Global| Feb 18 2009

Global| Feb 18 2009U.S. Import Price Decline Quickened

by:Tom Moeller

|in:Economy in Brief

Summary

The worldwide recession continued to dampen pricing power last month. Overall U.S. import prices fell another 1.1% during January after a 5.0% December decline that was deeper than reported initially. The latest drop about matched [...]

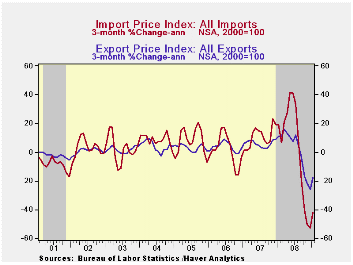

The worldwide recession continued to dampen pricing power last month. Overall U.S. import prices fell another 1.1% during January after a 5.0% December decline that was deeper than reported initially. The latest drop about matched Consensus expectations.

During the last twelve months, the 12.5% decline in import prices is the quickest in the series' history which dates back to 1983.

Petroleum prices fell 2.4% last month. That was a much slower rate of decline than during earlier months, but here in February the decline has quickened again. Crude oil prices are more than ten percent below the January average cost of $41.74 per barrel of crude. That is just back in the range of ten-to-thirty percent monthly declines in place since August.

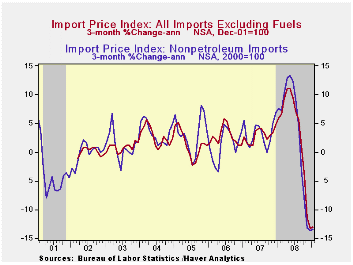

January import prices less petroleum were down for the sixth straight month, by 0.8%. At an annual rate, the 13.4% decline over the last three months is near the record.Through early February, the foreign exchange value of the dollar rose 12.6% versus the year-ago level and thus reduced the pressure on U.S. import prices. During the last ten years, there has been an 83% (negative) correlation between the nominal trade-weighted exchange value of the US dollar vs. major currencies and the y/y change in non oil import prices.

Capital goods import prices were unchanged last month following two consecutive months of decline. That's a reversal from earlier this year. On a three-month basis, prices fell at a 2.5% annual rate after 5%-to-6% rates of increase during early 2008. Less the lower prices of computers, capital goods prices in January rose 0.5%. The three-month growth rate fell to 0.4 after 9.0% growth earlier this year. Prices of computers, peripherals & accessories were down at an 8.7% rate during the last three months.

Prices for nonauto consumer goods were unchanged in January for the second consecutive month. The three-month rate of change remained a negative 1.9% versus the 5.9% peak rate of growth in early-2008. Durable goods prices overall fell at a 5.4% annual rate during the last three months, a reversal from the 6.2% rate of increase in early 2008. To the upside, apparel prices rose 0.3% during January and a 2.0% rate of growth during the last three months is stable with the 1.9% increase in prices during all of last year. Motor vehicle & parts prices fell at a 1.5% rate during the last three months after a 2.6% increase last year.

In yet another area, prices have weakened. Imported food prices fell at a 9.0% annual rate during the last three months after an 11.8% jump during 2008. That increase followed an 8.2% 2007 surge and a 4.0% 2006 increase.

Total export prices increased 0.5% during January after five months of sharp decline. Nonagricultural export prices were unchanged (-2.9% year-to-year) but agricultural prices recovered all of their December drop with a 6.2% (-9.7% y/y) increase.

The import and export price series can be found in Haver's USECON database. Detailed figures are available in the USINT database.

Overview: Global Financial Crisis Spurs Unprecedented Action from the BIS Quarterly Review is available here.

| Import/Export Prices (NSA, %) | January | December | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Import - All Commodities | -1.1 | -5.0 | -12.5 | 11.5 | 4.2 | 4.9 |

| Petroleum | -2.4 | -27.2 | -55.0 | 37.7 | 11.6 | 20.6 |

| Nonpetroleum | -0.8 | -1.1 | -0.6 | 5.3 | 2.7 | 1.7 |

| Export- All Commodities | 0.5 | -2.2 | -3.6 | 6.0 | 4.9 | 3.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief