Global| May 14 2019

Global| May 14 2019ZEW Global Expectations Are Set Back

Summary

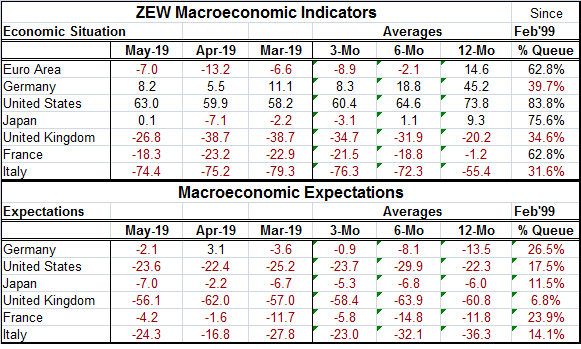

ZEW macro-indicators of current conditions show some strengthening month-to-month. However, only the U.S. has a queue standings anything close to strong (in the 80th percentile). Japan has a firm standing in its 75th percentile with [...]

ZEW macro-indicators of current conditions show some strengthening month-to-month. However, only the U.S. has a queue standings anything close to strong (in the 80th percentile). Japan has a firm standing in its 75th percentile with the euro area and France in their 60th percentile also solid but less firm standings. Germany, the U.K. and Italy have queue standings in the bottom 30th percentile range of their respective historic queues of data.

ZEW macro-indicators of current conditions show some strengthening month-to-month. However, only the U.S. has a queue standings anything close to strong (in the 80th percentile). Japan has a firm standing in its 75th percentile with the euro area and France in their 60th percentile also solid but less firm standings. Germany, the U.K. and Italy have queue standings in the bottom 30th percentile range of their respective historic queues of data.

Moreover, all the country/region moving averages are weakening from 12-months to six-months to three-months. ZEW experts see widespread deterioration in current macroeconomic conditions.

Expectations are negative up and down the line. But contrarily, they show some gradual improvement – except for the U.S. where deterioration is quite modest. There is some significant improvement in Germany, France and Italy. Expectations standings are all below the 50% mark (below their respective medians). Expectations coalesce around the 25th percentile level or lower. These are very weak expectations.

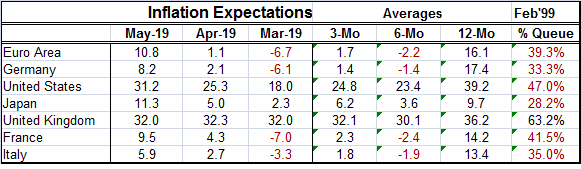

Inflation expectations are below their median readings everywhere except in the U.K. But the U.K. readings are holding steady. Elsewhere inflation expectations already 'below average' are easing further from 12 months to three-months. But all countries/regions except the U.K. show inflation expectations rising in May compared to the last three-month average. Despite the broader trends, the short-term expectations for inflation are shifting.

This shifting precedes news on the trade front where talks between the U.S. and China have led to increased tensions, concerns and most of all increased tariffs. While some are concerned that tariffs will bring inflation, others are more concerned that a trade war will weaken economic conditions globally. We don't see any of that playing out in anticipation in the ZEW Survey, but it will bear watching if the U.S. and China talks drag on through next month.

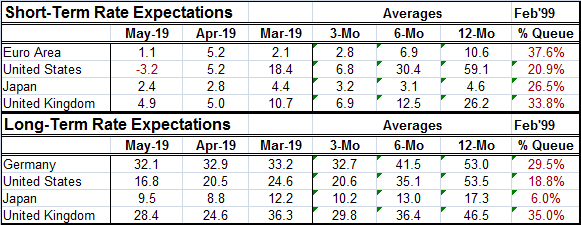

Short- and long-term interest rate expectations continue to be low and are all well below their medians. Short-term interest rate expectations in the U.S. began braking lower sharply in January. Euro area expectations have slipped steadily on that same timeline but not by as much as for the U.S. Japan's expectations have been steady while in the U.K. they have slipped moderately. Long-term rate expectations have been falling too. The queue standings for long rate expectations are lowest for Japan but also are low in the U.S. Both Germany and the U.K. have standings below their respective medians, well below them.

The ZEW survey continues to show relatively solid current conditions with some obvious variations. Expectations are negative but have lost some of their downward momentum. Inflation expectations have been falling but have recently reversed slightly. And interest rate expectations continue to be very low for both long- and short-term rates. The most identifiable shift this month is the upturn in inflation expectations in May compared to April, a reversal of a long trend that is apparent in the sequential readings for three-months, six-months and 12-months. Just because expectations are changing, that does not mean that conditions will be changing. That is the thing to watch out for especially with trade frictions apparent and more to come.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief