Global| Sep 28 2007

Global| Sep 28 2007Money Markets: Has the Crisis Passed?

Summary

Forces on money markets that were quite severe just a few weeks ago look to be letting up. There are still reasons for concern, but the most current information about the markets' behavior seems to portray some remission of August's [...]

Forces on money markets that were quite severe just a few weeks ago look to be letting up. There are still reasons for concern, but the most current information about the markets' behavior seems to portray some remission of August's liquidity squeeze.

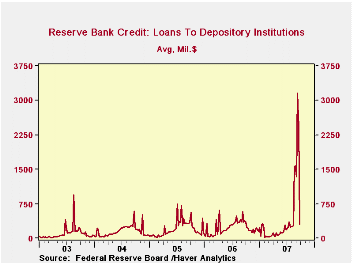

The simplest indicator is the amount of bank borrowing at the Federal Reserve. The data out late yesterday for the Fed's statement week ended Wednesday showed just $306 million in loans to depository institutions on average during the week, down from $2.421 billion the week before. Primary credit, the kind of borrowing meant for operational needs, averaged only $88 million, compared with the previous $2.179 billion, and it fell to 0 on Wednesday. Another favorable sign is the continuing absence of secondary credit, that granted on a penalty-rate basis to banks facing more intense difficulties. A deteriorating situation might suggest greater use of this facility, but only one week, August 22, has seen any of this type of borrowing.

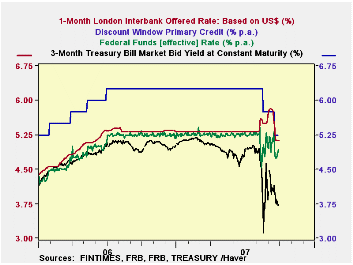

Interest-rate relationships have stopped worsening. In the second graph, we plot four major short-term interest rates. The "riskiest" is 1-month LIBOR; from near stability for well over a year, it lurched suddenly higher in mid-August while US Treasury bill rates were dropping. It continued higher through the early part of this month, peaking at 5.82% on September 7. Borrowers who pay LIBOR rates have far from risky credit, but they are private businesses, not governments; in this environment, that was enough. They paid a double premium: the absolute level of their rates went up, and relative to Treasuries, its spread widened dramatically. This situation has improved, most especially since the September 18 FOMC meeting. This LIBOR rate has fallen to 5.12%, although it's still considerably wider to Treasury bills than has been usual.

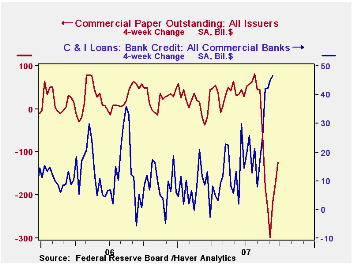

Among types of credit, the commercial paper market continues to shrink. This very short-term borrowing (most is 1-4 days now) has decreased in total by $369 billion since the end of July, equal to 16.6%. The weekly declines have become progressively smaller, and the most traditional type of "paper", that issued by nonfinancial companies, has been basically flat throughout September. Asset-backed paper, the newest kind and carrying the greatest perceived risk, is still retreating; it is down altogether now by $271 billion since August 15, a 23% drop. Notably, as we pointed out here a month ago, banks have been taking up some of this financing slack. Total bank loans had grown at a 21% annual rate in the four weeks through September 12; the key "commercial and industrial" category was up at a whopping 58% pace, equal to $46 billion. This compares to $25.3 billion in the four weeks before that. It doesn't offset all of the contraction in commercial paper -- and bank lending does not cover the exact same uses in the first place. But the upturn in bank activity came quickly, suggesting an adaptability of both lenders and borrowers toward meeting financial needs, even in the face of near-crisis conditions.

| Million $ | 9/26/07 | 9/19/07 | 9/12/07 | August 2007 | Jan-July 2007 | 2006 |

|---|---|---|---|---|---|---|

| Loans to Deposit Institutions | 306 | 2421 | 3158 | 778 | 133 | 225 |

| Primary | 88 | 2179 | 2932 | 506 | 55 | 59 |

| Secondary | 0 | 0 | 0 | 17 | 1 | 0 |

| Seasonal | 218 | 241 | 226 | 255 | 77 | 166 |

| Percent | ||||||

| Fed Funds Rate | 4.79 | 5.12 | 4.98 | 5.02 | 5.25 | 4.96 |

| Discount Rate | 5.25 | 5.61 | 5.75 | 6.01 | 6.25 | 5.96 |

| Seas. Adj. Bil. $ | ||||||

| Commercial Paper--Total | 1,855.4 | 1,869.1 | 1,917.1 | 2,191.5 | 2,064.8 | 1,798.0 |

| Asset-Backed | 912.2 | 929.5 | 945.1 | 1,110.7 | 1,100.3 | 931.4 |

| Weekly Change | -17.3 | -15.6 | -21.6 | -57.0 | +4.5 | +4.0 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief