Global| Aug 11 2004

Global| Aug 11 2004OECD Leaders Again Flat

by:Tom Moeller

|in:Economy in Brief

Summary

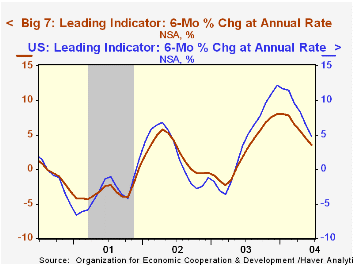

Since February, the Index of Leading Indicators for the Major Seven OECD Countries is virtually unchanged. Flat readings in both June and May pulled the six-month rate of growth to 3.6%, less than half the growth rate when the year [...]

Since February, the Index of Leading Indicators for the Major Seven OECD Countries is virtually unchanged. Flat readings in both June and May pulled the six-month rate of growth to 3.6%, less than half the growth rate when the year began.

Leaders in Japan and in the United States have weakened notably. Since February the leaders in Japan fell 0.7% and in the US they are down 0.1%. Declines in construction and share prices accounts for much of the weakness in both countries.

The leading index for the European Union has remained relatively firm, up 0.9% since February due to 1.6% growth in the German leaders and 1.5% growth in the French leaders. Leaders in Italy, however, fell 0.8% during the last four months and the leaders in the UK fell in three of the last four months. The six month growth rate dropped to fell to 1.3% from the high of 5.1% in February.

In Canada the leading index continued higher through June. A 0.8% gain pulled the six-month growth rate rose to 6.6versus a low of -3.1% in early 2003.

Visit the OECD's website at this website.

| OECD Main Economic Indicators | June | May | 6-Mth Chg. | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| OECD Major Seven - Leading Index (Trend Restored) |

102.6 | 102.6 | 3.6% | 2.6% | 2.3% | -3.1% |

| European Union | 106.0 | 105.9 | 4.1% | 2.3% | 3.5% | -2.4% |

| Japan | 97.5 | 97.3 | 0.4% | 1.8% | 0.3% | -4.5% |

| United States | 103.1 | 103.2 | 4.8% | 3.9% | 2.1% | -3.3% |

by Tom Moeller August 11, 2004

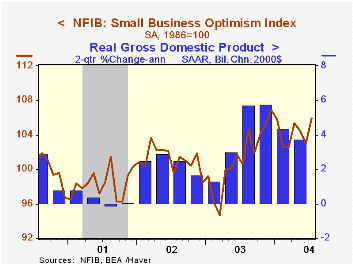

The Small Business Optimism Index published by the National Federation of Independent Business (NFIB) jumped 2.8% last month and the increase recovered all of the decline during the prior two months.

The percentage of firms expecting the economy to improve jumped to 37%, the highest level since January. The percent of firms planning to raise employment rose to 15%, also the highest percentage since January.

The percentage of firms raising average selling prices fell sharply to 20% from the record 29% in June.

During the last ten years there has been a 68% correlation between the level of the NFIB index and the two quarter % change in real GDP.

About 24 million businesses exist in the United States. Small business creates 80% of all new jobs in America.

| Nat'l Federation of Independent Business | July | June | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Small Business Optimism Index (1986=100) | 105.9 | 103.0 | 5.3% | 101.3 | 101.2 | 98.4 |

by Tom Moeller August 11, 2004

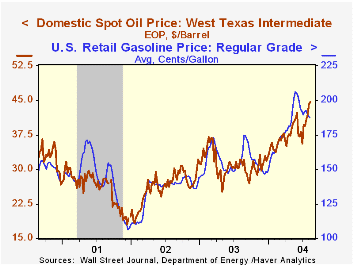

Spot crude oil prices surged last week with the price of West Texas Intermediate crude rising to a record $44.55 per barrel. The average price for unleaded regular gasoline fell to $1.88 per gallon versus the high of $2.06 in late May.

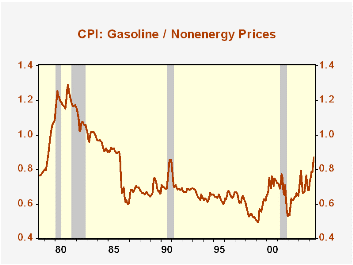

Despite the decline in gas prices the relative price of gasoline is the highest since the early 1980s, up 85% since the low in early 1999.

Wholesale natural gas prices eased further last week to $5.78/mmbtu (+21.2% y/y).

For the latest Short Term Energy Outlook from the US Department of Energy click here.

| Energy Prices | 08/09/04 | 12/31/03 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| US Retail Gasoline, Regular ($/Gal.) | $1.88 | $1.48 | 19.5% | $1.56 | $1.35 | $1.42 |

| Domestic Spot Market Price: West Texas Intermediate ($/Barrel) | $44.55 | $32.78 | 39.5% | $32.78 | $31.23 | $19.38 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief