Global| Feb 02 2009

Global| Feb 02 2009U.S. December Income, Consumption & Prices Fell While Savings Rose

by:Tom Moeller

|in:Economy in Brief

Summary

The personal income & outlays report for the end of 2008 contained news of difficult times for the "front-end" of the U.S. economy. To start, personal income fell for the third straight month. The 0.2% December decline was a bit less- [...]

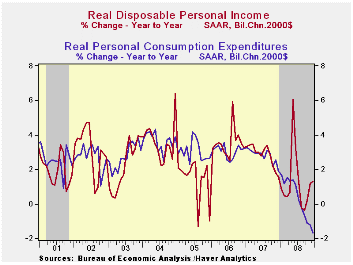

The personal income & outlays report for the end of 2008 contained news of difficult times for the "front-end" of the U.S. economy. To start, personal income fell for the third straight month. The 0.2% December decline was a bit less-than-expected and it lowered the gain for the full year to 3.7% which was the weakest since 2003. The year ended with December-to-December growth in income of just 1.4% and a three-month drop of 2.6% (AR).

A 0.3% decline in wages & salaries was in the forefront of that income weakness as employment levels declined. Wages over the last three months were down at a 2.1%rate and up just 2.8% for the full year, half that during 2007. Factory sector wages suffered the worst of the shortfall with an 8.2% three-month rate of decline. In addition, service sector wages fell at a 1.5% rate during those three months which was their weakest performance since the recession of 2001.

Lower interest rates caused the seventh straight monthly

decline in interest income. The -7.2% y/y growth rate was eclipsed,

however, by the 22.1% rate of decline during the last three months.

Dividend income also fell at a 5.9% rate during that three month period

as corporate profits fell.

Disposable personal income dropped last month for the sixth month in the last seven to lower the three-month change to -2.3%. Thanks to falling energy prices and weaker pricing power generally, real disposable income growth actually increased by a strong 6.7% (1.3% y/y).

Personal consumption suffered heavily from across-the-board

weakness. The December decline was the sixth in a row. While the

three-month rate of growth was an abysmal -11.2% (AR), the change in

real terms was little better. Real personal consumption

expenditures fell 0.5% last month and at a 3.1% during the

last three.

Real spending on discretionary items was notably weak. Motor vehicle & parts purchases fell 0.4% in December and the three-month annual growth rate amounted to -33.1%. Real spending on household furniture & appliances fell at a lesser 4.7% rate while real spending on apparel dropped at a 2.7% rate since September. These and other detailed spending figures are available in Haver's USNA database.

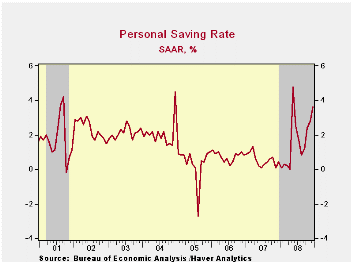

The silver lining of this weakness in spending is while it reflects weakened income growth, it also produced a rise in the level of savings. The personal savings rate rose last month to 3.6 versus an average of 1.7% for the year, which was the highest since 2004.

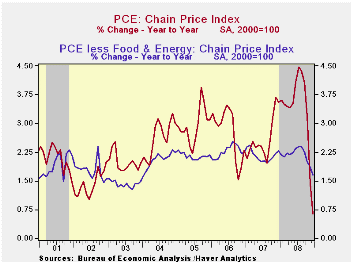

Declines in spending caused pricing power to evaporate. The PCE chain price index fell 0.5% last month with lower petroleum prices. Core pricing power, however, was additionally under pressure. The 0.0% December downtick in the core PCE price index about matched expectations and it was the third such consecutive decline. It lowered the three-month change in core pricing to -0.1% which was its weakest since the recession of 2001.

The Federal Reserve Board published a policy that was adopted to help avoid preventable foreclosures on certain residential mortgage assets. The Fed's release can be found here.

| Disposition of Personal Income (%) | December | November | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Personal Income | -0.2 | -0.4 | 1.4 | 3.7 | 6.1 | 7.1 |

| Disposable Personal Income | -0.2 | -0.3 | 1.9 | 4.6 | 5.5 | 6.4 |

| Personal Consumption | -1.0 | -0.8 | -1.1 | 3.6 | 5.5 | 5.9 |

| Saving Rate | 3.6 | 2.8 | 0.4 (Dec. 08) | 1.7 | 0.5 | 0.7 |

| PCE Chain Price Index | -0.5 | -1.1 | 0.6 | 3.3 | 2.6 | 2.8 |

| Less food & energy | -0.0 | -0.0 | 1.7 | 2.2 | 2.2 | 2.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief