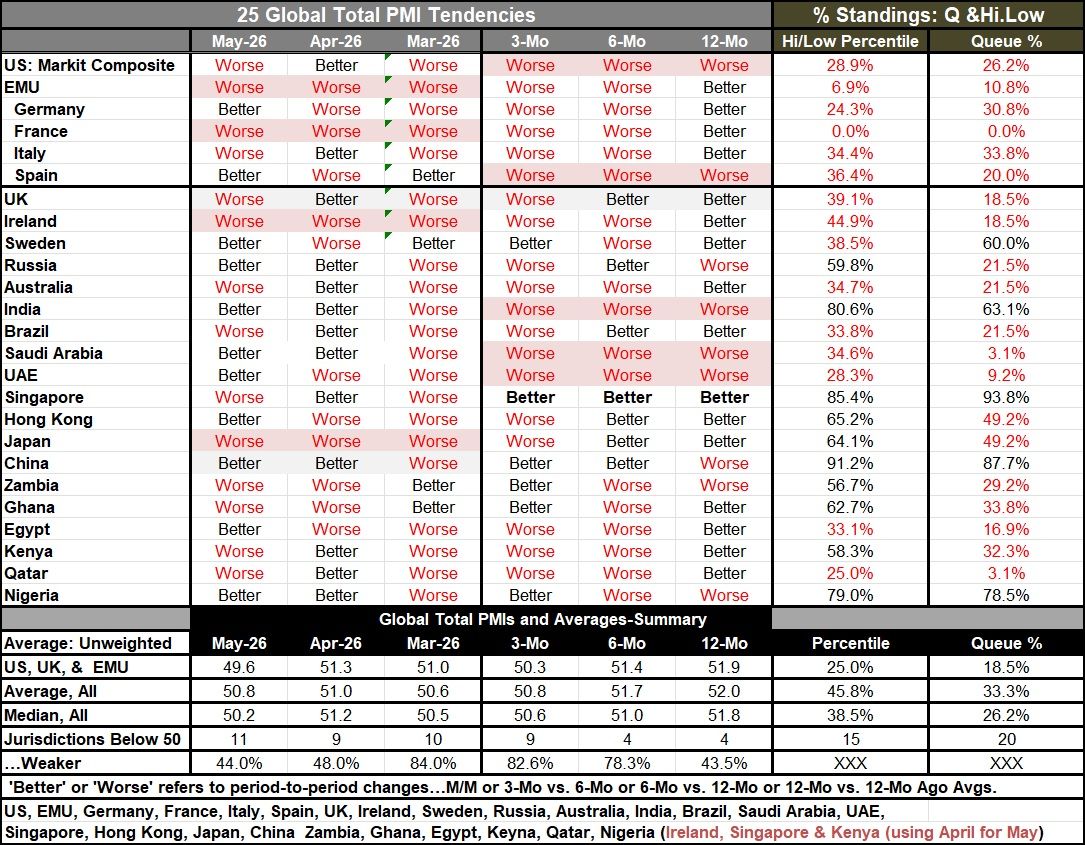

The services sector tends to dominate the composite readings, so what we see this month is a great deal of weakness in the S&P composites, reflecting service sector weakness. The 18 early reporting manufacturing reporters registered a median queue ranking in their 67.7 percentile; that compared to a median ranking of 26.2% for this group of 25. However, the two groups are not the same. If we recalculate for the 10 common reporters, we get a median manufacturing ranking of 61.5% compared to a composite median ranking of 23.8%; for those same ten, the services sector median ranking was in its 16.9 percentile. That is a ranking that seems to flirt with recession potentially. To that point, in May 2026, eleven of twenty-five composite PMIs registered diffusion values below 50, indicating contraction.

In May, among the 25 reporting composite PMI reporters, 44% of them were weakening month-to-month, which is less than half but still a very large proportion and not particularly good news; this followed 48% weakening in April and 84% weakening in March. So, with the heating up of war in the Middle East and the closure of the Strait of Hormuz, service sector conditions have gotten a lot worse even though it might have seemed logical that it would be the manufacturing sector that would suffer. The PMI data do not bear out that expectation. In March, the global PMI data improved only in Spain, Sweden, Zambia, and Ghana—thin gruel for good news.

On a monthly basis, there is sequential weakening in progress in the European Monetary Union, France, Ireland, and Japan.

If we look at the broader sequential data over three months, six months, and 12 months, we see that conditions have gotten progressively weaker, with 82.6% of these reporters weaker over three months, 78.3% weaker over six months, and 43.5% weaker over 12 months. There is progressive weakening on this broader timeline in the United States, Spain, India, Saudi Arabia, and the United Arab Emirates. There's sequential improvement indicated only in Singapore.

The queue percentile standing evaluations at the far right of the table rank and therefore order the data across these reporters, on observations back to January 2021. On that relatively long timeline, only 5 reporters have current readings above their respective 4.5-year. medians. Those are Singapore, China, Nigeria, India, and Sweden. On this timeline, the French composite is at its absolute lowest ranking of the period. The European Monetary Union reading is in its lower 10th percentile, with the four largest monetary union economies each having a ranking below their respective 35th percentiles. The U.S. ranking is in its 26th percentile, roughly just above the bottom quarter of its raked results. The U.K. is in its lower 18th percentile. Japan is near its median, at its 49th percentile; however, none of these readings are reassuring. For example, Japan’s near 50th percentile ranking compares to a weaker U.S. ranking, but the U.S. composite PMI diffusion value at 51.5 is stronger than Japan’s at 51.1. But the U.S. value is weaker relative to its history back to January 2021. Japan’s higher ranking actually simply refers to performance that is still quite weak, but nearly as good as it has done over the past 4.5 years. It is important to keep the relative (ranking) and the absolute (diffusion value) comparisons separate. Diffusion values are not presented in the table—except for a few averages/medians—because putting those data in table for the countries is prohibited by the data provider.

The weakness is broad-based. While the manufacturing sectors have been digging out, the services sectors have continued to worsen during the improvement in manufacturing—which I take to be a bad sign. Manufacturing tends to be the more sensitive signal, and we often think of manufacturing showing a turnaround in the economy before it becomes a process involving the entire economy. But in this case, it doesn't look like the manufacturing revival is progressing across the various economies. Certainly, one reason could be rising oil prices and the fact that oil prices eventually become an input to just about every single business—because if it's not a direct input, it's an indirect input through its impact on transportation costs.

Broad but mild slippage If we look at the average and median PMI values, we can see that while there has been broad slippage, the slippage has been quite slow. The average reading for this group over 12 months is the PMI at 52; that has slipped to 50.8 over three months and sits at 50.8 in May. The median for the group is 51.8 over 12 months; it has slipped to 50.6 over three months and registers 50.2 in May. The bad news is more that these economies have lingered at very weak readings than that there is technical slippage in progress. Over 12 months, there were only four of 25 reporters with PMIs below 50. Over three months, that figure has mushroomed to 9, and as of May, there are 11 reporters with PMIs below 50, indicating economic contraction. These are poor trends and clearly ones to watch. Weakness has been driven by the services sector where we get fewer observations and data, and this is a sharp counterpoint to some of the manufacturing data that have been improving.

Summing up In the U.S., for example, not only have some of the manufacturing data been improving but job market data—which had scraped to very low levels around the turn of the year—have been rising and returning to show more encouraging job growth for an economy with closed borders and weak labor force growth. Europe, on the same metrics, faces greater challenges. Monetary policy still has to be concerned with inflation that is over the top and rate hikes are coming to be expected. In the U.S., some revival in productivity creates a counterpoint, even though service sector readings continue to be weak. Forecasting in this environment, of course, is absolutely treacherous; even discerning what the current trend is from current data has become a challenging process. Markets for the most part remain relatively upbeat as stocks continue their advance in the U.S. Bond yields have been creeping up, but without damage to stocks, so far. Financial markets, exchange rates, and central bank activity are all going to be important features to keep an eye on. The usual detailed economic reports are confusing as uncertainty stirs the pot, increasing the turbidity surrounding the economic outlook.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief