Global| May 13 2008

Global| May 13 2008U.S. Business Inventory Gain Slowed, Retail Inventories Fell

by:Tom Moeller

|in:Economy in Brief

Summary

Total business inventories grew just 0.1% during March. The gain was less than the expected 0.4% rise and the 0.5% February increase was little revised. The annualized three month growth in inventories backed off slightly to 6.6% from [...]

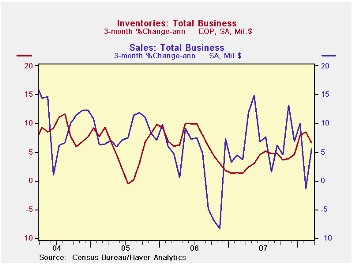

Total business inventories grew just 0.1% during March. The gain was less than the expected 0.4% rise and the 0.5% February increase was little revised. The annualized three month growth in inventories backed off slightly to 6.6% from the elevated 8.5% growth rate in February.

Retail inventories fell 0.5% as the three month growth rate went negative at -0.9%. Inventories of motor vehicle & parts fell at a 0.9% rate during the last three months due to production cutbacks. Outside of autos, however, retail inventories plunged 0.4% in March and at a 1.0% rate during the last three months, the first decline since 2003.

The industry detail in the retail sector indicated that furniture inventories fell at an annual rate of 7.0% during the last three months. Clothing & accessory store inventories also dropped hard at a 7.9% rate during that period. General merchandise stores' inventories finally fell at a 2.9% rate due to the 1.1% cutback in March.

Factory inventories increased 0.9% following the upwardly revised 0.7% February increase. Higher oil prices continued to drive the increase and they rose 5.3%, 89.9% at an annual rate over the last three months. But elsewhere accumulation also has been strong. Excluding petroleum, factory inventories rose at a 7.9% rate over the last three months versus 5.9% growth during 4Q and 1.7% in 3Q.

Wholesale inventories fell 0.1% after the 0.9% February surge. Less the strong gains in petroleum inventories, accumulation still has been very firm at a 9.9% rate over the last three months after 4.9% growth last year.

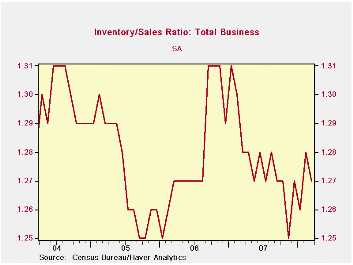

Total business sales rose 1.0% and made all of the prior month's decline. Three month growth recovered to 5.5% after having gone negative in February. The I/S ratio fell slightly to 1.27 in March. That's the average for the year to date and it is equal to all of 2007.

| Business Inventories | March | February | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total | 0.1% | 0.5% | 5.2% | 3.8% | 5.9% | 6.0% |

| Retail | -0.5% | -0.1% | 2.4% | 2.6% | 3.5% | 2.3% |

| Retail excl. Auto | -0.4% | -0.2% | 1.8% | 2.7% | 4.9% | 3.9% |

| Wholesale | -0.1% | 0.9% | 6.8% | 5.5% | 8.3% | 7.3% |

| Manufacturing | 0.9% | 0.7% | 6.5% | 3.7% | 6.4% | 8.9% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief