Global| Aug 02 2005

Global| Aug 02 2005U.S. Factory Inventories Down Again

by:Tom Moeller

|in:Economy in Brief

Summary

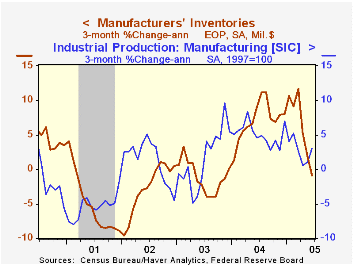

Factory inventories fell in June, down modestly for the third consecutive month. Three month growth in inventories fell to -0.9% (AR) versus the peak rate of accumulation near 12% in March and 7.5% growth last year. The slowdown [...]

Factory inventories fell in June, down modestly for the third consecutive month. Three month growth in inventories fell to -0.9% (AR) versus the peak rate of accumulation near 12% in March and 7.5% growth last year. The slowdown accounts for much of this year's slowdown in factory output growth.

Slower rates of inventory accumulation continue notable in the primary metals industry where three month growth fell to 0.5% versus the high of 42.2% and in the electrical equipment industry where growth in inventories fell to 1.8% versus an 18.5% peak. The level of computer inventories has been declining this year versus a peak growth rate of 13% last summer.

Factory shipments fell slightly in June and three month growth fell to 3.7% versus the high above 20% early last year.

Orders to the factory sector jumped 1.0% and the rise in durable goods orders was revised up to 2.0% from the advance report of a 1.4% gain.

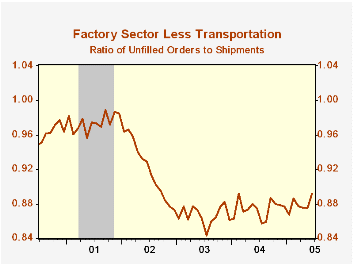

Unfilled orders surged another 2.8% as backlogs of aircraft & parts jumped 5.8% (30.2% y/y). Less transportation altogether backlogs rose 1.9% (9.5% y/y) boosted by a 2.5% (14.8% y/y) gain in machinery. The ratio of unfilled orders to shipments outside of transportation jumped the highest level since 2002.

| Factory Survey (NAICS) | June | May | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Inventories | -0.0% | -0.2% | 6.4% | 7.5% | -1.3% | -1.8% |

| New Orders | 1.0% | 3.6% | 9.8% | 10.9% | 3.7% | -1.9% |

| Shipments | -0.1% | 0.3% | 6.2% | 10.5% | 2.6% | -2.0% |

| Unfilled Orders | 2.8% | 2.1% | 10.1% | 9.1% | 4.2% | -6.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief