Global| Sep 29 2009

Global| Sep 29 2009U.S. Consumer Confidence Moves Sideways After Spring Bounce

by:Tom Moeller

|in:Economy in Brief

Summary

The Conference Board indicated that consumer confidence during September dipped from August. Though both figures were up sharply from the February low, the trend in the series has been roughly sideways since May. The Conference Board [...]

The Conference Board indicated that consumer confidence during September dipped from August. Though both figures were up sharply from the February low, the trend in the series has been roughly sideways since May. The Conference Board data can be found in Haver's CBDB database.

During the last ten years there has been an 86% correlation between the level of consumer confidence and the y/y change in real consumer spending.

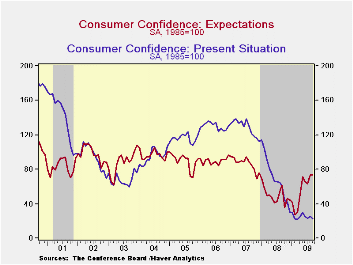

Consumers' assessment of the current economic conditions fell

again this month and remained near the historic low. It remained off by

almost two-thirds from one year earlier. Jobs were seen as hard to get

by an increased 47.0% of respondents and jobs were seen as plentiful by

3.4% which was near the series' historic low. Business conditions were

seen as good by just 8.7% and that also was near the series' low.

Consumers who thought business conditions were bad rose slightly to

46.3%. While off somewhat from its high the reading still near the

highest since 1983.

The expectations component of confidence slipped from August but the index remained near the highest level since late-2007. The percentage of respondents expecting business conditions to improve slipped to 21.3% though that remained near the highest level since 2004. A much reduced 15.0% expected conditions to worsen. That was off from the recent February high of 40.7%. An improved 17.9% of respondents expected economic improvement to generate more jobs, more than double the percentage at the recent low.

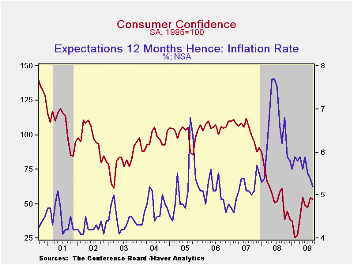

Expectations for the inflation rate in twelve months fell back to 5.2%, the lowest level since 2007 and down from last year's high of 7.7%. Interest rates in twelve months were expected to be higher by 48.8% of respondents, while 14.8% expected rates to fall. A greatly increased 35.4% of respondents expected stock prices to rise.

Consumers continued to manage their spending plans cautiously. Just 2.3% plan to buy a home during the next six months while 23.8% plan to buy a major appliance. That's versus 30.9% back in 2007. Only 4.4% plan to buy an automobile versus 6.0% in 2007. Just 2.1% plan to buy a new one.

Is The Financial Crisis Over? A Yield Spread Perspective from the Federal Reserve Bank of St. Louis is available here.

| Conference Board (SA, 1985=100) | September | August | Y/Y % | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Consumer Confidence Index | 53.1 | 54.5 | -13.5 | 57.9 | 103.4 | 105.9 |

| Present Situation | 22.7 | 25.4 | -62.8 | 69.9 | 128.8 | 130.2 |

| Expectations | 73.3 | 73.8 | 19.2 | 50.0 | 86.4 | 89.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief