Global| Feb 11 2009

Global| Feb 11 2009U.S. Trade Deficit Narrowed Further With Global Recession and Lower Oil Prices

by:Tom Moeller

|in:Economy in Brief

Summary

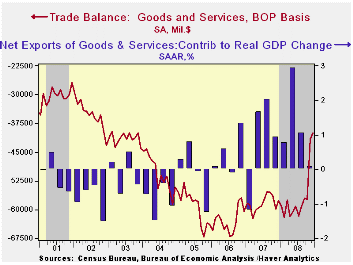

The December U.S. foreign trade deficit narrowed sharply to its shallowest since late 2003 as the global recession continued and oil prices fell further. The decline to $39.9B from an upwardly revised November deficit of $41.6B fell [...]

The December U.S. foreign trade deficit narrowed sharply to its shallowest since late 2003 as the global recession continued and oil prices fell further. The decline to $39.9B from an upwardly revised November deficit of $41.6B fell short, however, of Consensus expectations for a deficit of $36.0B.

For all of 2008, the trade deficit narrowed to $677.1B from the 2007 deficit of $700.3B. The latest was the lowest deficit since 2003. At 4.7%, last year's deficit as a percentage of GDP also was the lowest since 2003.

Adjusted for price inflation the trade deficit in goods narrowed last year as well. It fell more than $10.0B versus 2007 to 534.3B as real exports rose 6.5%, lifted by strength early in the year, and real imports fell 3.4%.

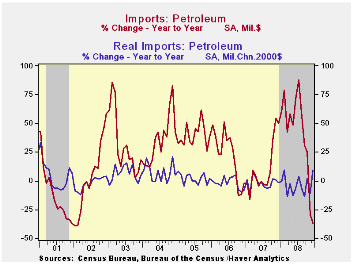

Lower oil prices caused December petroleum imports to drop by 6.7%. However, they rose by more than one-third for the full year due to the gains in early 2008. For December, in volume terms, petroleum imports rose a strong 23.3% (+9.6% y/y), but they were down for the full year. The quantity of crude petroleum imports made up all of their November decline with an 18.3% rise (+7.4% y/y). Moving the other way, of course, was the average price per barrel of crude oil which fell to $49.93 (-39.7% y/y) from a high of $124.7 in July.

Reflecting the U.S. recession, measured in chained-2000 dollars, nonoil imports fell 5.6% (-13.7% y/y) after a similar decline during November. Real imports of nonauto consumer goods fell 1.3% (-10.3% y/y) to their lowest level since early 2006. The chained-dollar value of imports of automotive vehicles & parts fell a sharp 9.2% (-28.8% y/y) and real imports of nonauto capital goods dropped 4.1%, down 11.1% from December of 2007.

Services imports slipped 0.4% (+3.3% y/y). Travel imports made up most of a November drop with a 1.6% increase (+0.7% y/y) while passenger fares again fell hard, by 1.5% but they were up 5.7% year-to-year. That strong year-to-year was reduced from the 20.5% increase early last year.

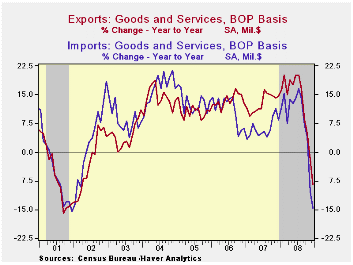

Recessions abroad lowered U.S. exports of goods for the fifth consecutive month. The 8.5% decline (-12.9% y/y) was the fifth in row. Adjusted for prices, chained-dollar goods exports fell 6.0% (-8.5% y/y) as real exports of capital goods declined 1.4% (-9.1% y/y) for the fourth consecutive monthly drop. Exports of nonauto consumer goods fell a huge 5.8% (-4.7% y/y) and they are off 16.7% during the last five months. Real exports of automobiles & parts registered another double digit decline with a 14.0% drop and they're off by more than one-third during the last five months.

Nominal exports of services slipped 0.4% (+1.8% y/y) for the fourth consecutive monthly drop. Travel exports made up 1.0% (-0.4% y/y) following three months of sharp decline. Passenger fares also rose by a slight 0.7% (0.7% y/y).

The U.S. trade deficit in goods with China narrowed again, to $19.9B, the smallest since March. For the whole year the deficit deepened, however, to $266.3 billion. Exports to China last year declined by nearly one-quarter, December-to-December, while imports fell just 2.2% y/y. The trade deficit with Japan narrowed m/m to $5.3B and for the whole year it narrowed to $72.7B which was the shallowest since 2003. Exports to Japan rose 6.2% during all of last year while imports fell 4.3% after a 1.8% decline during 2007.

Federal Reserve programs to strengthen credit markets and the economy is yesterday's testimony by Fed Chairman Ben S. Bernanke and it can be found here.

| Foreign Trade | December | November | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| U.S. Trade Deficit | $39.9 | $41.6B | $57.6B (12/07) | $677.1 | $700.3 | $753.3 |

| Exports - Goods & Services | -6.0% | -6.0% | -8.4% | 12.0% | 13.0% | 13.5% |

| Imports - Goods & Services | -5.5% | -11.9% | -14.7% | 7.4 | 6.1% | 10.8% |

| Petroleum | -6.7% | -36.2% | -36.5% | 37.0 | 9.4% | 20.1% |

| Nonpetroleum Goods | -6.4% | -7.6% | -13.1% | 1.3% | 4.8% | 9.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief