Global| Apr 07 2026

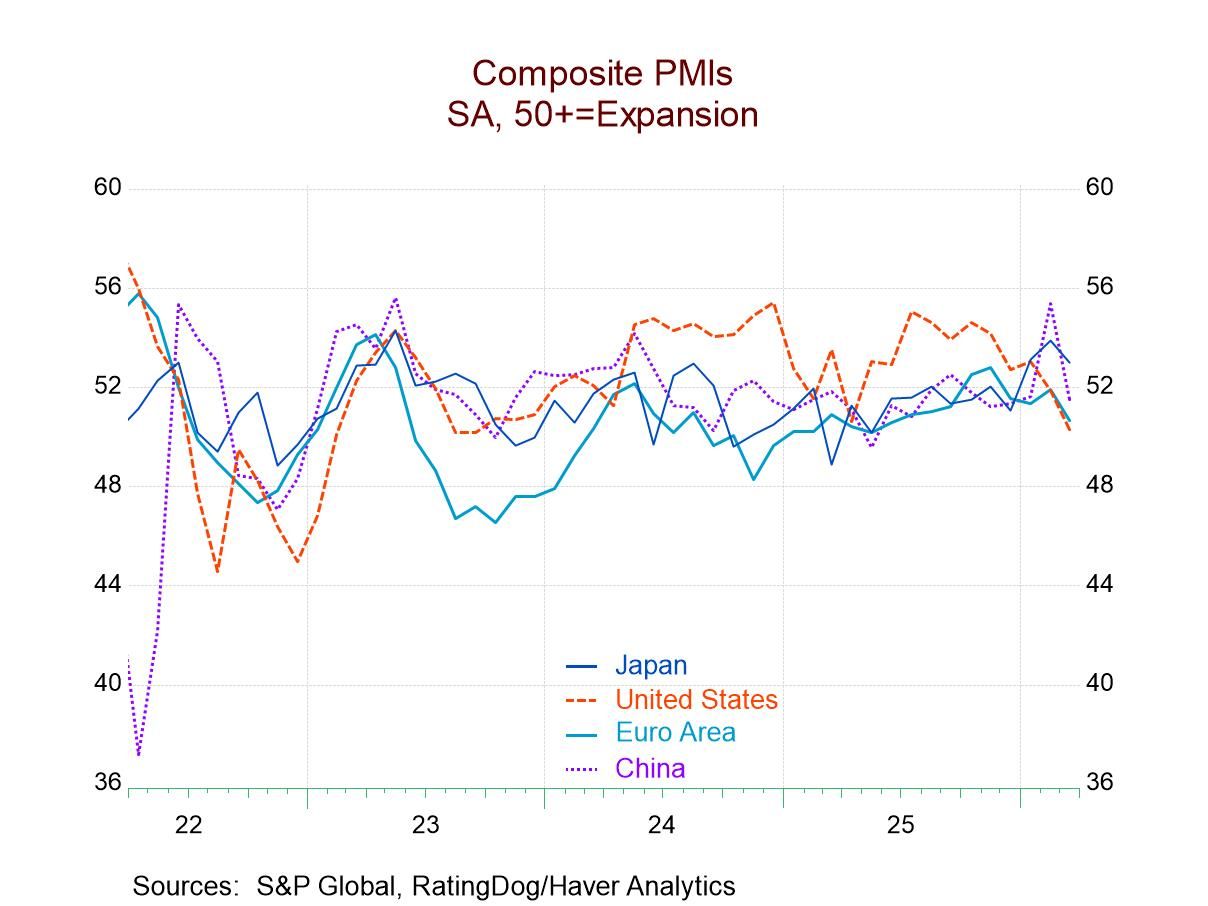

Global| Apr 07 2026Composite PMIs Retreat Broadly

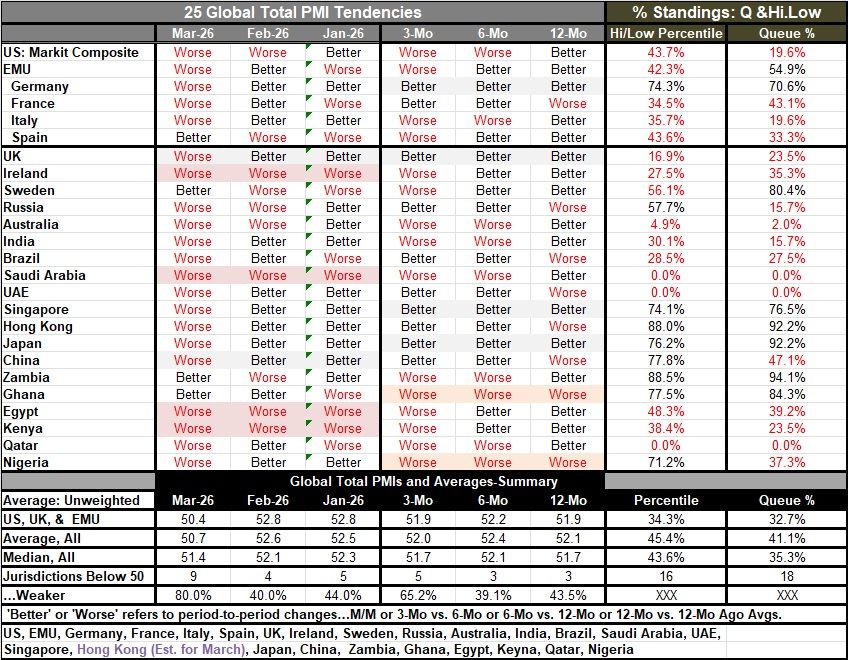

The S&P composite PMIs in March weakened decisively across the board, with only four of 25 reporters showing an improvement in March compared to February. February had been a strong month, with only 10 of 25 monthly composite indicators weaker on a month-to-month basis. In January, 11 of the composite indicators weakened month-to-month. So, between January and March, the proportion of countries showing composite indicators as weaker month-to-month went up from 40% to 44% and then all the way up to 80%, a huge shift for the worse.

Sequential trends Sequentially, looking at 12-months compared to 12-months ago, six-months compared to 12-months, and three-months compared to six-months, we see a similar progression. Over 12 months, 43.5% of the reporters were weaker; over six months, 39.1% of them were weaker period-to-period. And then over three months, that proportion jumped to 65.2% that were weaker month-to-month.

The war in Iran has been reflected in these numbers. We see it very clearly for the March data, the first full month after the attack. The average and median total PMI readings deteriorated from February to March: the average readings fell from 52.6 in February to 50.7 in March, and the median readings fell from 52.1 to 51.4.

The number of reporters with PMI values below 50, indicating contraction, jumped to 9 in March from 4 in February and 5 in January.

The data show that there has been broad weakening among these reporters. In addition, there has been a sharp rise in the number of them reporting outright economic contraction. The composite indexes are showing not just weakness month-to-month, but actual stepped-up contraction.

The queue percentile standings are also substantially degraded, with only eight of the 25 queue metrics that are reported above their historic medians on data back to January 2022. And the countries that are reporting good performance are often very small countries. Ghana and Zambia show very strong queue percentile standings. Sweden shows a high percentile standing. However, Japan and Hong Kong also show percentile standings in their 90th percentile, and Germany's standing has gotten to its 70th percentile. However, if oil prices climb and shortages in a variety of supply chains begin to be impacted because of the lack of oil, and in some cases, fertilizer and other commodities, we are going to start to see weakness spread.

In some developing countries, there's already a more generalized economic weakness being caused by fuel rationing because prices are so high. If the Strait of Hormuz is not open soon, these conditions are going to get demonstrably worse. Even though the U.S. economy has done relatively well and is unaffected by oil supply shortages—although prices in the U.S. certainly have risen—the U.S. composite PMI index has only a 19.6 percentile standing, not a terribly good place to say that the economy is largely unaffected by these events. The U.S. composite PMI has fallen for two months in a row.

Not surprisingly, three countries have reported the lowest composite PMI readings since 2022 when these rankings began. They are Saudi Arabia, Qatar, and the United Arab Emirates, all of whom are in the middle of this Middle East conflict.

The European Monetary Union posted a queue standing above its 50th percentile, at 54.9. And its diffusion reading on the month at 50.5 is similar to the U.S. at 50.3, indicating that economic activity is still expanding in the community—but barely. Both France and Italy logged composite PMI readings below 50; France has generated three sub-50 diffusion readings in a row, and in addition, three more of them sequentially over three months, six months, and 12 months. The queue standings may overstate the case for resiliency in some instances. There was plenty of weakness to go around across economies in March.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief