Global| Apr 16 2008

Global| Apr 16 2008U.S. Industrial Output Up 0.3% Last Month

by:Tom Moeller

|in:Economy in Brief

Summary

Industrial production last month rose 0.3% after a 0.7% February decline which was deeper than reported initially. Also revised down was production growth last year and during 2006. A 0.1% decline in March output had been the [...]

Industrial production last month rose 0.3% after a 0.7% February decline which was deeper than reported initially. Also revised down was production growth last year and during 2006. A 0.1% decline in March output had been the Consensus expectation.

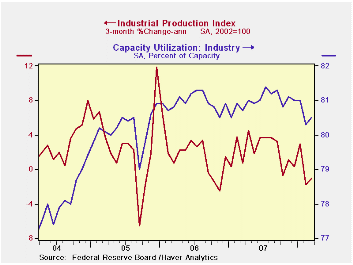

Factory output ticked up 0.1% in March after falling by a downwardly revised 0.5% in February. The three month change in output, however, fell to a negative 1.4% (AR). Production in the high tech sector has been strong and rose 1.3% (13.1% y/y), as it did in February. Outside the high tech sector, factory output fell 0.1% and a February decline was revised deeper to -0.7%. Three month output growth in manufacturing output less high tech fell to -2.8% (AR) but appliance production rose 5.0% last month.

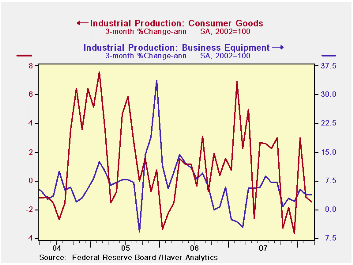

Production of computers & electronics surged again last month by 2.6% and three month growth totaled 20.3% (AR).

Weakness elsewhere in the durable goods area continued intense. Output of furniture & appliances is down at a 10.5% rate during the last three months while production of automotive products has fallen at a 29.0% rate. Auto output is down partially due to the workers' strike at the American Axel Company. Machinery production is off at a 1.2% rate and metals output turned negative. In the nondurables sector apparel product output has fallen at a 10.8% rate over the last three months.

Output of business equipment increased 0.6% after no change in February. Output of industrial equipment less high tech recovered 0.7% after a 0.2% February slip. The three month growth rate improved to 3.9%.

Capacity utilization rose slightly to 80.5% during March but utilization in the factory sector slipped to 78.5%, its lowest also since late 2005. Annual growth in capacity is growing 1.8% y/y and at 2.1% in the factory sector. Less high tech, capacity growth is a lower 0.9% y/y.

| INDUSTRIAL PRODUCTION (SA) | March | February | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total | 0.3 | -0.7 | 1.5 | 1.7 | 2.2 | 3.3 |

| Manufacturing | 0.1 | -0.5 | 1.2 | 1.7 | 2.4 | 4.0 |

| Utilities | 1.9 | -3.6 | 2.3 | 3.3 | -0.6 | 2.1 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief