Global| May 01 2009

Global| May 01 2009U.S. Factory Inventory Decumulation Continues Strong

by:Tom Moeller

|in:Economy in Brief

Summary

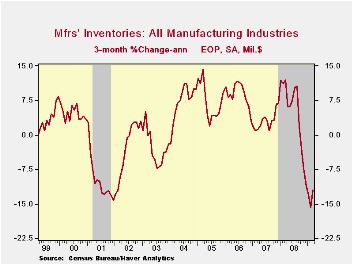

During March, the manufacturing sector continued to shed inventories at near a record rate. The 0.8% decline followed a revised 1.3% cutback during February. During the last three months the 12.1% annualized rate of stock-pile [...]

During March, the manufacturing sector continued to shed inventories at near a record rate. The 0.8% decline followed a revised 1.3% cutback during February. During the last three months the 12.1% annualized rate of stock-pile decumulation was near the record. The series dates back to 1958. That accelerated rate is in spite of a 1.0% rate of accumulation in petroleum inventories, now that prices have firmed. Excluding oil factory inventories fell at a 12.6% three-month rate that was only slightly exceeded in 2001.

The three-month rates of inventory destocking in several industries have been more than notable. Inventories of electrical equipment & appliances have fallen at a 24.1% rate while textile product inventories were down at a 34.8% clip. Steep production cutbacks pulled furniture inventories down at a 21.8% rate since December while inventories of primary metals fell at a 32.5% pace. Lesser rates of decline were registered in the machinery industry (-12.3%) and by computers & electronic products (-11.9%).

The Manufacturers' Shipments, Inventories and Orders (MSIO) data is available in Haver's USECON database.

Inventory accelerator in general equilibrium from the Federal Reserve Bank of St. Louis is available here.

| Factory Survey (NAICS, %) | March | February | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Inventories | -0.8 | -1.3 | -3.8 | 2.1 | 3.7 | 8.2 |

| Excluding Transportation | -0.8 | -1.5 | -6.4 | -0.6 | 2.7 | 7.9 |

| New Orders | -0.9 | 0.7 | -21.6 | 0.1 | 1.9 | 6.2 |

| Excluding Transportation | -0.9 | 0.5 | -19.0 | 3.1 | 1.2 | 7.4 |

| Shipments | -1.2 | -0.5 | -17.1 | 1.7 | 1.2 | 5.9 |

| Excluding Transportation | -1.5 | -0.6 | -17.3 | 3.7 | 1.5 | 6.7 |

| Unfilled Orders | -1.5 | -1.7 | -4.8 | 3.5 | 17.1 | 15.3 |

| Excluding Transportation | -1.5 | -2.1 | -8.7 | -1.0 | 8.2 | 16.0 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief