Global| May 13 2019

Global| May 13 2019OECD Leading Economic Indicators Demonstrate Growing Weakness

Summary

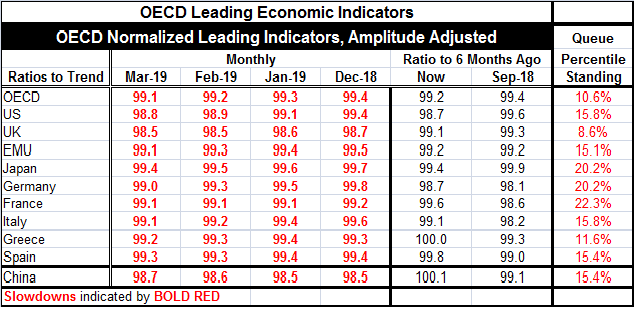

The OECD LEIs are adjusted in such a way that both the change and level give the individual series meaning. Levels below 100 indicate subpar growth and declines also point to weakening conditions. The OECD prefers to look at index [...]

The OECD LEIs are adjusted in such a way that both the change and level give the individual series meaning. Levels below 100 indicate subpar growth and declines also point to weakening conditions. The OECD prefers to look at index changes over six months. The table has two sets of such comparisons gear to look at the indexes on that basis. These looks at the ratio of the indexes to six months ago and at six months ago compared to the six months before that. Both comparisons show a truck-load of weakness.

The OECD LEIs are adjusted in such a way that both the change and level give the individual series meaning. Levels below 100 indicate subpar growth and declines also point to weakening conditions. The OECD prefers to look at index changes over six months. The table has two sets of such comparisons gear to look at the indexes on that basis. These looks at the ratio of the indexes to six months ago and at six months ago compared to the six months before that. Both comparisons show a truck-load of weakness.

In terms of the level, all the LEI indexes are below 100 indicating a slowdown. The ratio to six months ago finds all countries/regions lower than six months ago and lower than the six months before that as well (except for Greece over the recent six months). The table also shows values below 100 for all countries/regions over the last three months. That result extends to the last four months and except for Germany to the past five months. April is the latest month in which more than two of the OECD values in the table were at 100 or more for the same month.

The table also offers a look at the OECD LEIs ranked over all values since December 1994. Over that 24-year period, the strongest of the LEIs right now is in its 20th percentile decile in with none as high as their respective 25th percentile. France, Germany and Japan log the relative strongest LEI readings in March. The U.S. with a rank standing in its 15.8 percentile is one of the weaker country readings in the table, surpassed in significant measure only by the weakness in the U.K. The U.K. is suffering from Brexit fever, a long lasting and seemingly incurable ‘disease.’ Just one percentage point stronger than the OECD standing is Greece.

The OECD LEIs have gotten about as weak as they have been as a MINIMAL condition before several past U.S. recessions

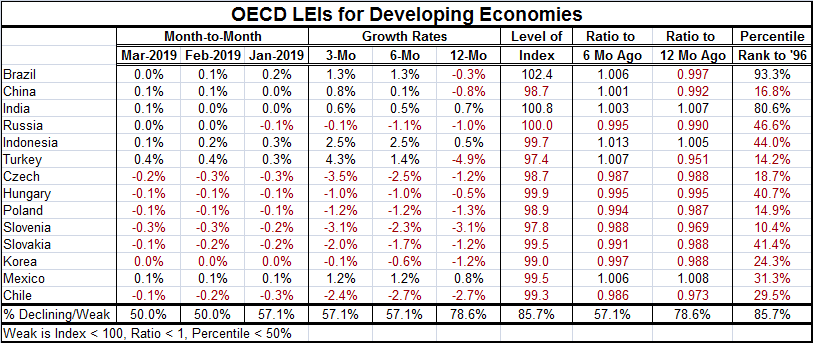

Developing economies reveal a rash of weak readings in terms of momentum as well as in terms of levels. Twelve of fourteen are at or below 100 with only Brazil and India have readings above 100; Russia has a reading right at 100. The ratios to six months ago and for six months ago to six months before that show 57% of the developing economies below a ratio of unity over six months and 78% below a ratio value of unity for the previous six months.

The percentile standings on rankings back to 1996 show strong standings for Brazil (93rd percentile) and India (80th percentile). No other countries have a ranking as high as the 50th percentile. That means all the rest have standings below their respective medians for this period.

The OECD LEIs are falling on a broad trend to weaker growth. With the U.S.-China trade conflict in gear and Brexit dragging on in Europe and both episodes will be further weakening global trends that already are sliding.

The OECD LEIs have slipped ahead of past recessions as much as they have weakened already. However, in recessions they slid quite a bit more after the recession began. China already has expended a lot of energy and run up already substantial debt levels to try to extend growth in the face of trade pressure. Yet, growth in China is about to come under even greater pressure. The U.S. has already used fiscal policy in this cycle. Central banks are for the most part already full stop on stimulus, the Fed being the main exception. While in the U.S. Federal Reserve is running a wait-and-see policy, it seems as though the bigger more dangerous and global risk is on the downside - not from inflation on the upside. We’ll see if policymakers figure this out in time or not.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief