Global| Apr 15 2008

Global| Apr 15 2008U.S. PPI Soared

by:Tom Moeller

|in:Economy in Brief

Summary

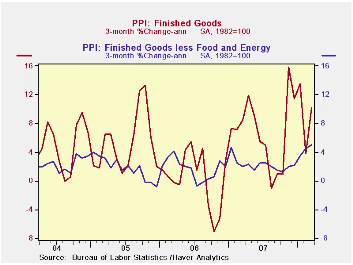

Finished producer prices in the U.S. soared 1.1% last month, up sharply from the unrevised 0.3% February increase. The increase nearly doubled Consensus expectations for a 0.6% rise and it was the strongest rise since last November. [...]

Finished producer prices in the U.S. soared 1.1% last month, up sharply from the unrevised 0.3% February increase. The increase nearly doubled Consensus expectations for a 0.6% rise and it was the strongest rise since last November.

Energy prices surged 2.9% (20.4% y/y) as home heating oil prices spiked by 13.1% (52.0% y/y) and natural gas prices increased 4.2% (4.0% y/y). Gasoline prices continued firm and rose 1.3% (36.4%).

Why Do Gasoline Prices React to Things That Have Not Happened? from the Federal Reserve Bank of St. Louis is available here.

Finished consumer food prices spiked 1.2% (5.8% y/y). During the past three months food prices have risen at a 10.1% annual rate led by soaring egg prices (56.3% y/y), higher dairy prices (13.5% y/y), higher coffee prices (13.8% y/y) and higher bakery product prices (7.8% y/y). That strength has been offset somewhat by easier gains in prices for beef & veal (-0.3% y/y) and fresh fruits (0.0% y/y).

Less food and energy, prices matched expectations and rose a more moderate 0.2%, less than half the 0.5% February surge. Prices of core finished consumer goods rose 0.3% (3.3% y/y) due to strength in nondurable prices (4.4% y/y). Capital equipment prices rose a modest 0.1% (2.0% y/y), about equal to the rise for all of last year.

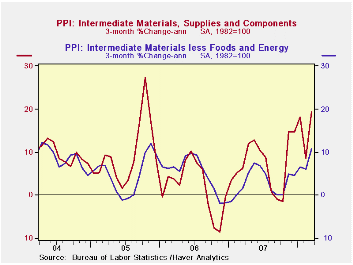

Intermediate goods prices surged 2.3% on the strength of a 2.9% (20.0% y/y) jump in food prices and a 5.9% (26.8% y/y) increase in energy prices. Excluding food & energy, prices about doubled the February rise with a 1.1% increase.

Financial Market Turmoil and the Federal Reserve: The Plot Thickens is yesterday's speech by Federal Reserve Board Governor Kevin Warsh ad it can be found here.

| Producer Price Index (%) | March | February | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Finished Goods | 1.1 | 0.3 | 6.9 | 3.9 | 3.0 | 4.9 |

| Core | 0.2 | 0.5 | 2.8 | 1.9 | 1.5 | 2.4 |

| Intermediate Goods | 2.3 | 0.8 | 10.6 | 4.1 | 6.4 | 8.0 |

| Core | 1.1 | 0.6 | 5.5 | 2.8 | 6.0 | 5.5 |

| Crude Goods | 8.0 | 3.7 | 31.3 | 12.1 | 1.4 | 14.6 |

| Core | 3.5 | 3.3 | 16.7 | 15.7 | 20.8 | 4.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief