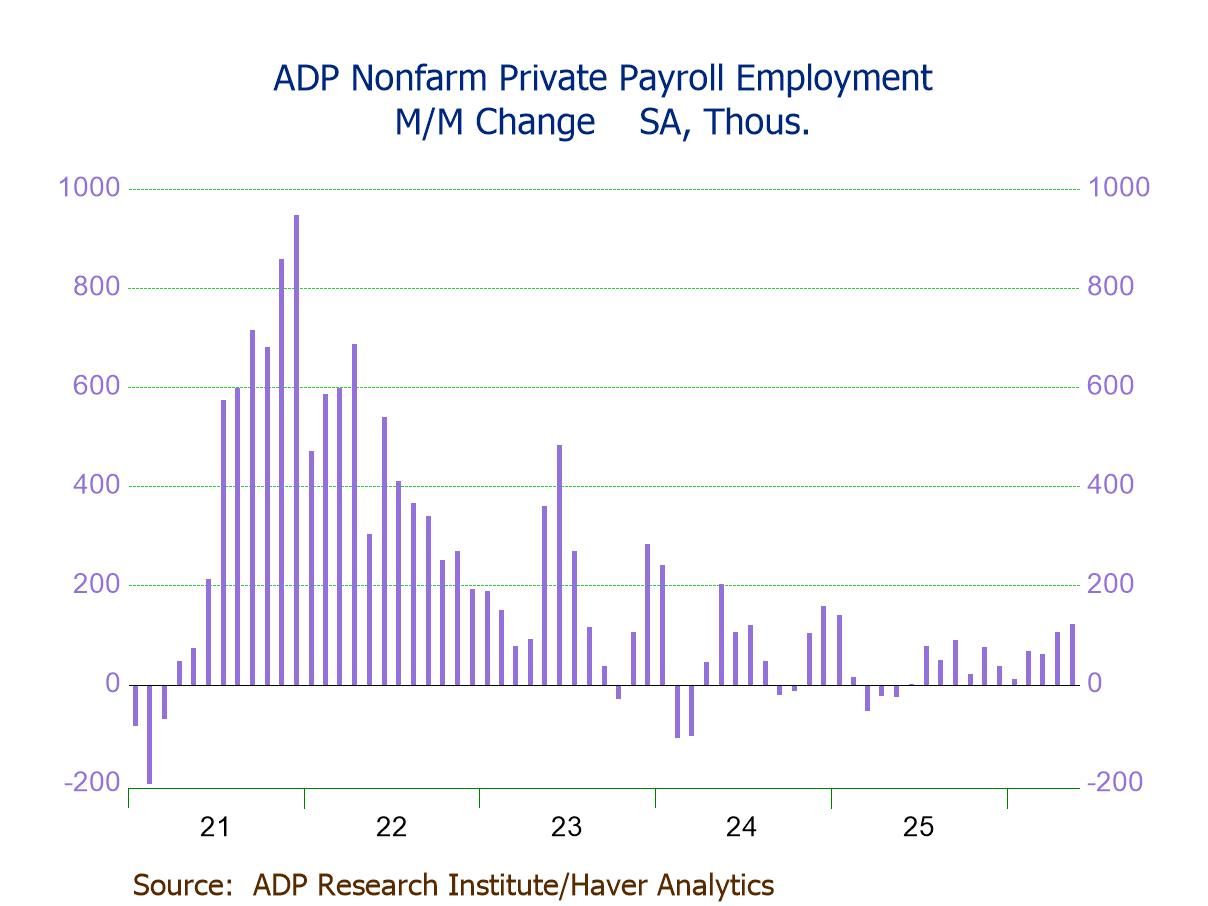

U.S. ADP Private Employment Growth in May Strongest Since Jan. ’25

Summary

- Private payrolls +122K in May, largest of 11 straight m/m gains, indicating sustained labor-market momentum.

- Broad-based hiring across company sizes, driven by small businesses (+67K).

- Service-sector jobs up (+114K), led by education & health svs. (+57K) and trade, transp. & utilities (+36K), partly offset by information (-9K).

- Goods-producing jobs up (+8K), driven by construction (+8K).

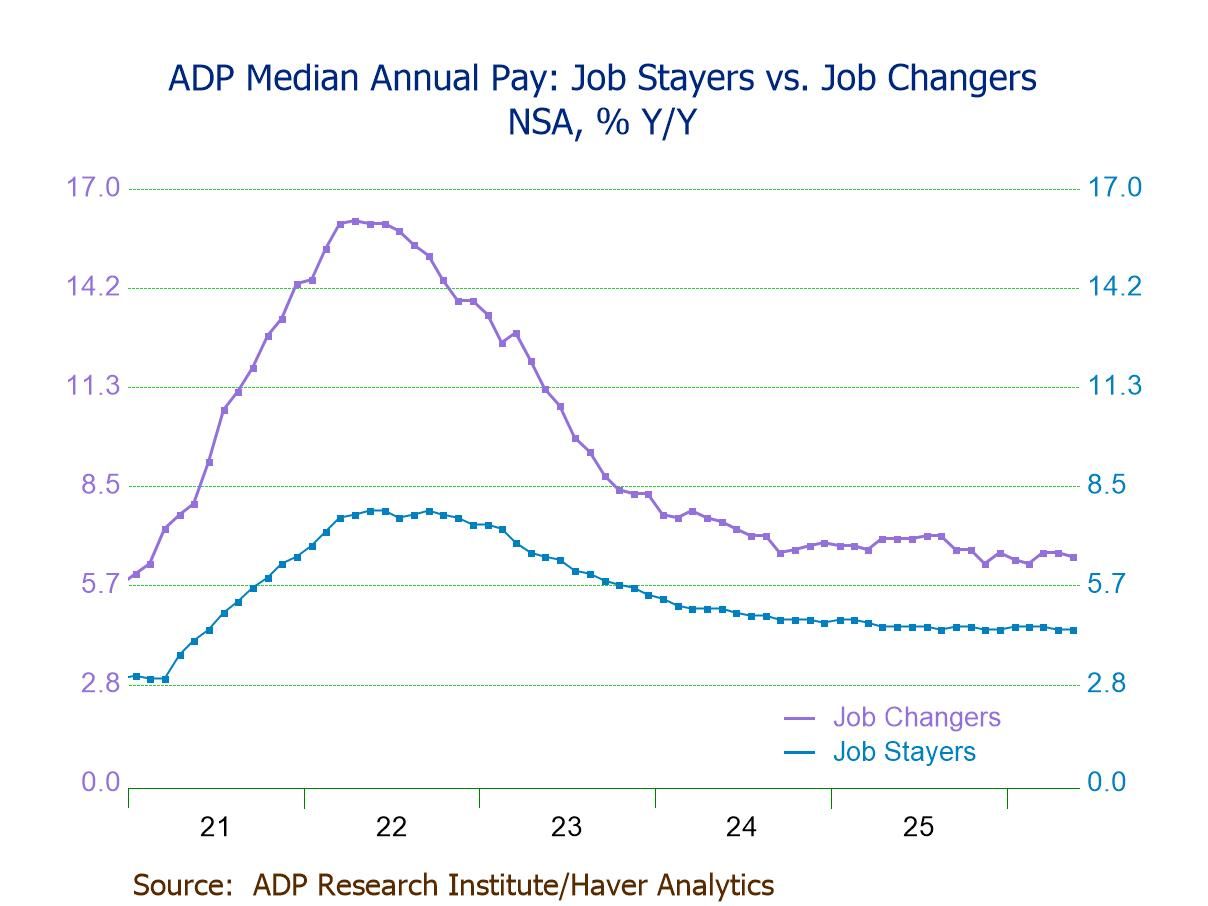

- Wage growth down marginally y/y for job changers (6.5%) but steady for job stayers (4.4%).

U.S. nonfarm private sector payrolls jumped a more-than-expected 122,000 (0.5% y/y) in May—the largest of 11 straight m/m gains and the strongest since January 2025—after rises of 105,000 in April (+109,000 initially) and 61,000 in March (unrevised), according to the ADP National Employment Report. The Action Economics Forecast Survey expected a 110,000 May increase. The three-month average change rose to 96,000 in May, the highest since February 2025, from 77,000 in April and 46,000 in March.

Small business hiring (less than 50 employees) rose 67,000 (0.9% y/y) in May, the 11th consecutive m/m rise, after a 63,000 gain in April (+65,000 initially), with employment in very small firms (1-19 employees) up 49,000 and employment in small firms (20-49 employees) up 18,000. Employment at medium-sized firms (50-499 employees) advanced 17,000 (-0.3% y/y) in May following a 2,000 increase in April (unrevised) and two successive m/m declines. Large business hiring (500+ employees) rose 40,000 (1.6% y/y), the third m/m rise in four months, after a 42,000 April rebound (unrevised).

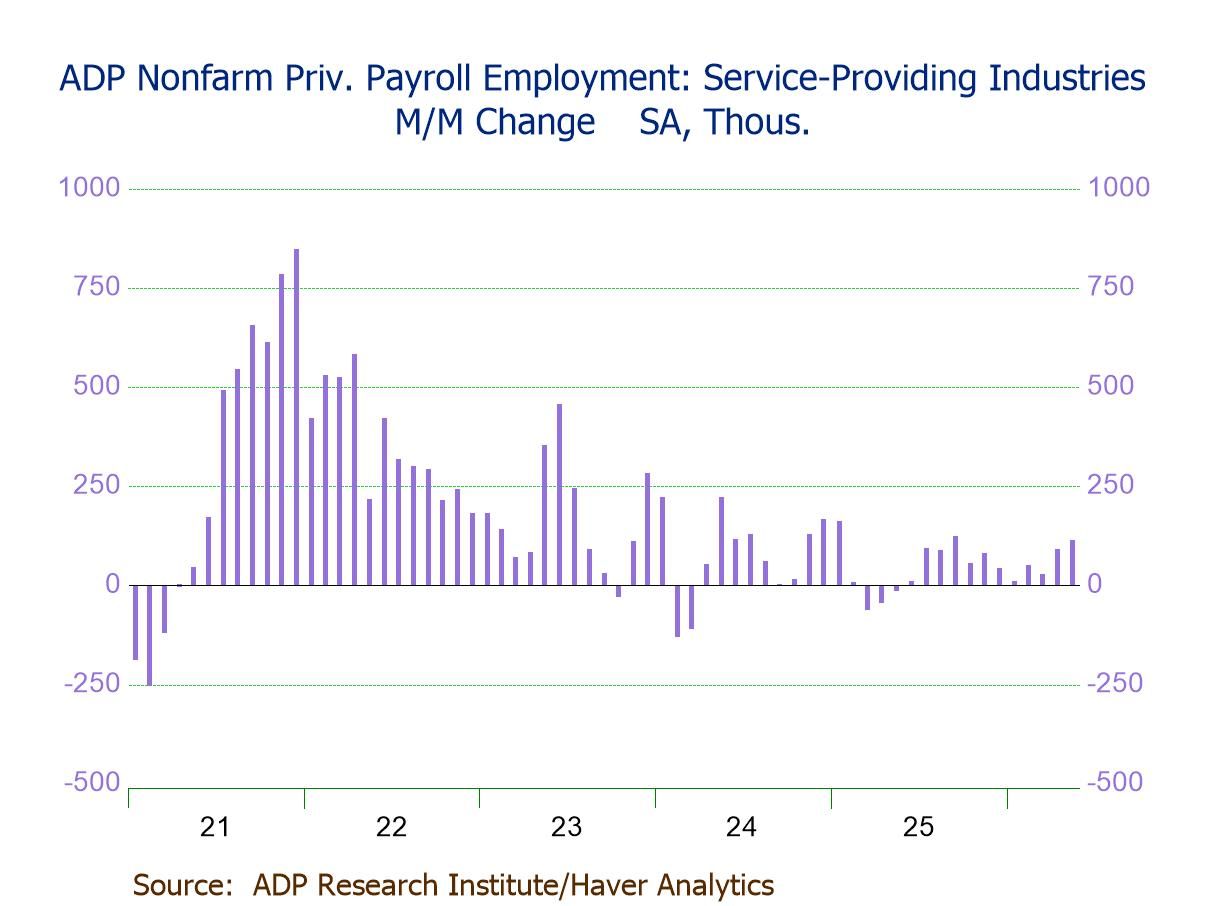

Service-producing jobs jumped 114,000 (0.7% y/y) in May, the 12th straight m/m gain, on top of a 91,000 rise in April (+94,000 initially). May’s gain was led by education & health services (+57,000), followed by trade, transportation & utilities (+36,000), professional & business services (+11,000), leisure & hospitality (+8,000), financial activities (+7,000), and other services (+4,000). In contrast, employment fell m/m in information (-9,000) in May, the only declining category, following three consecutive m/m increases.

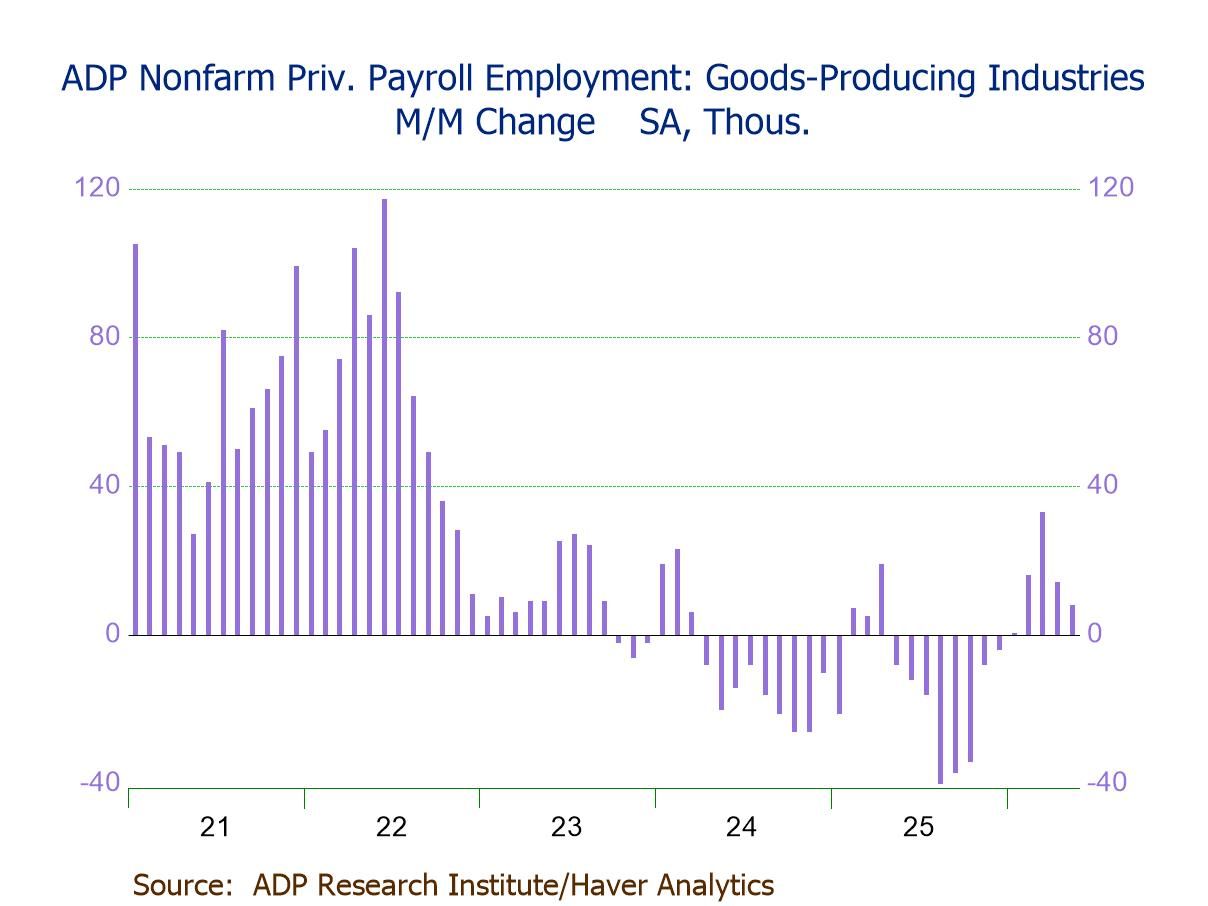

Goods-producing employment increased 8,000 (-0.4% y/y) in May, the smallest of four straight m/m gains, following a 14,000 rise in April (+15,000 initially). May’s increase was led by construction (+8,000) and manufacturing (+3,000, the first m/m increase since March 2024), while natural resources & mining (-3,000) fell m/m for the first time since January.

By region, nonfarm private payroll employment rose m/m across all major regions in May, reflecting m/m gains in the West (+45,000; +1.0% y/y), Northeast (+35,000; +0.4% y/y), South (+23,000; +0.5% y/y), and Midwest (+21,000; +0.2% y/y).

Wage growth for job changers eased to 6.5% y/y in May from 6.6% in April and March, remaining well below a high of 16.1% in April 2022. Wage growth for job stayers held steady at 4.4% y/y for the second consecutive month in May, holding in a narrow 4.4%-4.5% range since April 2025. Pay growth was unchanged across major industries, including financial activities (5.1% y/y), manufacturing (4.8% y/y), construction (4.5% y/y), leisure & hospitality (4.5% y/y), trade, transportation & utilities (4.4% y/y), education & health services (4.2% y/y), other services (4.1% y/y), and professional & business services (4.1% y/y), while pay growth in natural resources & mining dipped to 4.2% in May from 4.3% in April.

The ADP National Employment Report and Pay Insights data can be found in Haver's USECON database. Historical figures date back to January 2010 for private employment. Pay data date back to October 2020. The expectation figure is available in Haver's AS1REPNA database.

Winnie Tapasanun

AuthorMore in Author Profile »Winnie Tapasanun has been working for Haver Analytics since 2013. She has 20+ years of working in the financial services industry. As Vice President and Economic Analyst at Globicus International, Inc., a New York-based company specializing in macroeconomics and financial markets, Winnie oversaw the company’s business operations, managed financial and economic data, and wrote daily reports on macroeconomics and financial markets. Prior to working at Globicus, she was Investment Promotion Officer at the New York Office of the Thailand Board of Investment (BOI) where she wrote monthly reports on the U.S. economic outlook, wrote reports on the outlook of key U.S. industries, and assisted investors on doing business and investment in Thailand. Prior to joining the BOI, she was Adjunct Professor teaching International Political Economy/International Relations at the City College of New York. Prior to her teaching experience at the CCNY, Winnie successfully completed internships at the United Nations. Winnie holds an MA Degree from Long Island University, New York. She also did graduate studies at Columbia University in the City of New York and doctoral requirements at the Graduate Center of the City University of New York. Her areas of specialization are international political economy, macroeconomics, financial markets, political economy, international relations, and business development/business strategy. Her regional specialization includes, but not limited to, Southeast Asia and East Asia. Winnie is bilingual in English and Thai with competency in French. She loves to travel (~30 countries) to better understand each country’s unique economy, fascinating culture and people as well as the global economy as a whole.

More Economy in Brief