Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

by:Andrew Cates

|in:Economy in Brief

Summary

Recent de-escalation signals in the Middle East have offered some relief to markets, but the economic aftershocks from the earlier escalation are still feeding through—particularly via energy prices and heightened geopolitical risk. Crucially, these shocks are not hitting a clean cyclical backdrop. Instead, they are amplifying a set of pre-existing supply-side pressures—fragmented trade, strained supply chains, and a more complex policy environment—that have been building for some time. The charts this week pick up that theme. Forward-looking sentiment indicators suggest global growth has lost some momentum, even if activity remains in expansion territory (chart 1). At the same time, broader measures of uncertainty remain elevated (chart 2), while supply chain stress is once again moving higher, reinforcing the idea that disruption is becoming more structural (chart 3). Financial markets are reflecting this shift, with increased uncertainty around the future path of policy rates (chart 4), and survey evidence pointing to a more fundamental challenge around the credibility and transmission of monetary policy itself (chart 5). And yet, there are some offsets. Despite the recent spike in oil prices, medium-term inflation expectations—at least in the US—remain relatively well anchored (chart 6). Even so, the overall message is one of a more fragile, supply-driven cycle—where shocks like the Middle East do not just disrupt the outlook, but intensify the underlying constraints shaping the global economy.

The global business cycle Our first chart this week looks at the March flash composite PMIs—one of the earliest sentiment reads on how the Middle East crisis, which escalated at the end of February, is feeding through into global activity. The message on momentum is soft. Three-month changes are generally weak—and in several cases negative—pointing to a modest cooling in growth as we moved into March. But the level still matters. Most major economies remain in expansion territory (above 50), including India, the US, UK, euro area and Japan. So while growth has lost a little pace, it has not collapsed. The main exceptions are France and Australia, where PMIs are now below 50, signalling contraction. Elsewhere, this looks less like a sharp shock and more like an early loss of momentum—potentially just the first pass of the geopolitical impact rather than the full effect.

Chart 1: Flash composite PMIs for March — levels and 3-month changes

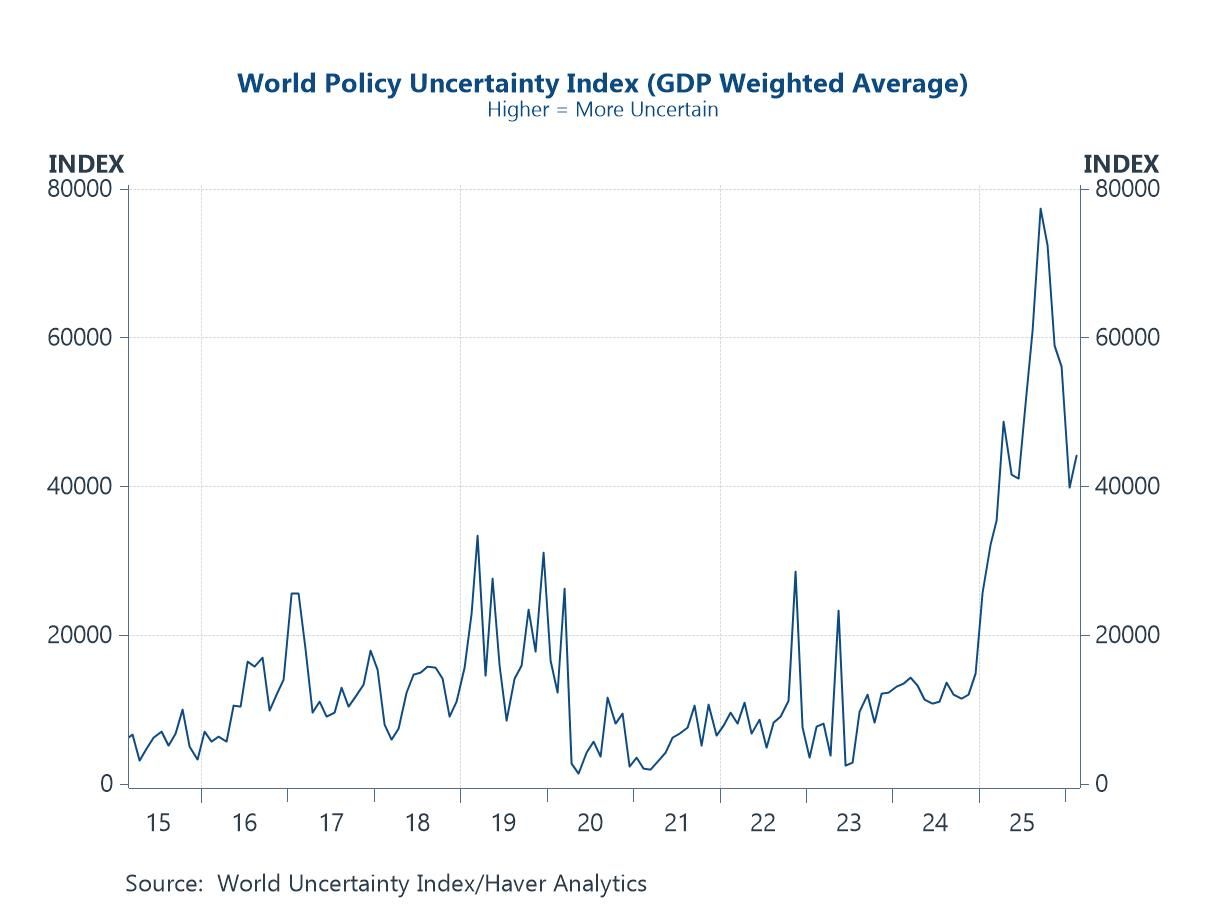

The age of uncertainty Our second chart underscores just how elevated—and persistent—global policy uncertainty has become. While spikes in uncertainty are nothing new, what stands out here is the shift in regime: rather than brief, event-driven surges, uncertainty now appears to be running at structurally higher levels, punctuated by sharper geopolitical shocks—most recently the escalation in the Middle East. This matters because uncertainty is no longer just cyclical noise around the business cycle; it is increasingly a feature of the economic backdrop itself. A more fragmented geopolitical order, the weaponisation of trade and finance, the energy transition, and more activist—and at times less predictable—fiscal and industrial policy are all contributing to a world where firms and households face a more complex and less stable decision-making environment.

Chart 2: World Policy Uncertainty Index

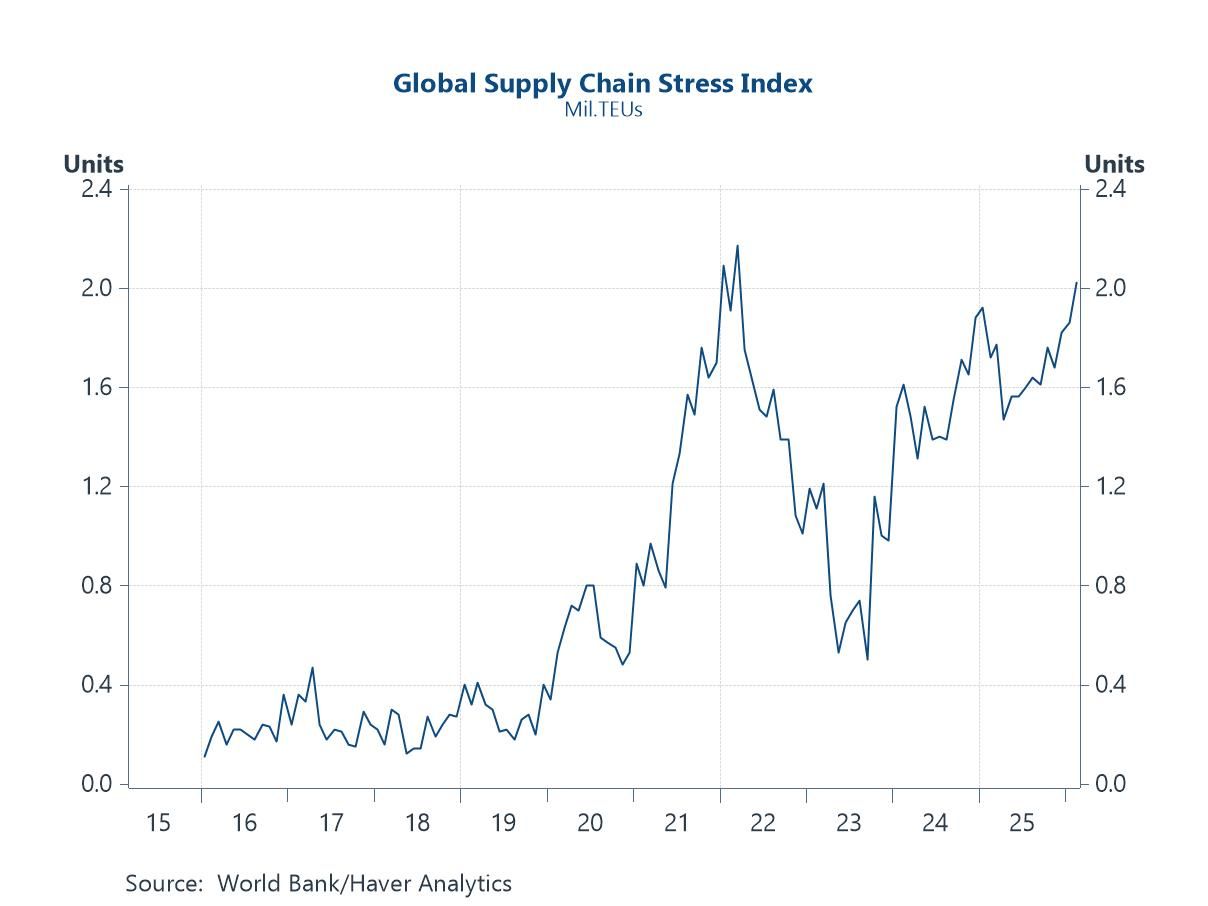

Global supply chains under strain A key channel through which this elevated uncertainty is manifesting is in global supply chains. After easing back from the pandemic-era extremes, supply chain stress is once again trending higher—and, more importantly, appears to be settling at a structurally elevated level. The drivers are increasingly familiar. Geopolitical fragmentation and trade tensions are reshaping production networks; conflict-related disruptions (including in the Middle East) are affecting key shipping routes; and firms are deliberately trading efficiency for resilience via reshoring, friend-shoring and inventory rebuilding. Layer on top the energy transition—which is reconfiguring commodity flows—and the result is a system that is inherently more complex and arguably more prone to disruption. Methodologically, the index captures these pressures by tracking the movement of large, globally significant container vessels (Panamax and above, >4,000 TEU) using shipping data. In other words, it focuses on the core arteries of global trade rather than regional flows—making the recent rise all the more telling.

Chart 3: World Bank Gauge of Global Supply Chain Stress

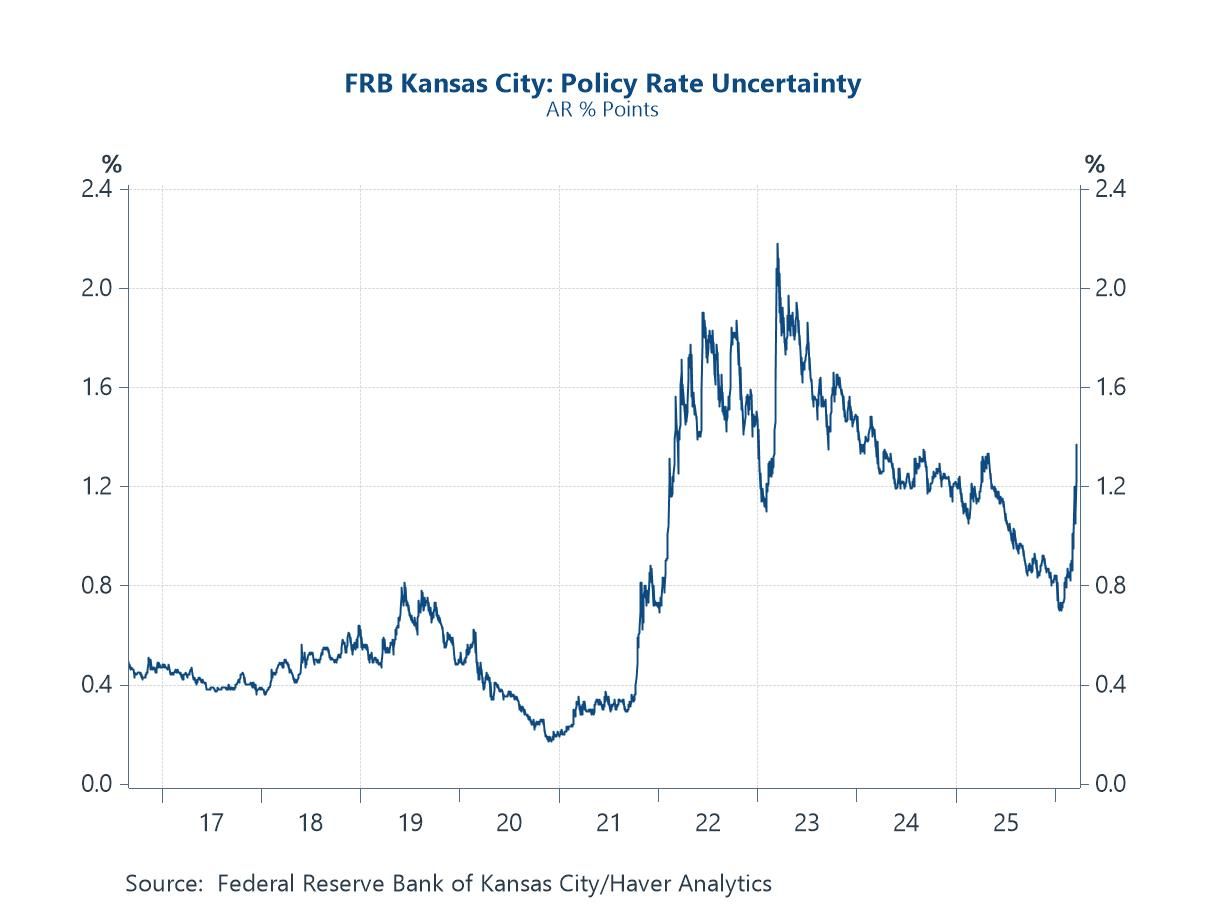

Monetary policy in an uncertain world It almost goes without saying that, in a world of greater supply-side complexity, uncertainty around the path of monetary policy has also moved higher. The challenge for central banks is clear: they are attempting to steer demand in an environment where inflation is increasingly being driven by supply shocks—energy, geopolitics, supply chains—rather than traditional cyclical forces. That makes the reaction function harder to read, both for policymakers and markets. This is reflected in the Kansas City Fed’s measure of policy rate uncertainty, which has risen markedly since the pandemic and remains elevated. The index is derived from market pricing and captures the dispersion of expectations around where short-term U.S. interest rates will be one year ahead—effectively a real-time gauge of how confident (or not) markets are about the policy outlook. In that sense, monetary policy uncertainty is no longer just about timing or calibration. It reflects a deeper question about effectiveness: how central banks respond in a world where the sources of inflation—and the structure of the economy itself—have fundamentally shifted.

Chart 4: FRB Kansas City Policy Rate Uncertainty

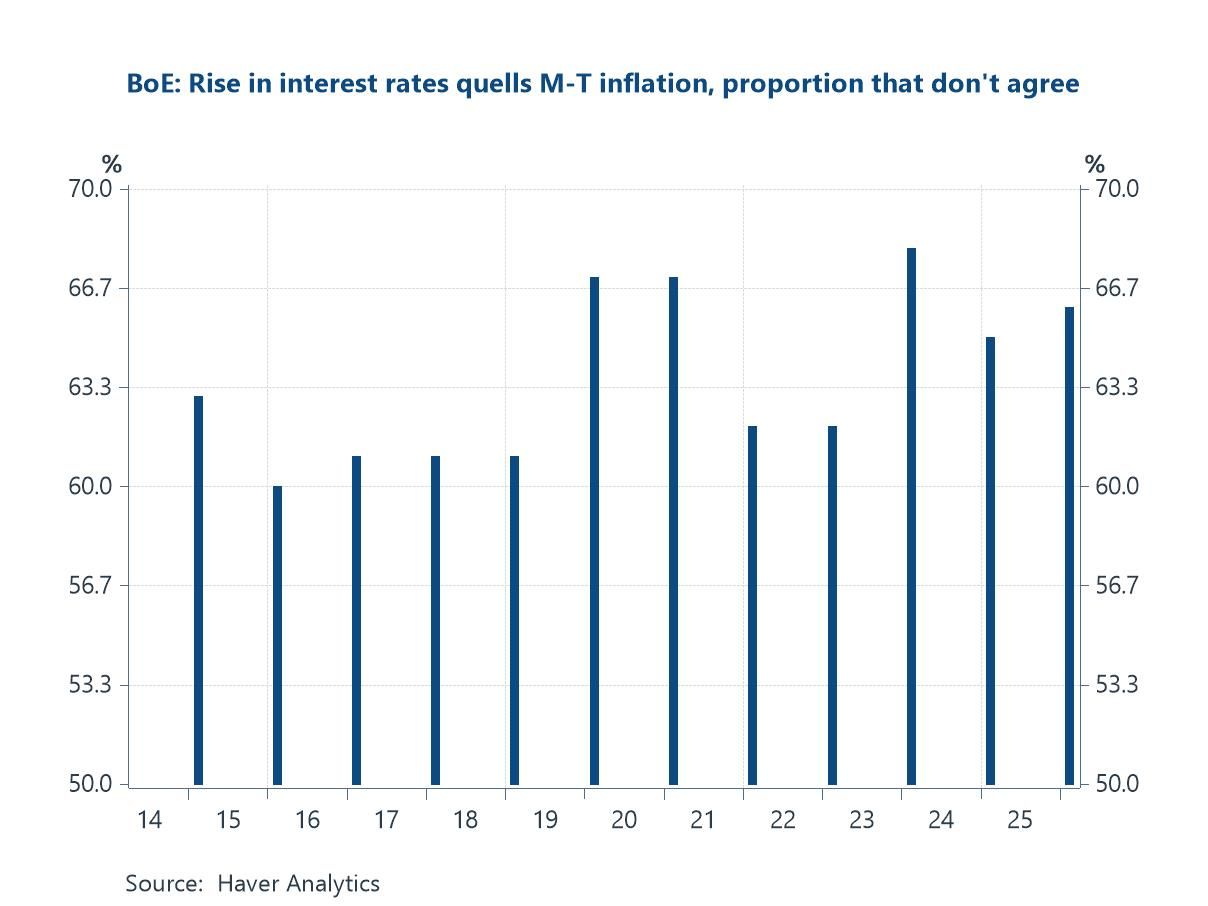

The limits of monetary policy This brings us to a more subtle—but arguably more important—challenge for policymakers: credibility. The Bank of England/Ipsos inflation attitudes survey shows that a consistently large share of respondents do not believe that higher interest rates will slow inflation over the medium term. In other words, the core transmission mechanism of monetary policy—working through expectations—is being called into question. That matters because if households don’t see rate hikes as disinflationary, then managing inflation expectations becomes significantly harder. Instead of anchoring expectations, tighter policy may even be perceived as part of the inflation problem itself—raising mortgage costs and reinforcing the sense that prices are still rising. In the context of a supply-constrained world, this is a serious complication. Monetary policy is being asked to do more, in an environment where its effectiveness may be diminished—and where expectations are increasingly shaped by lived experience (energy, food, housing) rather than central bank signalling.

Chart 5: BoE/Ipsos inflation attitudes survey — share disagreeing that higher rates reduce inflation

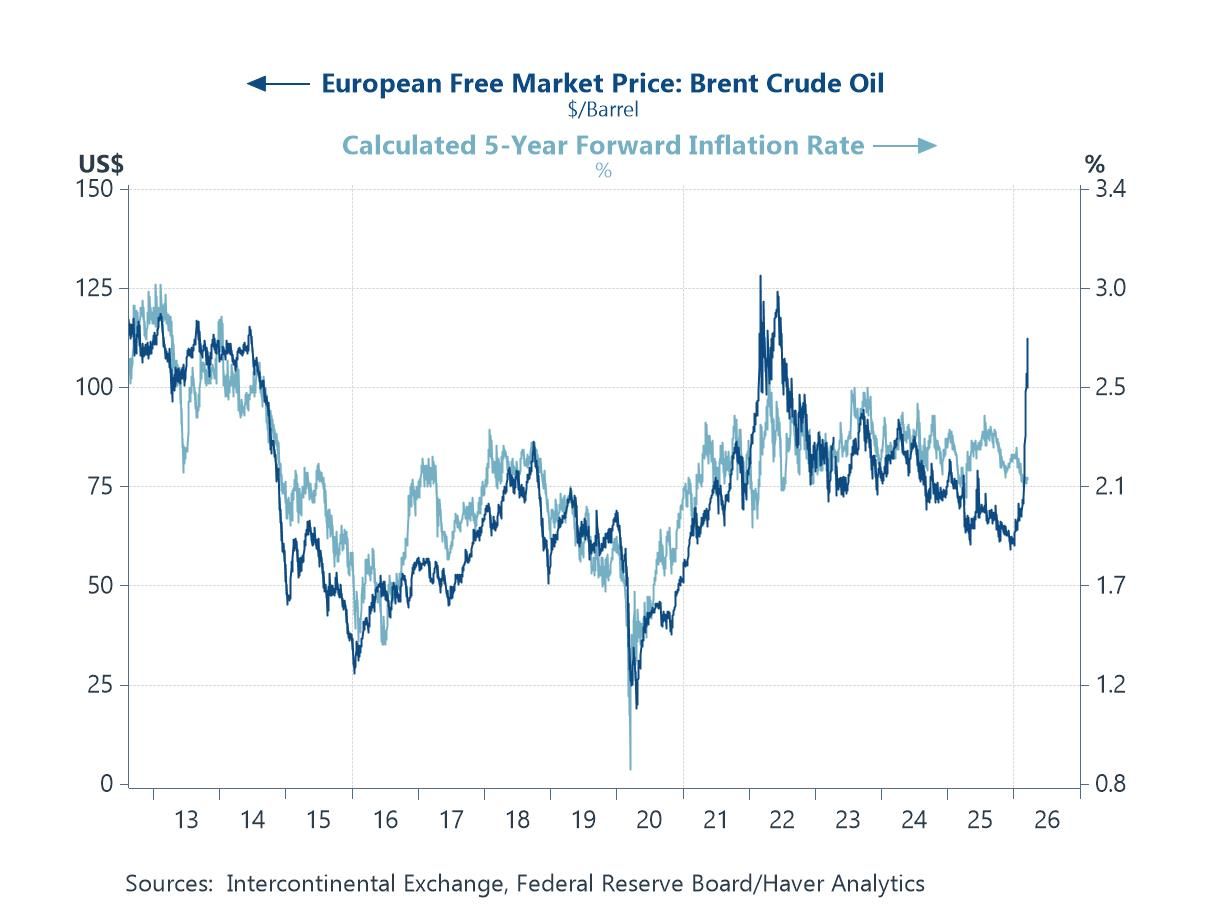

Anchored inflation expectations Finally, and on a slightly more reassuring note, markets are not (yet) extrapolating the recent energy shock into a sustained inflation problem. Oil prices have spiked sharply in response to the latest Middle East escalation, but US medium-term inflation expectations—proxied here by the 5-year forward—have remained relatively contained. That divergence matters. It suggests that, for now at least, markets still see energy-driven inflation as temporary rather than systemic. In other words, while the supply side remains volatile, the broader inflation regime has not become unanchored. In the context of everything discussed above—higher uncertainty, strained supply chains and more complex policy trade-offs—that resilience in expectations offers a degree of comfort. It implies that credibility, while challenged, has not been lost—and that the system still has some anchors, even in a more fragmented and supply-constrained world.

Chart 6: Brent crude oil vs US 5-year forward inflation expectations

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief