Global| May 01 2019

Global| May 01 2019U.K. Manufacturing Sector Slows

Summary

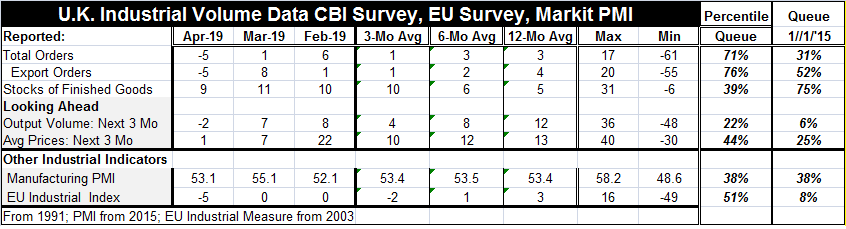

The U.K. manufacturing PMI from Markit falls to 53.1 in April from 55.1 in March. Interestingly, the averages of the various industrial gauges in the table show degradation from their respective 12-month averages to their six-month [...]

The U.K. manufacturing PMI from Markit falls to 53.1 in April from 55.1 in March. Interestingly, the averages of the various industrial gauges in the table show degradation from their respective 12-month averages to their six-month averages to their three-month averages. There are two exceptions. One exception is for inventories that sequentially crept higher, a movement that actually reinforces notions of an economic slowing. The other exception is for the U.K. manufacturing PMI which is surprisingly steady when averaged over each horizon.

The U.K. manufacturing PMI from Markit falls to 53.1 in April from 55.1 in March. Interestingly, the averages of the various industrial gauges in the table show degradation from their respective 12-month averages to their six-month averages to their three-month averages. There are two exceptions. One exception is for inventories that sequentially crept higher, a movement that actually reinforces notions of an economic slowing. The other exception is for the U.K. manufacturing PMI which is surprisingly steady when averaged over each horizon.

On the far right, I present two columns of percentile standings the first for a long period and for the longest period that would allow comparison among all measures. In the percentile queue column (long span where applicable), the standing of orders, export orders, expected output volume for the next three months, average prices expected for the next three months and the EU industrial index all show higher standings for the April values than what appear when ranked on a shorter more recent span of time.

These ranking differences communicate that the data from the recent shorter period are stronger in general than in the longer period causing the current rankings of April date to appear weaker than they are relative to their broader historic levels when we compared them to the shorter data period.

Since the PMIs are only available in a generalized data base for this short period, the ranking of this index grades out as weaker than it ought to be. The EU industrial survey is available for a longer period back to 2003 and it is similar in concept to the Markit survey. Its own ranking falls to its lower 8% over the recent short period compare to a 38th percentile standing over its broader, longer period. Both are poor and low.

Even so, the longer period queue percentile standings range from moderate to weak. There is no case for a strong U.K. factory sector here. But there is some uncertainty about how weak the manufacturing sector really is.

The May Administration is still in negotiations with Labor to try and get a Brexit agreement that can pass the scrutiny of Parliament. Until the U.K. forms a Parliament friendly plan that the EU will accept, there is a good change that the U.K. business deterioration will continue. The data show that sequential deterioration is in gear from twelve months to six months to three months, but there is also deterioration within the last three months with only the Markit manufacturing PMI gauge on some sort of an improving ‘trend’ compared to February and March. Even there, the gauge is higher compared to March but lower compared to February.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief