December CPI: Price Increases Quickened After Two Slow Months

Summary

- Not by enough to suggest that restraint in October and November reflected distortions from the government shutdown

- But by enough to suggest that October and November reflected normal volatility rather than the beginning of a slower trend.

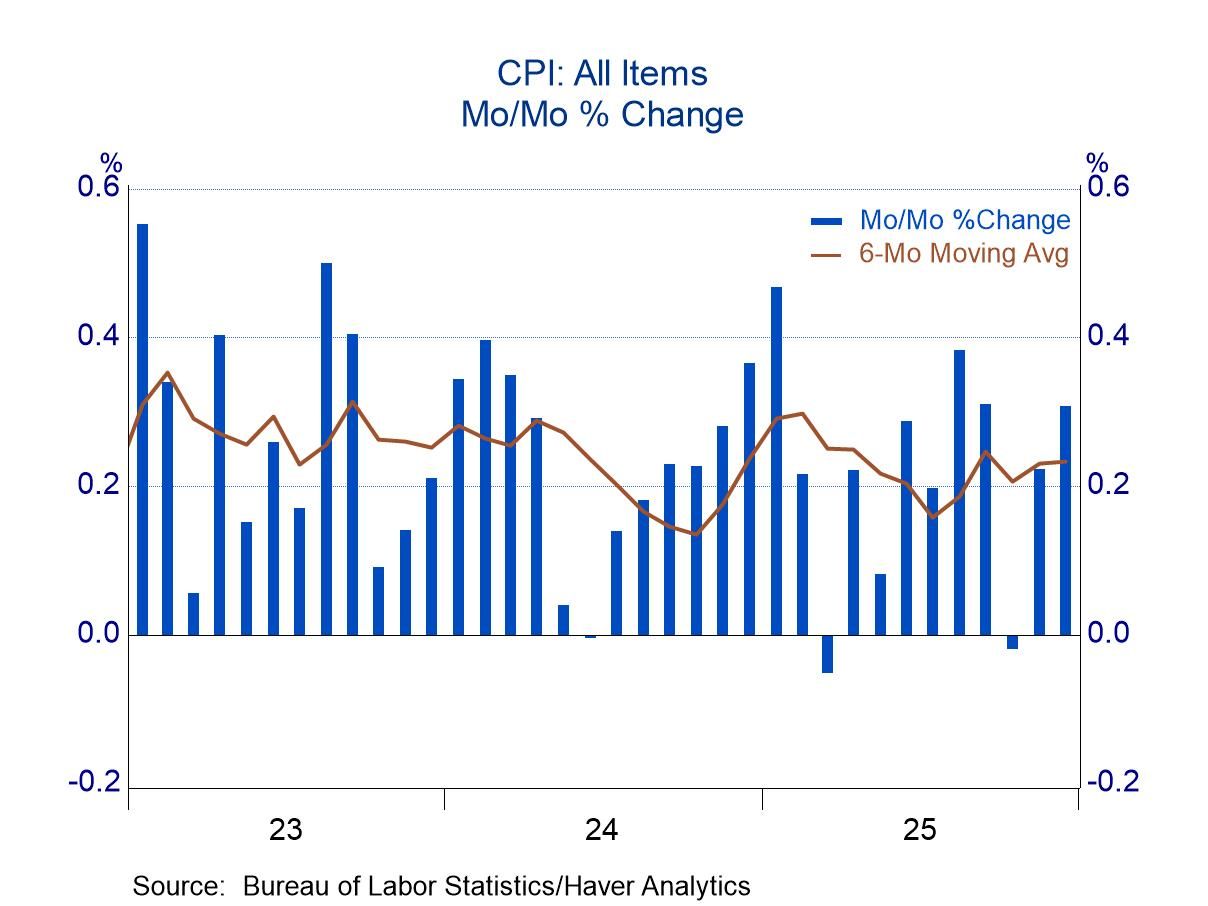

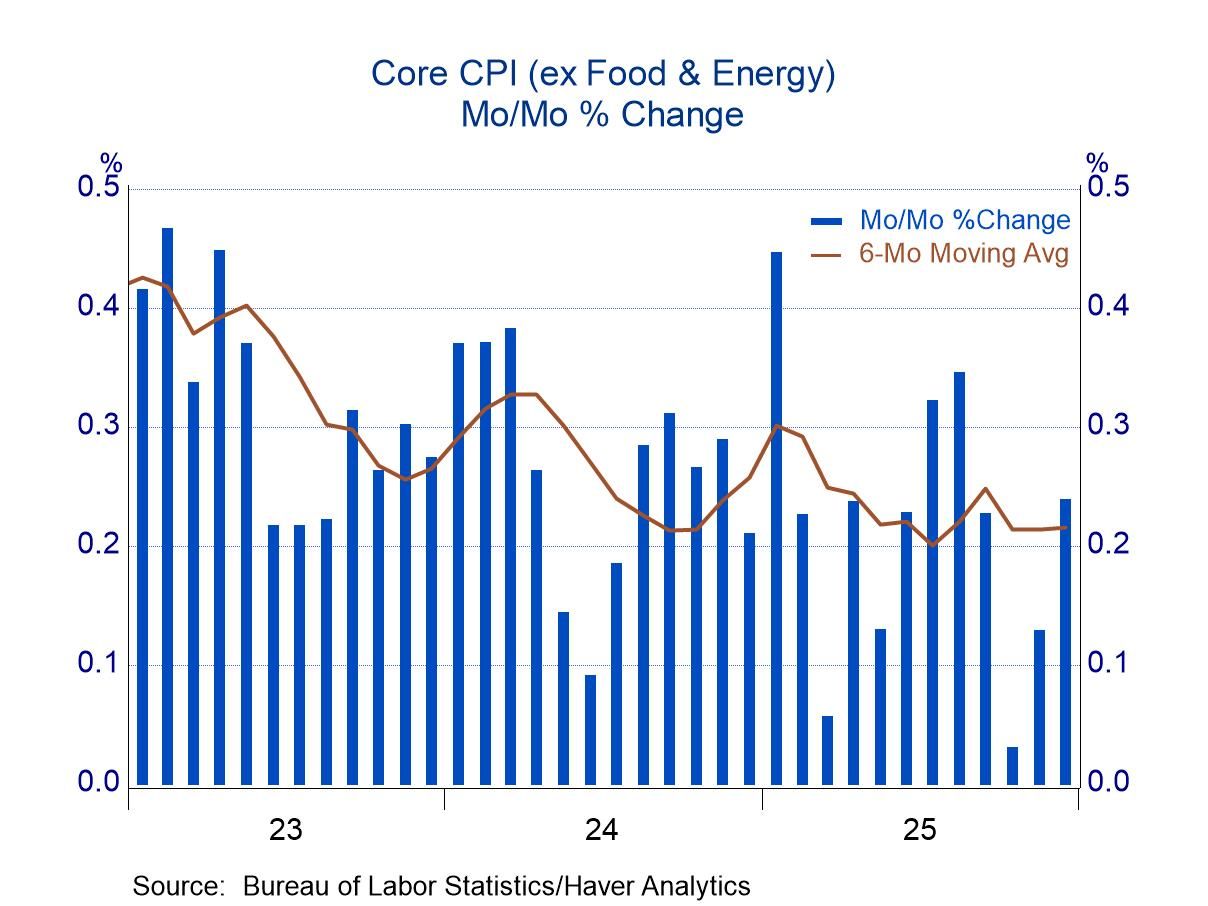

The consumer price index rose 0.3% in December, while the core index (prices excluding food and energy) rose 0.2%. Both measures were faster than the averages of 0.1 percent in the prior two months. (The Bureau of Labor Statistics did not publish a CPI for October because of the government shutdown. Both the headline and core indexes showed increases of 0.2% for the two-month period from September to November.)

The December results were not pronounced enough to suggest that the restraint in October and November reflected distortions triggered by the government shutdown. At the same time, they were not soft enough to suggest that October and November were signaling faster deceleration in inflation. The past three months seemed to be showing the same degree of random volatility seen in the prior two years, with the underlying trends showing a slight degree of deceleration. The year-over-year increase in headline CPI totaled 2.7%, only slightly slower than 3.0% in mid-2024. The Core has eased a bit more: 2.6% in December versus 3.3% in mid 2024.

Prices of core goods and services have been following different paths in the past few years, and they carried different signals in December. Prices of core goods showed no month-to-month change in December, which kept the year-over-year trajectory moving sideways. The flat pattern is encouraging in that it suggests that core goods inflation is perhaps steadying after trending upward since mid-2024. Core service prices rose 0.3 percent in December, in line with the recent average. Core service inflation showed little easing in the early part of 2025, but hints of slowing emerged from September to November. December results, though, raised questions about faster deceleration in service inflation.

The Consumer Price figures can be found in Haver's USECON database. The expectations figure is contained in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global