Asia| May 18 2026

Asia| May 18 2026Economic Letter from Asia: After the Summit

In this week’s Letter, we review the key outcomes from last week’s US–China summit, which, while largely symbolic as a reset in bilateral relations, also yielded several notable trade-related agreements (chart 1). We also examine China’s latest monthly data releases, which extended last month’s moderation in growth and further highlighted the increasingly two-speed nature of its economy (chart 2). Turning to Japan, we look ahead to this week’s key data releases. Q1 GDP growth appears likely to be supported by resilient exports, while the domestic picture—reflected in indicators such as household spending—continues to lag (chart 3). On the inflation front, upcoming CPI readings will be closely watched; if price pressures accelerate further alongside continued yen weakness, this could revive a policy dilemma for the Bank of Japan (chart 4). Zooming out, inflation appears to have reasserted itself as the dominant market driver, with nominal yields rising across markets (chart 5). At the same time, AI-related optimism has taken a back seat for now, as equity markets pull back from recent rallies (chart 6).

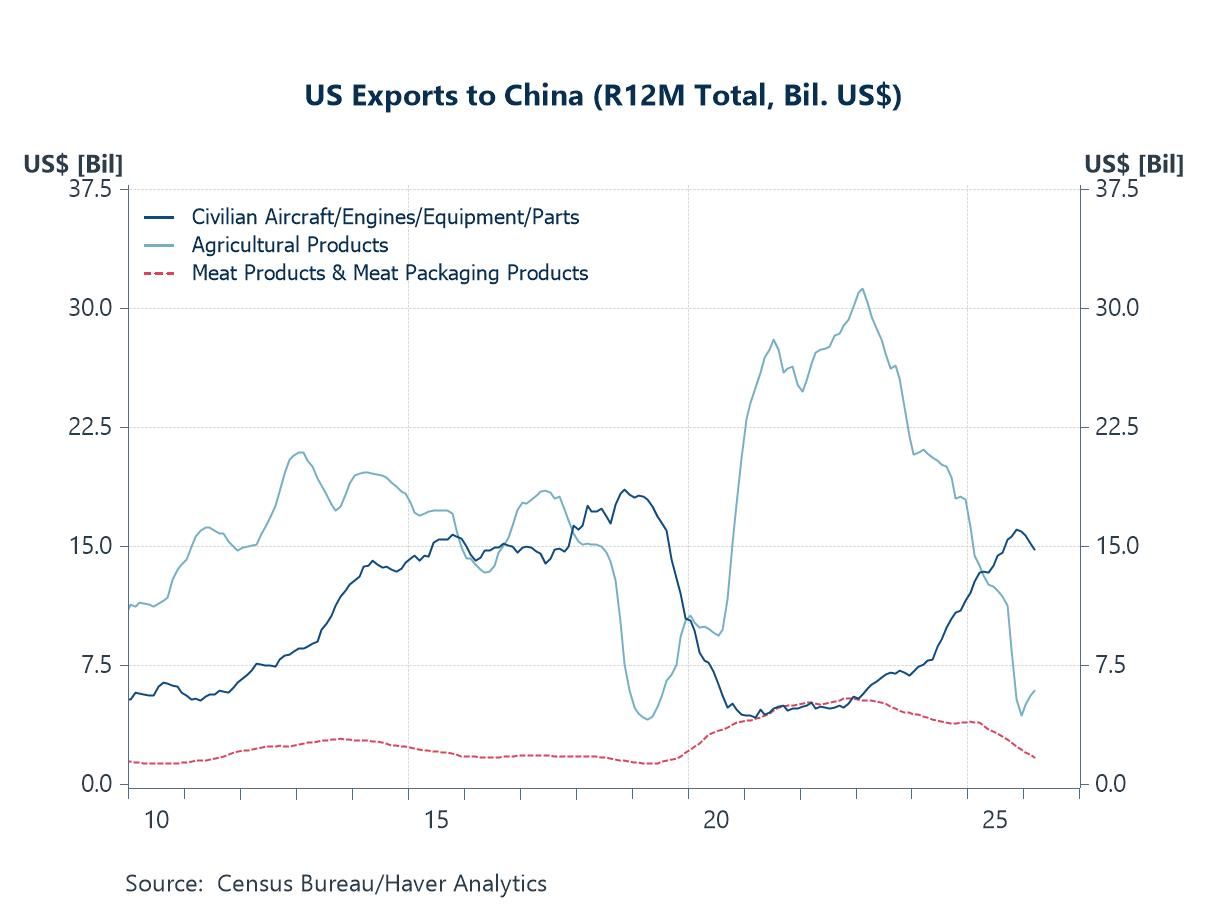

The US-China summit The highly anticipated US–China summit concluded last week, with few details released immediately afterward. More information emerged early this week, as the White House outlined several key developments. Perhaps most importantly, though largely symbolic at this stage, the two sides agreed to build a “constructive relationship of strategic stability.” While the phrase does not imply any concrete policy actions, it may signal a shift away from the repeated tensions and frictions that have characterized recent interactions. The US and China also agreed that the Strait of Hormuz should be reopened, although no specific measures were announced to achieve this. On more tangible outcomes, the White House said China approved an initial purchase of 200 Boeing aircraft for Chinese airlines and committed to buying at least $17 billion of US agricultural products annually from 2026 to 2028. China also restored market access for US beef by renewing expired registrations for more than 400 US beef facilities and adding new listings, while resuming imports of US poultry.

Chart 1: US exports to China

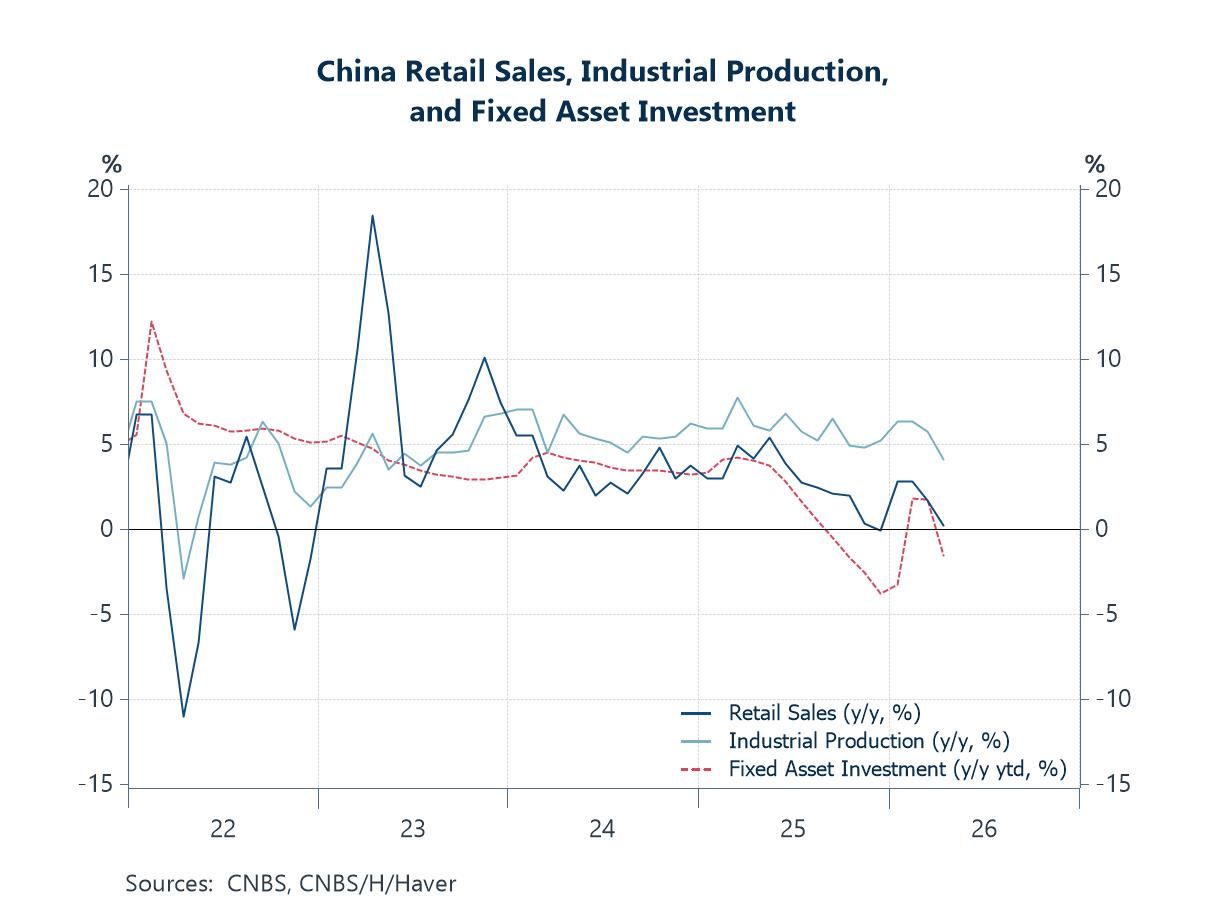

China’s latest data releases Overall, the US–China summit signalled a more conciliatory tone between the world’s two largest economies, with the initially announced agreements broadly reinforcing that shift, including plans to establish two new boards focused on trade and investment. Meanwhile, China’s latest data releases offered further insight into the economy’s performance amid the ongoing oil supply squeeze linked to disruptions in the Strait of Hormuz. Extending the slowdown already evident in March, April data showed weaker growth in retail sales, industrial production, and fixed asset investment, as illustrated in chart 2. In the case of fixed asset investment, year-to-date growth slipped into contraction territory. The increasingly two-speed nature of China’s economy is becoming more apparent. On one hand, robust exports and still-solid manufacturing activity continue to support overall growth. On the other, softer retail sales and broader domestic demand remain a persistent drag on the economy.

Chart 2: China retail sales, industrial production, and fixed asset investment

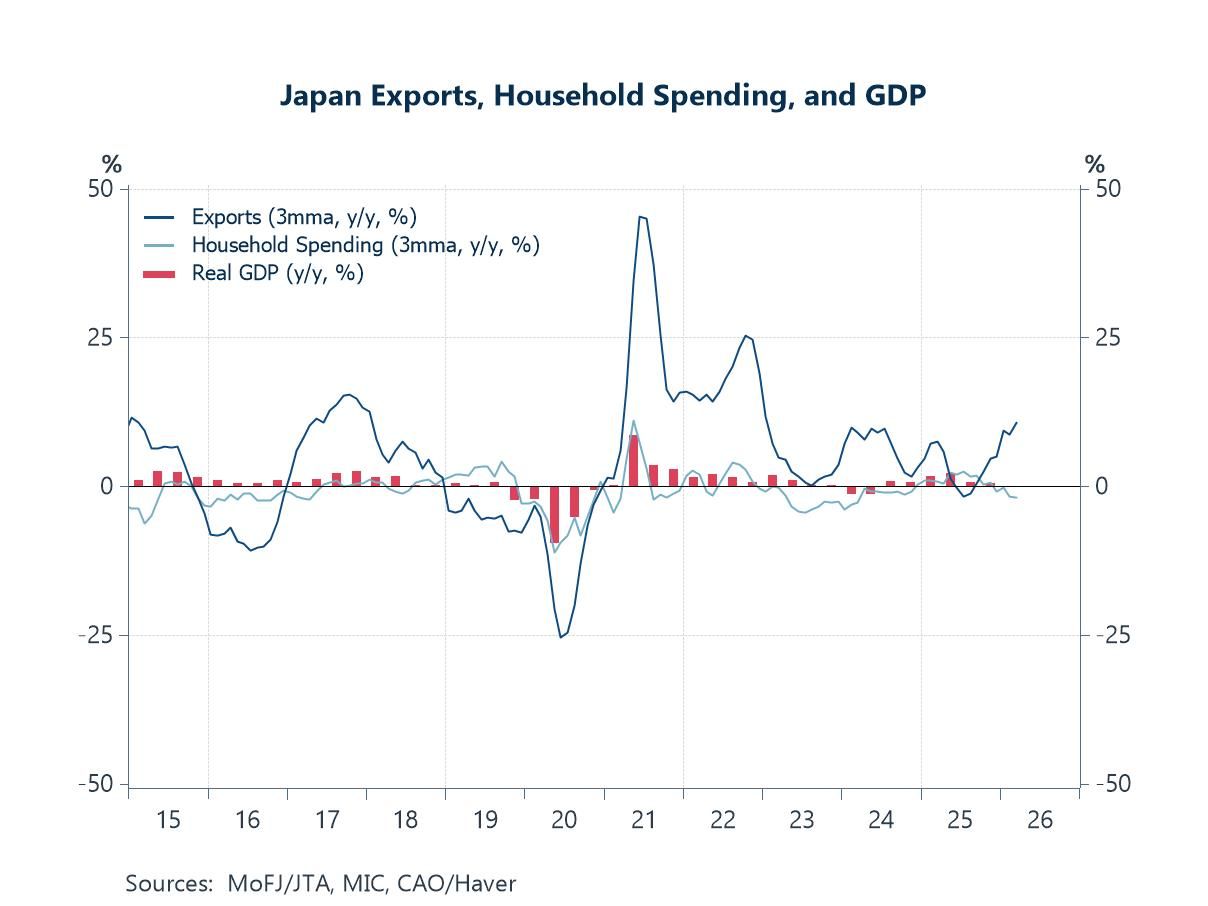

Japan Beyond China, Japan will also be in focus this week, with several key indicators on growth and inflation due for release. Most notably, Japan’s preliminary Q1 GDP reading, due Tuesday, will provide the first comprehensive snapshot of the economy after incorporating the initial effects of the Middle East conflict. As with China, Japan’s economy exhibits a two-speed dynamic. Strong export growth is likely to have supported Q1 activity, reflecting resilient external demand. However, domestic indicators such as household spending continue to point to a fragile underlying picture (chart 3). This leaves Japan exposed to a similar risk as China: If external demand weakens under the weight of rising oil prices and broader uncertainty stemming from disruptions in the Strait of Hormuz, growth could come under significant pressure in the absence of secondary growth drivers.

Chart 3: Japan exports, household spending, and GDP

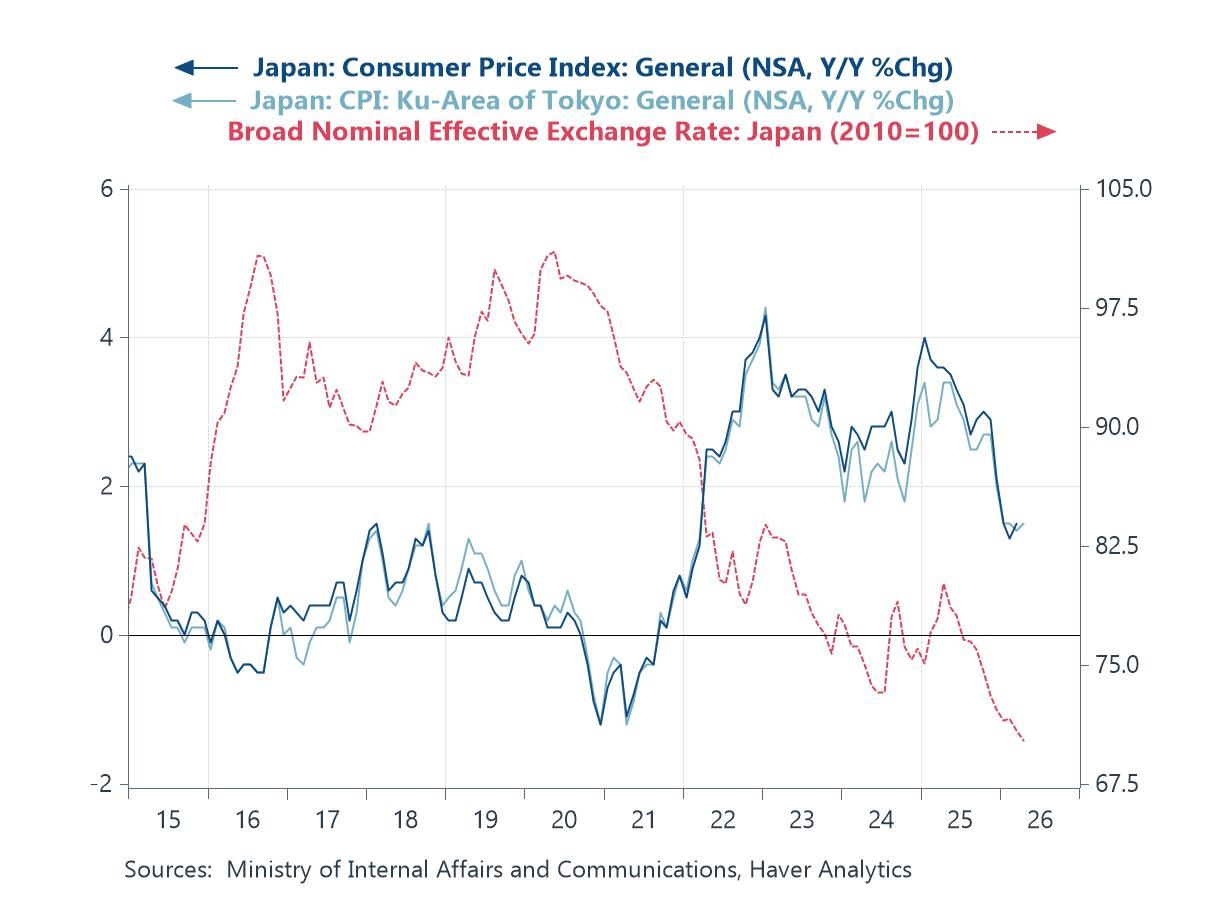

Inflation will also be a key focus in Japan this week, given its implications for household purchasing power, real economic growth, and monetary policy. While inflation is not yet showing a full resurgence, nationwide consumer price inflation picked up in March (chart 4), and Tokyo CPI data pointed to a modest firming in price pressures in April. These developments have coincided with a prolonged weakening of the yen, which, while supportive of exports, also raises inflationary pressures by increasing the cost of imported goods. If inflation were to return to the peaks seen in previous years, the Bank of Japan could once again face a policy dilemma, particularly if economic growth slows at the same time. In that scenario, the BoJ would need to balance the risks of persistent inflation against the need to support a weakening economy.

Chart 4: Japan consumer inflation and the yen

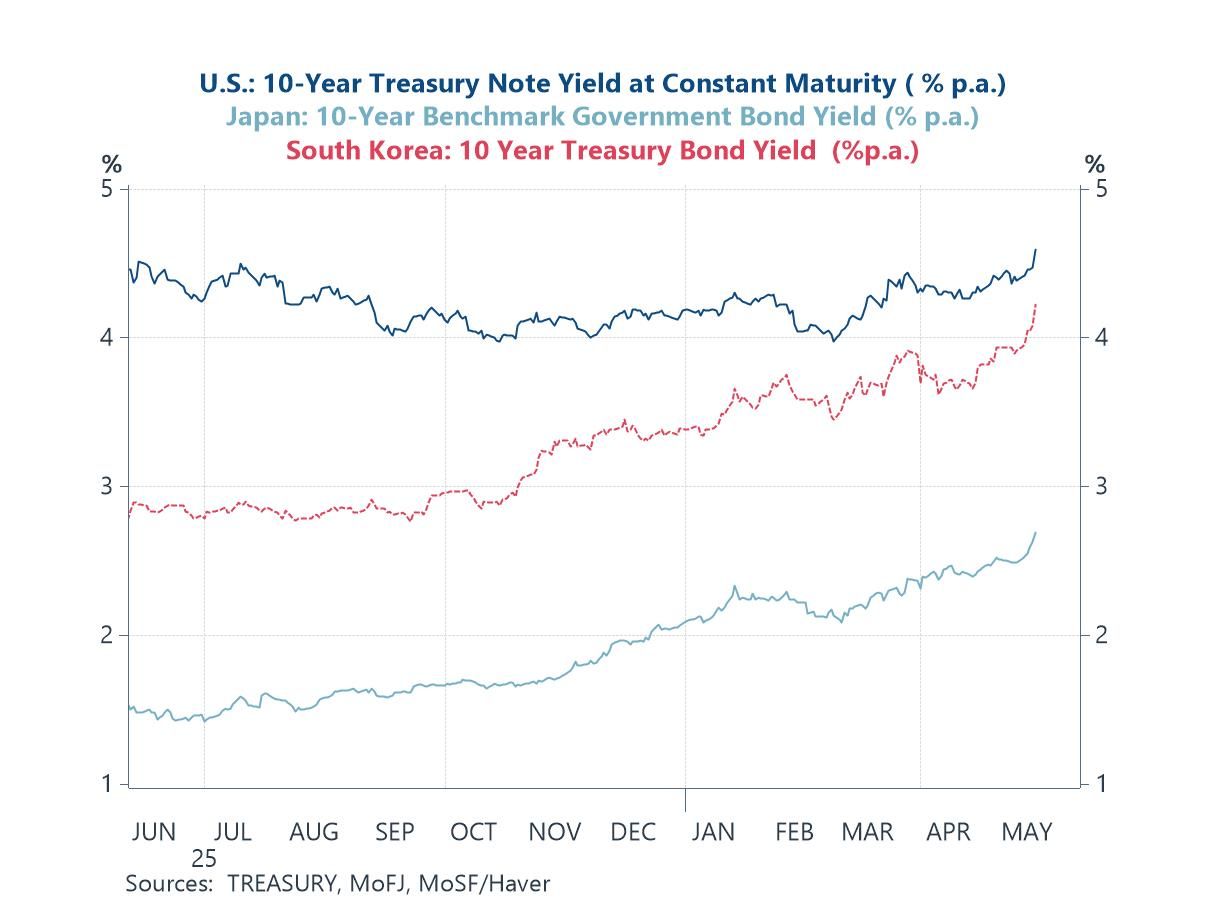

Market shifts Zooming out to broader market developments, and taking into account the recent US–China summit, the ongoing closure of the Strait of Hormuz, and earlier AI-driven optimism, it appears that AI enthusiasm has, for now, ceded its role as the dominant market driver. In its place, renewed inflation concerns have taken centre stage, weighing on bond prices and pushing yields higher, as shown in chart 5. This dynamic is particularly evident in some economies, such as Japan. While nominal government bond yields have risen sharply, real yields have edged lower, implying that inflation expectations have increased. These rising inflation expectations likely reflect the continued apparent impasse in US–Iran negotiations, along with the absence of concrete actions to reopen the Strait of Hormuz and ease pressure on global energy markets.

Chart 5: US, Japan, and South Korea 10-year yields

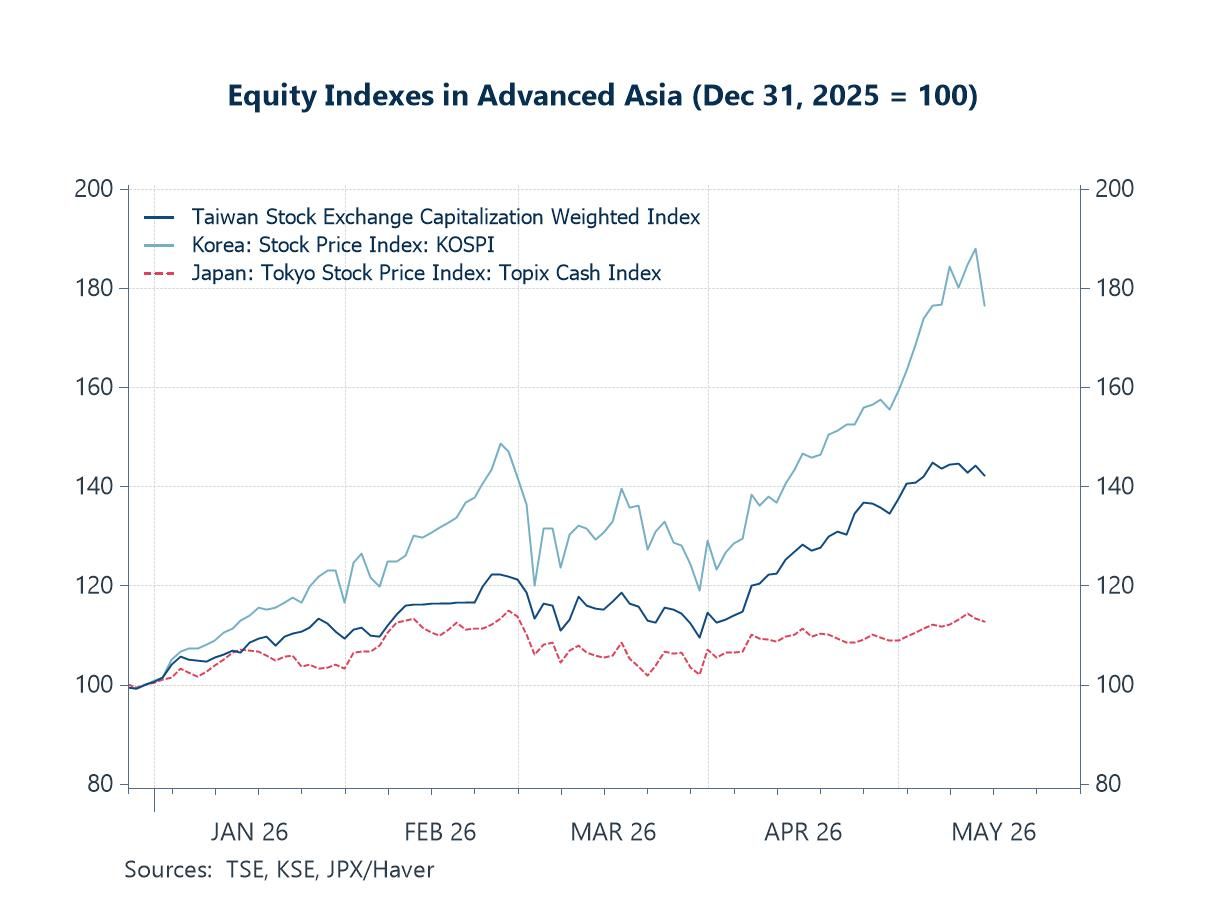

At the same time, AI optimism—which had previously underpinned equity market performance—has appeared to lose some momentum as a dominant price driver, with inflation concerns moving to the forefront. As shown in chart 6, after months of seemingly uninterrupted gains, equity indices in advanced Asian economies—typically heavy in technology and semiconductor exposure—pulled back last Friday, with further declines observed in Monday’s trading session. This shift has coincided with firmer crude oil prices, reinforcing the narrative that inflation risks and supply-side pressures linked to the Strait of Hormuz disruption are now firmly back in focus.

Chart 6: Advanced Asian equity indexes

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief