Global| Feb 21 2008

Global| Feb 21 2008U.S. Leading Economic Indicators Down

by:Tom Moeller

|in:Economy in Brief

Summary

For January, the Conference Board reported that the composite index of leading economic indicators fell 0.1% after a revised 0.1% decline during December. The latest drop matched Consensus expectations. It was the fifth decline in the [...]

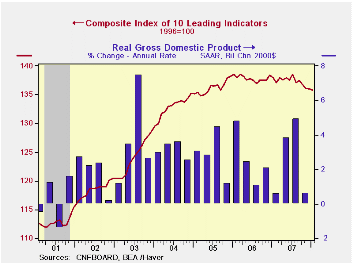

For January, the Conference Board reported that the composite index of leading economic indicators fell 0.1% after a revised 0.1% decline during December. The latest drop matched Consensus expectations. It was the fifth decline in the last six months and since the series' peak last July it has fallen 2.0%.

For all of last year the leaders fell 0.4% and the six month growth rate, calculated as the latest month's reading divided by the average of the prior twelve months, was -4.0%, the lowest since early 2001.

During the last ten years there has been a 59% correlation between the y/y change in the leading indicators index and the lagged change in real GDP.

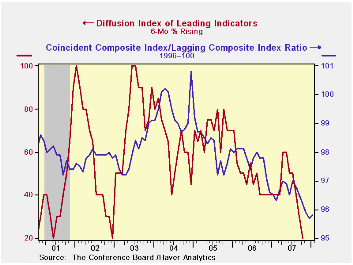

The breadth of one month gain amongst the 10 components of the leading index rose slightly to a break even 50.0%. Over a six month period, the breadth of gain amongst the leaders components cratered to 20%, equal to its lowest level since 2002.

Last month lower stock prices made the largest contribution to the decline in the overall leading index.

The method of calculating the contribution to the leading index from the spread between 10 year Treasury securities and the Fed funds rate has been revised. A negative contribution will now occur only when the spread inverts rather than when declining as in the past. More details can be found here.

The leading index is based on eight previously reported economic data series. Two series, orders for consumer goods and orders for capital goods, are estimated.

The coincident indicators rose 0.1% after a 0.1% December uptick. Over the last ten years there has been an 86% correlation between the y/y change in the coincident indicators and real GDP growth. Three of the four coincident series components rose very slightly and employment fell.

The lagging index was unchanged and the ratio of coincident to lagging indicators (a measure of economic excess) ticked up slightly but remained near its lowest since 1991.Visit the Conference Board's site for coverage of leading indicator series from around the world.

| Business Cycle Indicators | January | December | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Leading | -0.1% | -0.1% | -1.5% | -0.4% | 1.2% | 2.5% |

| Coincident | 0.1% | 0.1% | 1.5% | 1.8% | 2.5% | 2.1% |

| Lagging | 0.0% | 0.2% | 2.3% | 3.1% | 3.0% | 3.5% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief