Asia| Apr 06 2026

Asia| Apr 06 2026Economic Letter from Asia: First-Round Effects

In this week’s Letter, we examine the first-round price impacts of the surge in oil prices stemming from the ongoing Middle East conflict in Asia. Despite recent rhetoric and reports suggesting a potentially swift resolution, the conflict continues to unfold, with a ceasefire hanging in the balance, and with some measures of shipping volumes through the Strait of Hormuz still reduced to a trickle. At the same time, crude oil prices have been whipsawing amid shifting market perceptions about the persistence of the current supply shock (chart 1). The initial effects of higher oil prices are already showing up in hard data, particularly in energy- and fuel-related inflation across Indonesia, South Korea, and Vietnam (chart 2). In response, several governments have rolled out sizeable subsidy programmes to cushion rising energy costs, though these measures come with significant fiscal strain.

We also assess recent consumer inflation expectations in South Korea and Taiwan, which show early signs of edging higher (chart 3), although there is as yet no clear evidence of a meaningful unanchoring. To add further nuance, our latest Blue Chip survey suggests that most panellists expect only a limited and temporary pass-through from higher energy prices to core inflation, though a non-trivial minority anticipate a more persistent effect (chart 4). On the policy front, respondents broadly expect central banks to delay easing while avoiding outright tightening, with outcomes likely to diverge across regions (chart 5). In the near term, upcoming policy decisions in India, New Zealand, and South Korea—alongside other key data releases—will provide a useful test of these expectations (chart 6).

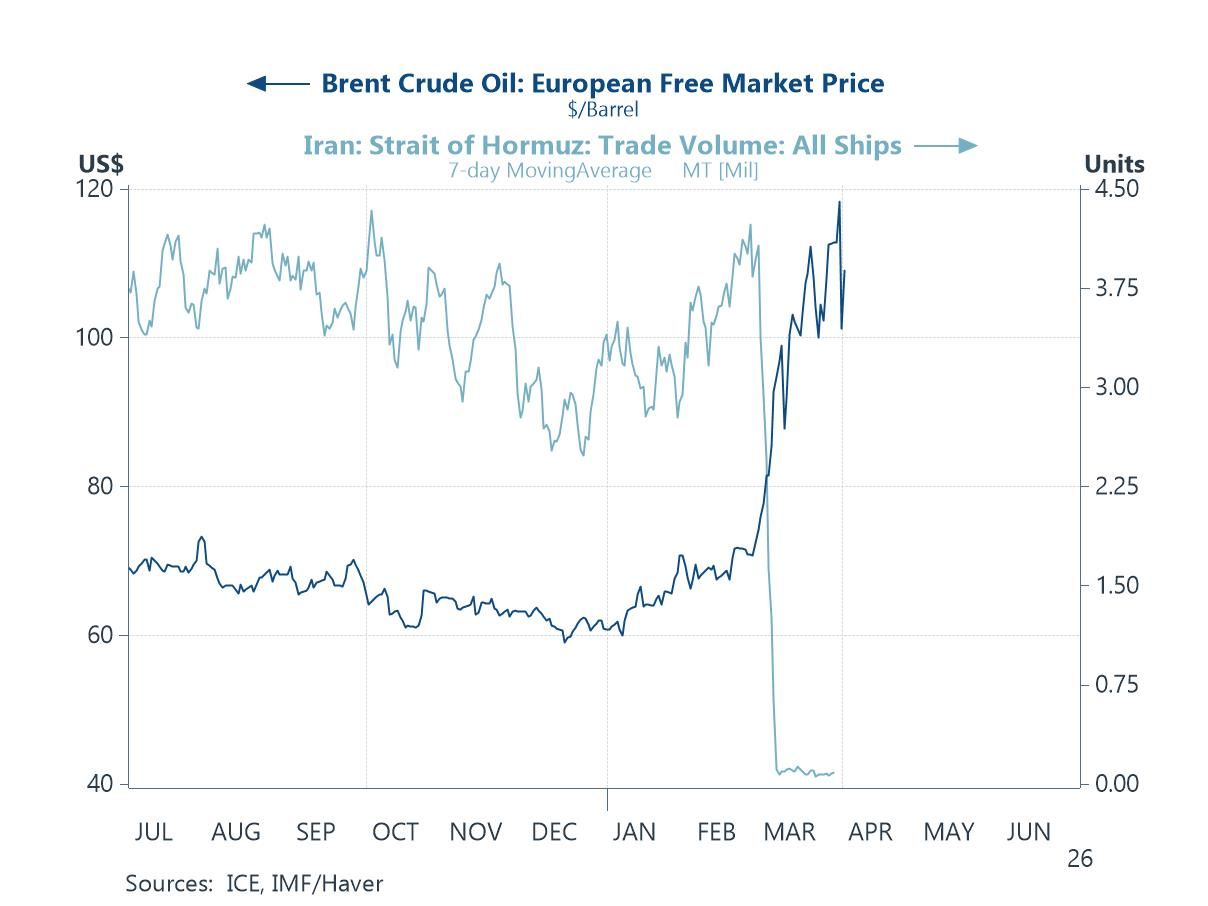

The Middle East conflict The Middle East conflict continues to rage, with IMF-tracked shipping volumes through the Strait of Hormuz still reduced to a trickle. Meanwhile, crude oil prices remain volatile, gyrating alongside shifting perceptions over how soon normal oil flows might resume. In reality, there is still little sign of a substantive resolution, and no agreement to fully reopen the strait appears imminent, suggesting that oil flows are likely to remain constrained at low levels in the near term. That said, some investors are closely monitoring developments following reports of discussions around a potential 45-day ceasefire, which could pave the way toward a more lasting resolution. Until then, and absent any meaningful supply relief, crude oil prices—and by extension, energy-related inflation—are likely to face continued upward pressure, particularly for oil-dependent, importing economies.

Chart 1: Brent crude oil price and Strait of Hormuz shipping volume

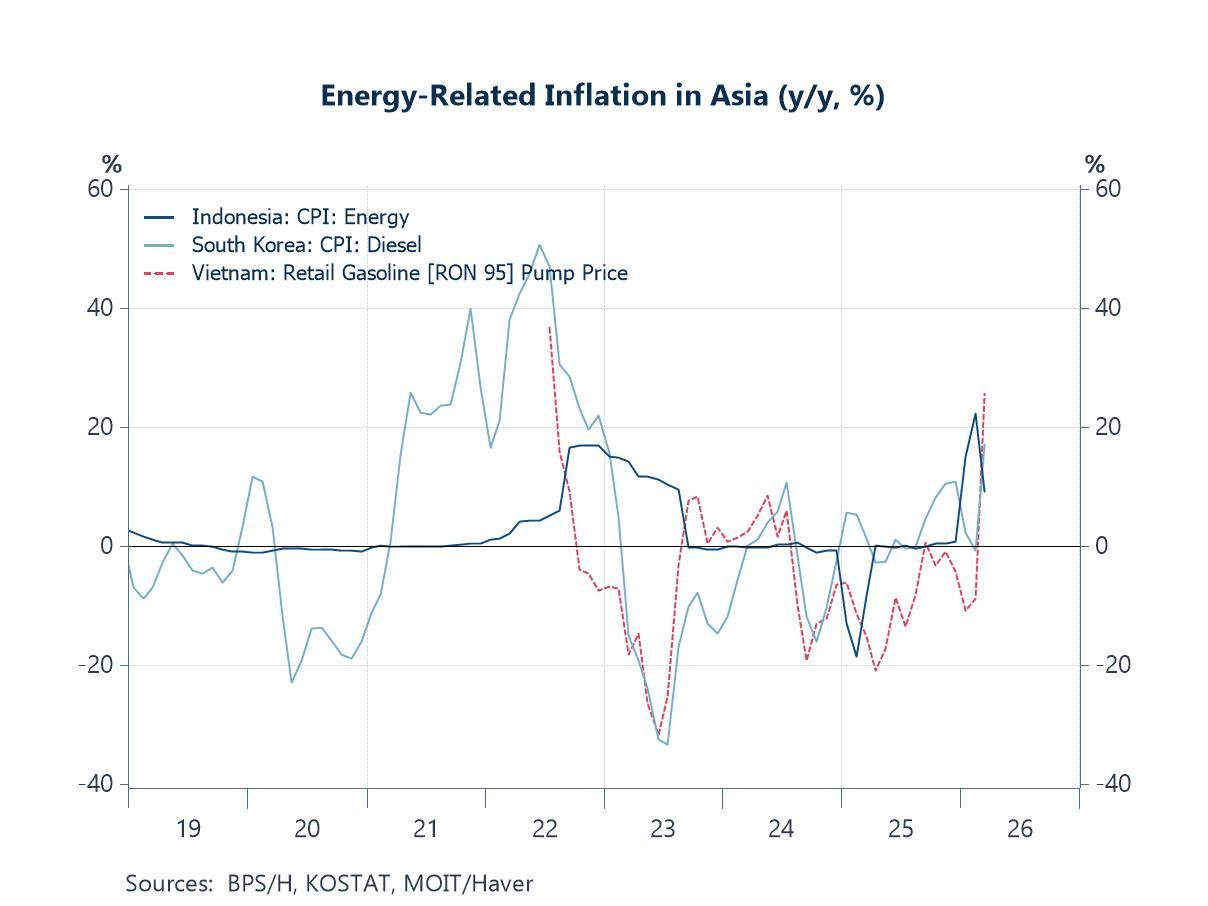

Initial price impacts The initial inflation concerns among policymakers and investors stemming from the surge in oil prices are now beginning to show up in the data, as illustrated in chart 2. The latest March readings—capturing the period after the onset of the Middle East conflict—already point to a sharp acceleration in energy-related prices on a year-ago basis. Indonesia’s energy CPI basket has risen by around 9%, while diesel prices in South Korea have jumped 17%. Vietnam’s retail gasoline prices have seen an even more pronounced increase, at roughly 25.6%. Given the scale of these price surges, and their direct impact on everyday essentials—particularly fuel for daily commutes and broader economic activity—governments across Asia have begun rolling out sizeable subsidy programmes. These measures, often implemented at significant fiscal cost, aim to cushion the burden on households and firms. For instance, South Korea’s finance ministry proposed a supplementary budget of around $17.3 billion in late March to support low-income households, youth, and businesses amid higher oil prices, with approval expected by April 10. Meanwhile, Indonesia has allocated approximately $22.4 billion toward energy subsidies and support for selected energy and utilities firms to help keep prices affordable.

Chart 2: Energy-related inflation in Asia

Consumer inflation expectations What policymakers are likely to focus on—beyond the immediate price impacts—is how the recent surge in oil prices feeds into inflation expectations. If left unanchored, these expectations could pose a far greater challenge than the supply-driven price shock itself, including reduced monetary policy effectiveness in reining in inflation and the risk of a self-fulfilling inflation cycle—though it is worth noting that such dynamics are not yet close to materialising. So far, there are some early, albeit inconclusive, signs that near-term consumer inflation expectations are beginning to drift higher in certain economies. As shown in chart 3, one-year-ahead inflation expectations edged up to 2.7% in March, while in Taiwan, consumer sentiment regarding domestic price trends over the next six months has turned notably more pessimistic relative to overall confidence.

Chart 3: South Korea and Taiwan consumer inflation expectations

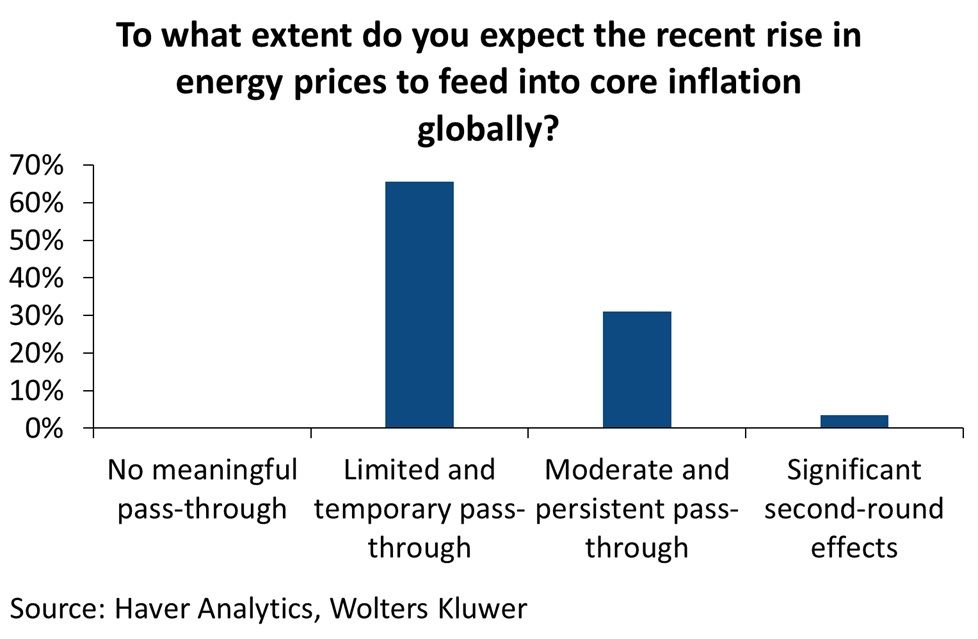

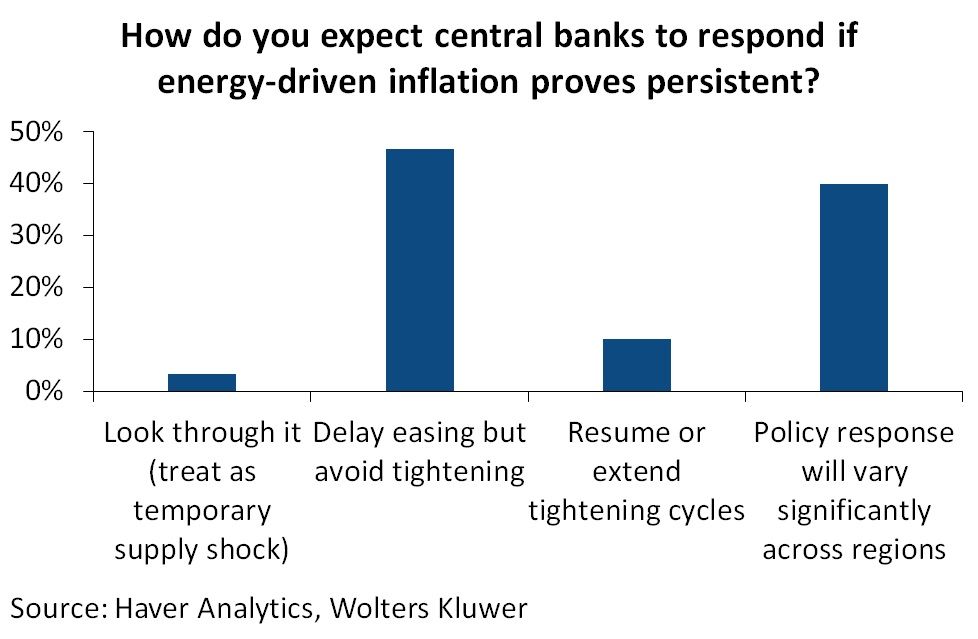

The latest Blue Chip survey Turning to investor perspectives on how higher energy prices may feed into inflation, our special questions in the latest Blue Chip Financial Forecasts (BCFF) survey offer some useful nuance. As shown in chart 4, around two-thirds of panellists expect only a limited and temporary pass-through from higher oil prices to core inflation. That said, a non-trivial minority (31%) anticipate a more moderate and persistent pass-through. This is notable given the focus on core inflation, and underscores how energy prices can generate second-round effects even in typically non-energy components, reflecting the pervasive role of energy in everyday economic activity—from manufacturing to the upkeep of a wide range of goods and services.

Chart 4: Blue Chip Financial Forecast special survey question on surged energy prices and core inflation

Delving deeper, we also asked panellists about their views on the prospective path of central bank policy should energy-driven inflation prove persistent. As shown in chart 5, responses broadly coalesce around two themes: central banks are likely to delay easing rather than tighten, and policy responses will vary meaningfully across regions. The former is already playing out to some extent in recent central bank decisions across Asia, with several explicitly citing the ongoing Middle East conflict as a reason to remain vigilant on inflation and refrain from easing policy prematurely. As for the latter, there are already signs of divergence in how different central banks are approaching the situation.

Chart 5: Blue Chip Financial Forecast special survey question on energy-driven inflation and policy

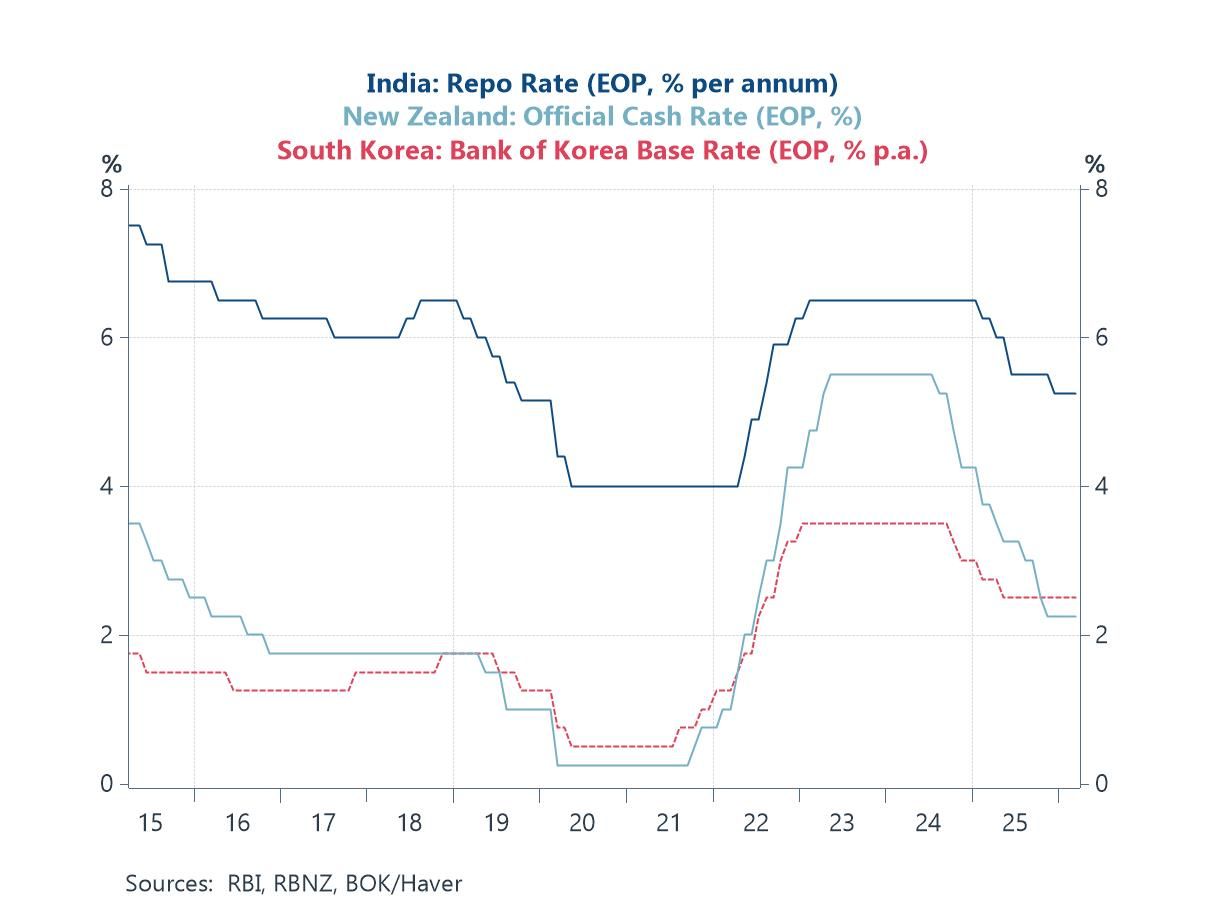

The week ahead Looking to the week ahead, there will be ample opportunities to assess whether investor expectations for central bank policy moves play out across Asia, with several rate decisions due—most notably in India, New Zealand, and South Korea. Also on the docket are China’s March CPI print and a range of Japan-related releases. Policymakers are likely to remain focused on balancing inflation control with supporting growth and maintaining currency stability. For now, and absent offsetting domestic factors, expectations for further near-term easing have been tempered by rising inflation risks. In China, recent CPI readings point to a modest pickup, while producer price deflation has begun to ease after a prolonged period of weak or negative inflation.

Chart 6: India, New Zealand, and South Korea policy rates

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief

U.K. Headline and Core Inflation Rates Slow Sequentially as BOE Gets Ready to Meet