Global| May 22 2019

Global| May 22 2019U.K. Inflation Kicks Up

Summary

The Bank of England makes monetary policy off the CPIH, which is the CPI measure inclusive of a measure of housing costs. This measure puts the U.K. on the same footing as the U.S. with its inflation measures and is unlike the EMU [...]

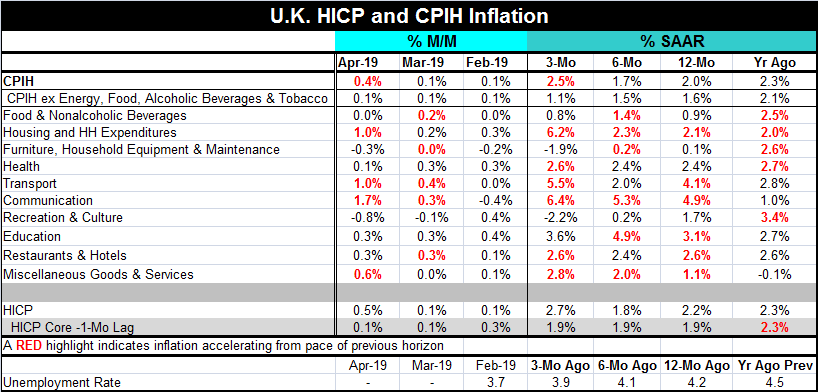

The Bank of England makes monetary policy off the CPIH, which is the CPI measure inclusive of a measure of housing costs. This measure puts the U.K. on the same footing as the U.S. with its inflation measures and is unlike the EMU where the HICP excludes housing costs altogether. The HICP measure for the U.K. is presented in the table below. Housing costs are an important part of consumer expenditure when you are not a native living in an idyllic Pacific Island. But countries have a hard time deciding how to measure them and inject them into the price index. Housing is always an item of dispute in the CPI. The dispute was so great when the EMU was formed that the only consensus they could come by was to leave them out, which is not a great compromise.

The Bank of England makes monetary policy off the CPIH, which is the CPI measure inclusive of a measure of housing costs. This measure puts the U.K. on the same footing as the U.S. with its inflation measures and is unlike the EMU where the HICP excludes housing costs altogether. The HICP measure for the U.K. is presented in the table below. Housing costs are an important part of consumer expenditure when you are not a native living in an idyllic Pacific Island. But countries have a hard time deciding how to measure them and inject them into the price index. Housing is always an item of dispute in the CPI. The dispute was so great when the EMU was formed that the only consensus they could come by was to leave them out, which is not a great compromise.

At this point whether policy is made off the HICP or the CPIH does not seem to have a great important although that could change in the future.

The CPIH is back at its 2% mark in April. It has had a run of three months below the 2% pace in January, February and March. Previously from February 2017 through November 2018, it had a 22-month run above its targeted 2% pace as the ECB had eased policy in the wake of the pro-Brexit vote undercutting the pound sterling leading to a rise of inflation on the back of higher import prices.

In April 2019, inflation is at the doorstep of excess again.

Core inflation is still well behaved. The lagged core HICP pace is stuck at a 1.9% pace over three months, six months and 12 months. More importantly, the CPIH enhanced core that excludes food, energy, tobacco and alcohol has decelerated. This measure of inflation is up by 1.6% over 12 months and 1.1% over three months, having ramped down to slower speeds. In contrast, housing and housing expenditures have accelerated and currently run at a pace of 6.2% over three months (annualized). Communications prices and miscellaneous goods and services prices also steadily accelerate. Only Recreation and culture prices decelerate among the major categories from 12-months to six-months to three-months (apart from the enhanced core, of course).

Among ten categories, eight of them show inflation at a better than 2% pace (annualized) over three months. Five of 10 categories show annualized inflation over 2% over six months. Over 12 months, six of 10 categories have annualized inflation as excessive. But much of this excess clearly stems from energy prices as the enhanced core’s tranquility underscores.

While the headline may nonetheless cause the BOE to feel some policy constraint against dropping rates, I would judge that if economic conditions got dicey it would be willing to make policy off the better conceived enhanced core signal (which measures inflation as restrained).

And risk abounds, as the U.K. continues to struggle with Brexit, Theresa May’s latest and perhaps last proposal was shot down. This does not seem to leave many options apart from a hard Brexit on the table mainly because if no other plan is adopted hard Brexit is the backup plan. May has promised to resign eventually, but that timing will be up to her since she was last challenged in December 2018 and by parliamentary rules she cannot be challenged again until 12 months pass. So she remains in the driver’s seat but in the seat of a vehicle that cannot be controlled.

All of this puts great risk on the economy. Rising oil prices have been able to ramp up headline inflation, but in my view that does not seriously impede the BOE that in any event has been willing to look at the inflation situation much more broadly than the ECB does. Moreover, if Brexit threatens the economy a lot of forces could be put in play including impulses of weakness from merchants suddenly disadvantaged by a hard Brexit and potentially inflationary forces too, if the pound reacts badly and falls again. Regardless of the actual inflation signals, the BOE could find itself in a position with few good or clear options.

But we are told that the BOE has been thinking about this for a long time and that it has long thought that a hard Brexit was one of the likelier cases and so it has been preparing for it. Preparedness is a good state. But unfortunately, it would likely still be trumped by hard Brexit which would be a very bad state.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief