Global| Jan 06 2003

Global| Jan 06 2003U.S. Light Vehicle Sales Surge

by:Tom Moeller

|in:Economy in Brief

Summary

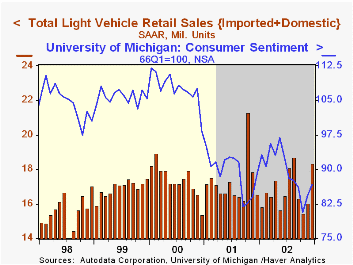

Unit sales of light vehicles surged in December to the highest level since August as zero percent financing incentives again took hold. Sales fell for the second consecutive calendar year since the high of 2000. December sales were [...]

Unit sales of light vehicles surged in December to the highest level since August as zero percent financing incentives again took hold. Sales fell for the second consecutive calendar year since the high of 2000. December sales were much better than Consensus expectations for a 16.1M unit sales rate.

Sales of domestically built vehicles rose 17.7% m/m. Nevertheless, sales were well off the monthly high sales rate of 17.7M units in October 2001. Auto sales rose 10.0% m/m but sales of light trucks surged 23.8%.

Imported vehicle sales rose 0.9% m/m following the strong 14.7% gain in November. Imported auto sales fell 1.4% but truck sales rose 5.8%.

Imports' share of the US light vehicle market fell to 18.4% in December. For the year, imports' share of the US vehicle market averaged 19.5% versus 17.8% during 2001.

| Light Vehicle Sales (SAAR, Mil.Units) | Dec | Nov | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Total | 18.32 | 16.04 | 10.7% | 16.78 | 17.26 | 17.40 |

| Domestic | 14.94 | 12.69 | 12.3% | 13.51 | 14.19 | 14.58 |

| Imported | 3.38 | 3.35 | 4.2% | 3.27 | 3.07 | 2.82 |

by Tom Moeller January 6, 2003

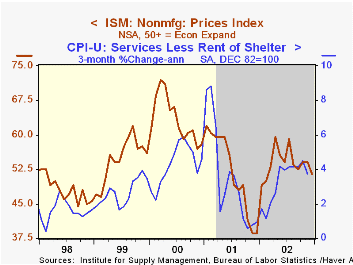

The Institute for Supply Management business activity index of the nonmanufacturing sector fell last month but remained at the second highest level since June. Consensus expectations were for a decline to 55.5.

Of the seasonally adjusted subgroups, the employment index rose modestly to its highest level since August. The new orders index fell slightly to a still high 56.3 and imports fell.

Business activity for the nonmanufacturing sector is a question separate from the subgroups mentioned above. In contrast, the NAPM manufacturing sector composite index weights the components.

The not seasonally adjusted index of prices fell sharply to the lowest level since February.

During the last five years, there has been a 57% correlation between the level of the price index in the NAPM nonmanufacturing survey and the three month growth in the CPI for services less rent of shelter.

ISM surveys more than 370 purchasing managers in more than 62 industries including construction, law firms, hospitals, government and retailers. The nonmanufacturing survey dates only to July 1997, therefore its seasonal adjustment should be viewed tentatively.

| ISM Nonmanufacturing Survey | Dec | Nov | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Business Activity Index | 54.7 | 57.4 | 50.1 | 55.1 | 49.0 | 59.2 |

by Tom Moeller January 6, 2003

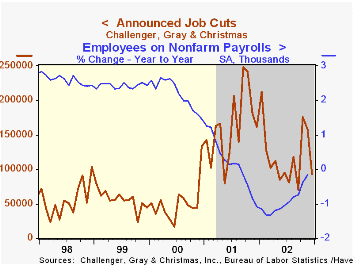

According to Challenger, Gray & Christmas, announced job cuts plunged last month from the elevated levels of October and November.

Because of the earlier surge in layoffs, the three month moving average of job cut announcements rose again to 142,145, the highest level since March. Nevertheless, layoffs were still well below the highs of late 2001.

Announcements of job cuts varied greatly amongst industries with large decline in the electronics, entertainment and financial industries offset by huge increases in health care, pharmaceutical and retail.

| Challenger, Gray & Christmas | Dec | Nov | Y/Y | 2002 | 2001 |

|---|---|---|---|---|---|

| Announced Job Cuts | 92,917 | 157,508 | -42.5% | 1,431,052 | 1,956,876 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief