Global| Apr 02 2026

Global| Apr 02 2026Global Manufacturing PMIs Stall—Will It Get Worse?

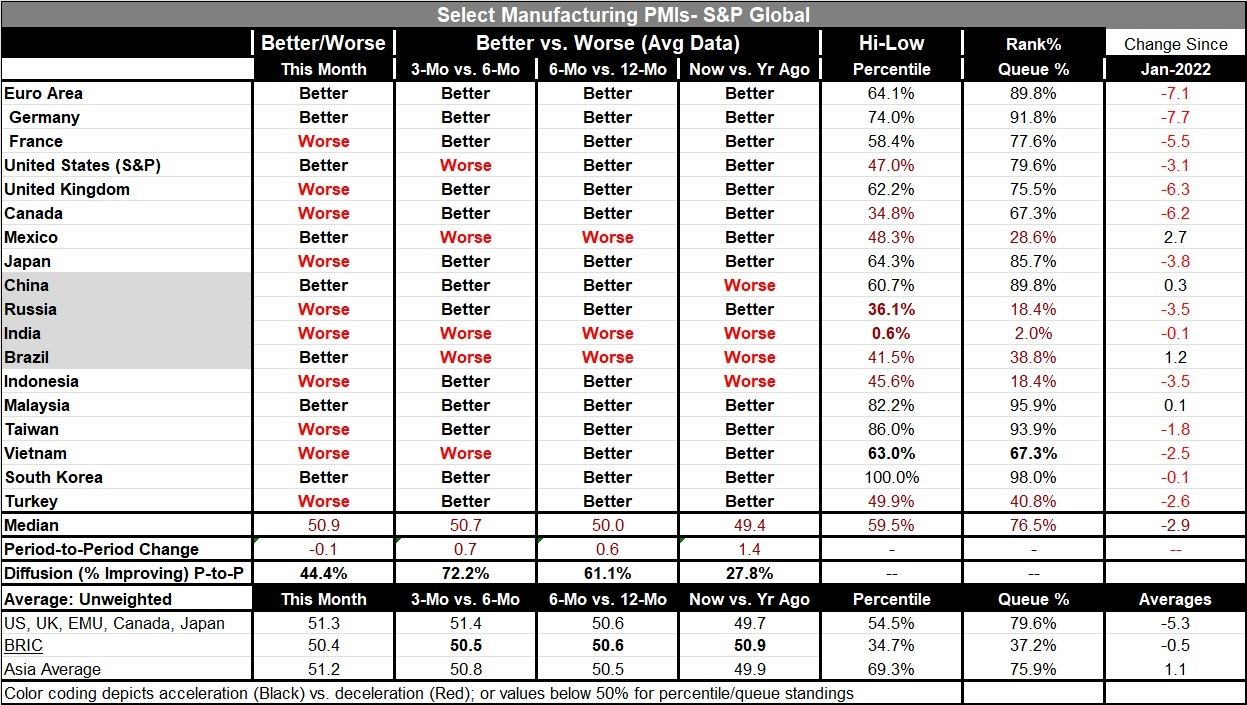

The S&P manufacturing PMIs for March showed improvements in 44.4% of the 18 reporters. The median reading for the month was at 50.9, indicating that expanding output was the median reading through the period. The median change showed a small step back of 0.1 diffusion points month-to-month.

Sequentially, looking at average yearly activity compared to a year ago, six months compared to 12 months, and three months compared to six months, we see progress in train. For three months compared to six months, the proportion of reporters showing improvement is 72.2%. For these reporters, over six months compared to 12 months, there is a 61.1% improvement proportion, while for 12 months compared to 12 months ago, there is only a 27.8% improvement.

The median reading over three months on average is 50.7, while the median reading over six months is 50.0 and the median reading over 12 months is 49.4. These readings show a very slow but steady improvement in manufacturing over this horizon.

In addition, we calculate the queue percentile standings for each reporter—that is, the level of the current diffusion index compared to all of the observations back to January 2022, expressing the final number as the percentile standing for the current month in that queue. On that basis, the median percentile standing for this group of reporters is 76.5%. It tells us that the median standing is in the top 25 percentile of all the readings since January 2022 to date. That's a reasonably good result. For the euro area, the queue percentile standing is at the 89.8 percentile, while for Germany it's at its 91.8 percentile. For the Monetary Union and for Germany, the current numbers are some of the best we've seen during this period. However, that doesn't mean that they're necessarily stellar readings.

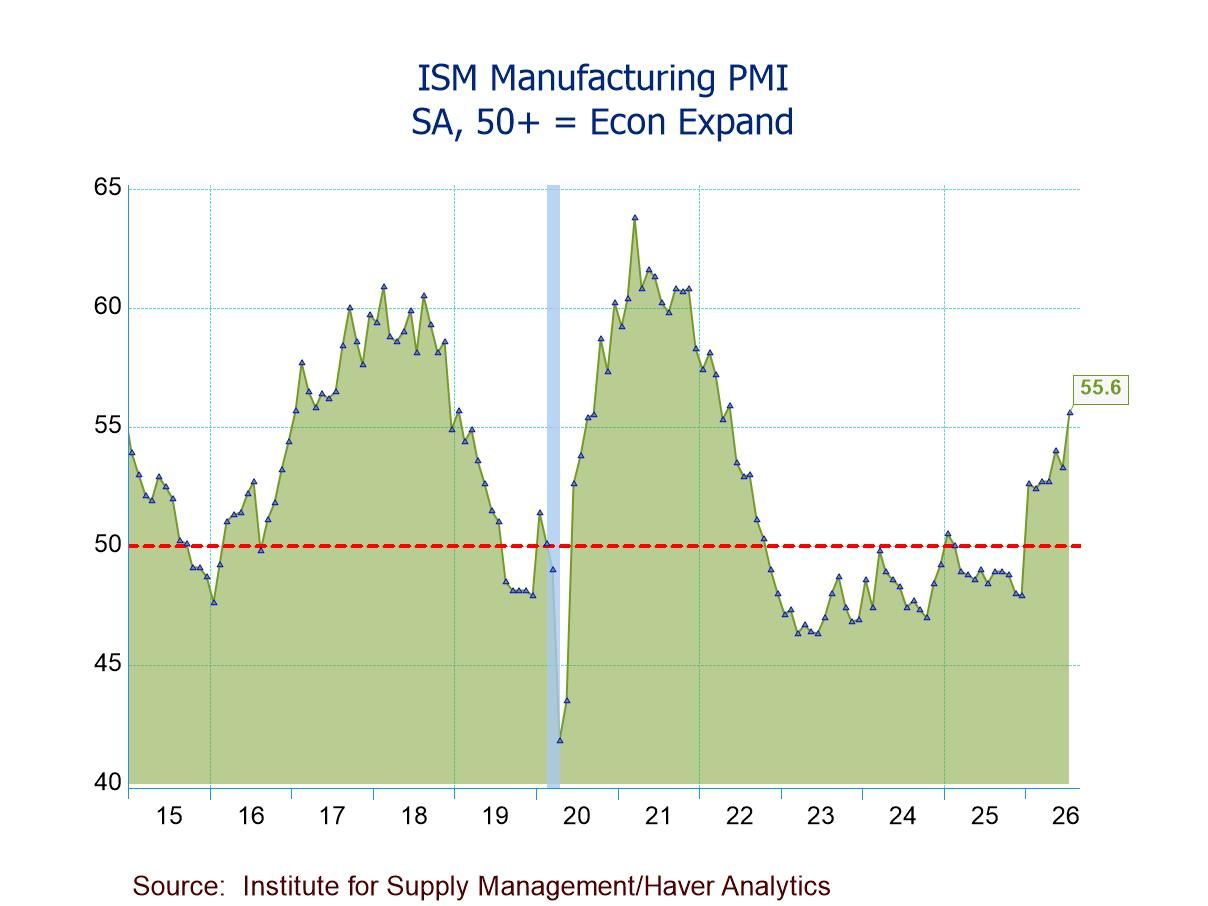

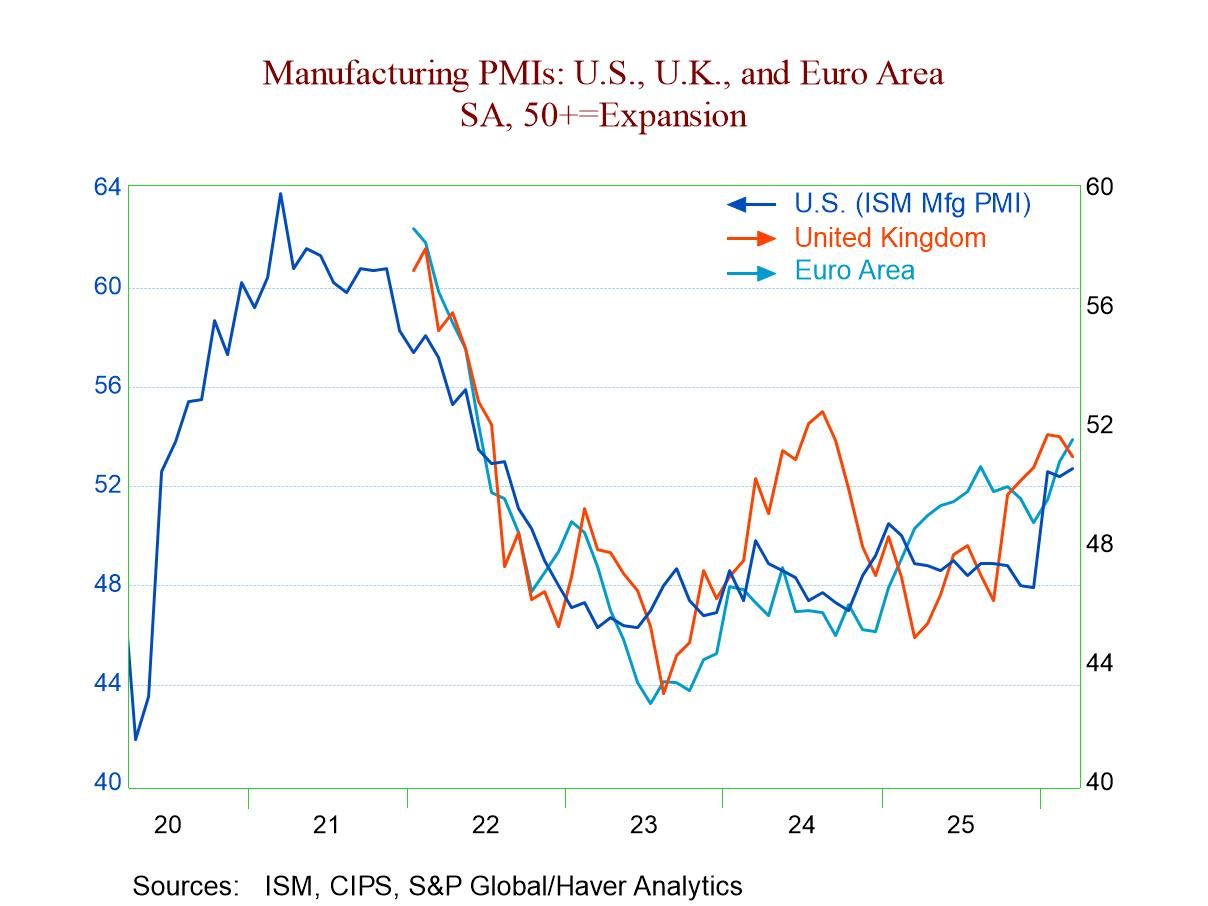

PMI diffusion vs. PMI rank standings German diffusion in manufacturing is 52.2 in March; for the EMU it is 51.6. Germany posts the fourth-highest PMI rank standing and the fifth highest raw standing in March. The highest standing among all reporters is 52.6 from South Korea. This is a period in which no country was posting very strong manufacturing results. In fact, the United States, with a manufacturing PMI rank standing of 79.6, has a diffusion reading in March just a tick below Germany’s whose queue standing at 91.8 seems miles ahead of the U.S.—but it isn’t. Remember that the queue standings are about relative positioning.

Looking at the details, we see that below-median rank readings were logged by Mexico, Russia, India, Brazil, Indonesia, and Turkey. The Asian markets and developing economies seem to have a harder time working up to the standards achieved by other countries.

We also have averages by certain groups of countries. For example, the U.S., the U.K., the Monetary Union, Canada, and Japan—an expanded G10 groping—had an average reading of 51.3 in March, and for that group of countries, the improvements have been steady from 12 months to six months to three months. For the BRIC countries in March, the average standing was 50.4, and for that group there has been a very slight ongoing erosion. For the Asian group, on average, the March reading is 51.2, and there has been a progression to stronger readings from 49.9 over 12 months to 50.5 over six months and to 50.8 over three months.

On balance, manufacturing was quite uneven in March; however, there's a progression of improvement that is still in place. But with rising oil prices, war in Iran, and lots of knock-on effects to supply trains, it's likely that these readings are going to fall on harder times in the months ahead—unless the Iran war can be wrapped up in very, very, short order. According to the Baltic Dry index, there hasn't been much reduction in global shipping of dry goods. That index excludes oil and other wet goods shipments that clearly have been impeded. However, giving it more time, we may see that the dry index begins to show some difficulties.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief