Global| Jun 02 2006

Global| Jun 02 2006U.S. Employment & Wage Growth Slowed

by:Tom Moeller

|in:Economy in Brief

Summary

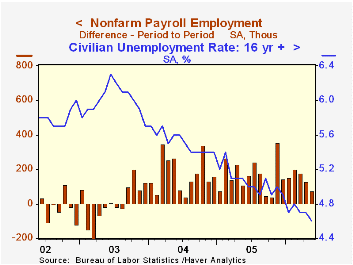

Nonfarm payrolls rose a modest 75,000 during May, the weakest increase since last October. Moreover, job gains during the prior two months were revised down by a cumulative 37,000 while the May gain fell short of Consensus [...]

Nonfarm payrolls rose a modest 75,000 during May, the weakest increase since last October. Moreover, job gains during the prior two months were revised down by a cumulative 37,000 while the May gain fell short of Consensus expectations for a 175,000 rise.

Despite the weak jobs figures from the establishment survey, the household survey indicated a drop in the unemployment rate to 4.6% which compared to Consensus expectations for m/m stability at 4.7%. Employment rose 288,000 (1.7% y/y) and the labor force rose 180,000 (1.2% y/y).

Private sector payrolls grew 67,000 (1.6% y/y) during May while government employment rose 8,000 (0.7% y/y).

Private service-producing jobs rose 77,000 (1.6% y/y) last months after a downwardly revised 72,000 rise in April. For the twelve months ending March, these jobs were rising an average 131,000 per month. May jobs in retail trade fell 27,100 (-0.1% y/y) again reflecting broad based sector declines. Financial sector jobs rose 12,000 (2.7% y/y) and professional & business services employment rose 27,000 (2.7% y/y). Temporary help services jobs fell by 2,800 (+3.7% y/y), the fourth m/m decline this year. Jobs in education & health rose a firm 41,000 (2.4% y/y) but leisure & hospitality jobs increased just 4,000 (1.7% y/y).

Factory sector payrolls fell 14,000 after an unrevised 19,000 April increase. Employment in the motor vehicles & parts industries fell 9,700 (-1.7% y/y) and computer & electronics payrolls reversed all of the prior month's gain with a 4,6000 (+0.3% y/y) worker decline.

Construction employment increased just 1,000 (3.5% y/y) following monthly gains that averaged 22,000 during the prior year.

Growth in average hourly earnings moderated to 0.1% from an upwardly revised 0.6% rise during April. The slowdown exceeded Consensus expectations for a 0.3% increase. Private service-producing wages rose just 0.1% (4.2% y/y) following a 0.7% increase in April. Professional & business services wages were unchanged (5.7% y/y) after a 1.1% April jump while finance, insurance & real estate earnings fell 0.1% (4.6% y/y). Factory sector earnings were unchanged (1.6% y/y) after an upwardly revised 0.4% April gain.

| Employment | May | April | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Payroll Employment | 75,000 | 126,000 | 1.4% | 1.5% | 1.1% | -0.3% |

| Manufacturing | -14,000 | 19,000 | -0.1% | -0.6% | -1.3% | -4.9% |

| Average Weekly Hours | 33.8 | 33.9 | 33.7 (May '05) | 33.8 | 33.7 | 33.7 |

| Average Hourly Earnings | 0.1% | 0.6% | 3.7% | 2.8% | 2.1% | 2.7% |

| Unemployment Rate | 4.6% | 4.7% | 5.1% (May '05) | 5.1% | 5.5% | 6.0% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief