Global| May 13 2004

Global| May 13 2004U.S. Retail Sales Moderate

by:Tom Moeller

|in:Economy in Brief

Summary

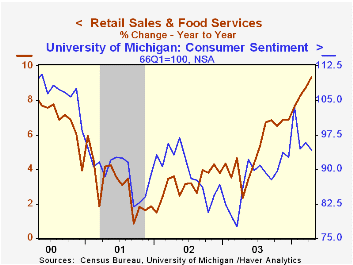

Retail sales eased 0.5% in April following little-revised jumps of 2.0% and 1.0% during the prior two months. Consensus expectations had been for a 0.1% dip. Retail sales excluding motor vehicles & parts dealers matched Consensus [...]

Retail sales eased 0.5% in April following little-revised jumps of 2.0% and 1.0% during the prior two months. Consensus expectations had been for a 0.1% dip.

Retail sales excluding motor vehicles & parts dealers matched Consensus expectations and eased 0.1% following an upwardly revised 1.8% jump in March.

The easing of prior sales strength was fairly broad based last month. Clothing and accessory store sales fell 2.0% (+8.2% y/y) following a downwardly revised 0.8% gain in March.Sales at general merchandise stores fell 0.8% (+7.2% y/y) after a 0.4% March gain. Strength was exhibited by sales of furniture/home furnishings & electronics/appliances which rose 0.7% (10.3% y/y) after an upwardly revised 1.2% March increase.

Sales of building materials, garden equipment & supply dealers (20.4% y/y) dipped 0.7% following the 11.0% m/m March surge.

Motor vehicle dealers' sales fell 1.8% after a 2.4% March gain as unit sales of light vehicles fell 1.6% to 16.41M. Sales at gasoline service stations rose 0.2% (10.9% y/y).

| April | Mar | Y/Y | 2003 | 2002 | 2001 | |

|---|---|---|---|---|---|---|

| Retail Sales & Food Services | -0.5% | 2.0% | 8.0% | 5.4% | 2.5% | 3.1% |

| Excluding Autos | -0.1% | 1.8% | 9.4% | 5.2% | 3.2% | 3.1% |

by Tom Moeller May 13, 2004

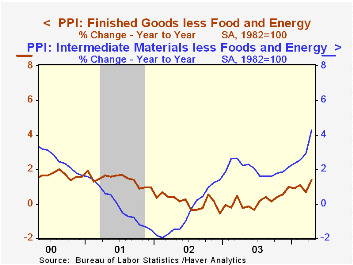

Finished producer prices surged 0.7% last month, the largest monthly gain since March 2003. The surge was more than double Consensus expectations.In contrast, the core PPI rose a moderate, expected 0.2%.

Finished consumer goods prices jumped 0.9% after a 0.7% leap in March. Less food & energy these consumer goods prices rose 0.3% (1.5% y/y) for the second month. Consumer durable prices fell 0.3% (+1.4% y/y) but core non-durable prices jumped 0.7% (+1.6% y/y).

Finished capital goods prices were unchanged for the second month in four (1.3% y/y).

Intermediate goods prices doubled the March gain with a 1.4% increase in April. The increase in core intermediate prices also nearly doubled with a 1.1% jump (4.3% y/y). Plywood prices added another 1.8% (NSA) to the pronounced strength in earlier months (52.3% y/y).

Crude goods prices jumped 3.0% as crude energy prices rebounded 6.3% (12.6% y/y) after the 6.1% March drop. Natural gas prices (5.4% y/y) and crude petroleum prices (29.7% y/y) jumped.

| Producer Price Index | April | Mar | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Finished Goods | 0.7% | 0.5% | 3.6% | 3.2% | -1.3% | 2.0% |

| Core | 0.2% | 0.2% | 1.4% | 0.2% | 0.1% | 1.4% |

| Intermediate Goods | 1.4% | 0.7% | 5.2% | 4.7% | -1.5% | 0.4% |

| Core | 1.1% | 0.6% | 4.3% | 2.0% | -0.5% | -0.1% |

| Crude Goods | 3.0% | 0.7% | 20.4% | 25.1% | -10.6% | 0.3% |

| Core | -3.9% | 2.7% | 26.3% | 12.4% | 3.8% | -10.0% |

by Tom Moeller May 13, 2004

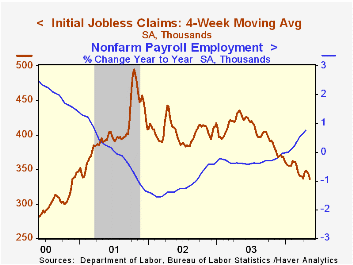

Initial claims for jobless insurance rose 13,000 last week to 331,000 following a 20,000 drop the week prior that was slightly less than initially estimated. Consensus expectations had been for 320,000 claims.

The 4-week moving average of initial claims fell to 335,750 (-22.1% y/y), the lowest level since November 2000.

Continuing claims for unemployment insurance recouped 53,000 of the deepened 83,000 drop the week prior.

The insured rate of unemployment ticked back up to 2.4% from 2.3%.

| Unemployment Insurance (000s) | 5/08/04 | 5/01/04 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Initial Claims | 331 | 318 | -20.8% | 403 | 404 | 406 |

| Continuing Claims | -- | 2,974 | -19.5% | 3,533 | 3,573 | 3,023 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief