French IP Waffles

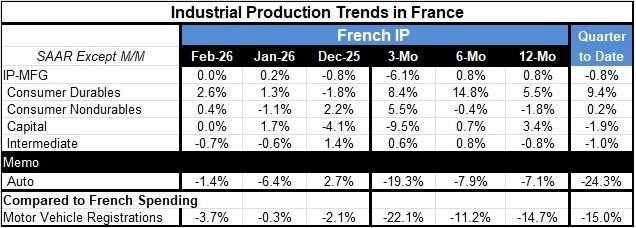

French manufacturing industrial production was flat in February after a January rebound; output rose by 0.2% following a 0.8% decline in December.

The components of industrial production in February showed 2.6% increase in consumer durables, a 0.4% increase in consumer nondurables, flat output from capital goods, and a 0.7% month to month decline in intermediate output.

Sequentially, French output had been growing at a slow, steady pace of 0.8% at an annual rate over both 12 months and six months, but then slipped to a 6.1% contraction at an annual rate over three months. Consumer durable goods output on this span shows consistent increases, but there are no trends to clear acceleration or deceleration. Consumer nondurables trace an accelerating path of moderate means from -1.8% over 12 months, to -0.4% over six months, and then rising at a 5.5% annual rate over three months. Capital goods output is moving in the opposite direction, growing by 3.4% over 12 months, slowing to a 0.7% annual pace over six months, and then contracting at a 9.5% annual rate over three months. Intermediate goods output is falling at 0.8% pace over 12 months, but then it switches to an expansion rate of 0.8% over six months and 0.6% and over three months. There's nothing remarkable about these patterns, except there's some acceleration, some deceleration, and a lot of mulling about at low growth rates.

As a separate item, French auto production is slipping and decelerating, falling by 7.1% at an annual rate over 12 months, falling at a 7.9% pace over six months, and then plunging at a 19.3% annual rate over three months. On these same horizons, motor vehicle registrations fall by 14.7% over 12 months; the weakness pares back to an 11.2% annual rate decline over six months, and then it steps up to a 22.1% decline at an annual rate over three months. French demand for autos is not in good shape.

In the quarter to date—now two months into the first quarter—manufacturing industrial production is falling at a 0.8% annual rate. That pace is boosted by 9.4% annual rate gain in consumer durables output but restrained by just a 0.2% annual rate increase in consumer nondurable goods. Capital goods output is falling at a 1.9% annual rate, while intermediate goods output is falling at a 1% annual rate. Also in the quarter to date, automobile production is plunging at a 24.3% annual rate, while on the demand side, motor vehicle registrations are falling at a 15% annual rate.

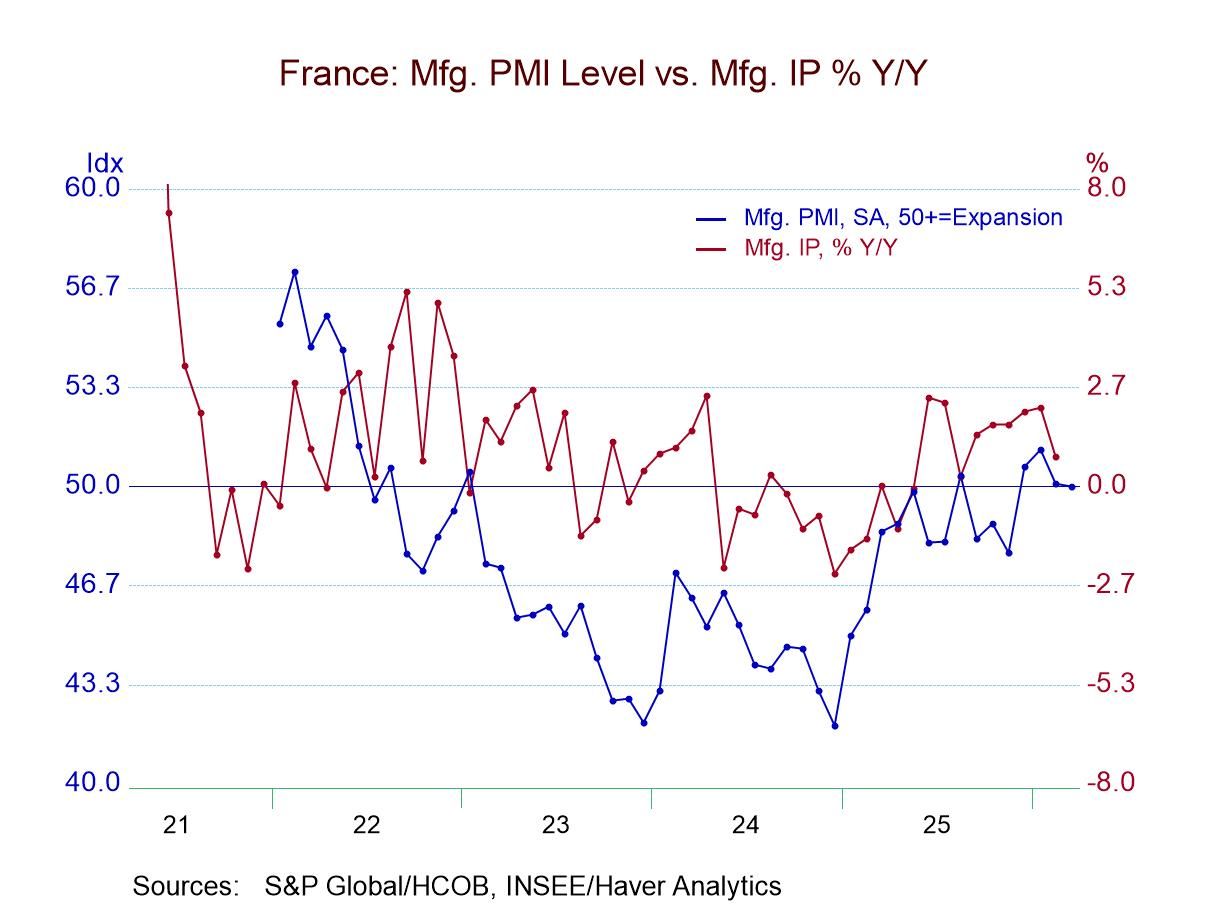

French manufacturing data are somewhat confusing. The chart shows that the industrial production trend has been showing consistent increases over 12 months, but it has recently been pulling back relatively sharply. On the other hand, the manufacturing PMI for France has been consistently negative going back to mid-2022 and only in early 2026 has the manufacturing PMI been posting some values above the 50% mark, indicating that output was starting to actually expand. In March, the PMI reading for manufacturing has slipped back by the thinnest margin below the 50% mark.

Of course, events in the Middle East make everything more speculative, with the war effectively closing the Strait of Hormuz and no certainty about how or when that is going to be sorted out. In the meantime, the potential threat of ongoing oil price pressures has put both the ECB and the Bank of England in a position to be more wary with policy, and they warned markets about the potential for rate hikes as soon as their next meetings are engaged. That also raises questions about the outlook for growth. But we continue to track and chronicle trends in the data. It's also quite clear that we could have events that will play out that could completely undermine these trends before they get a chance to run to conclusion. It's an important time to be wary and watch all developments—a lot is in play.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia