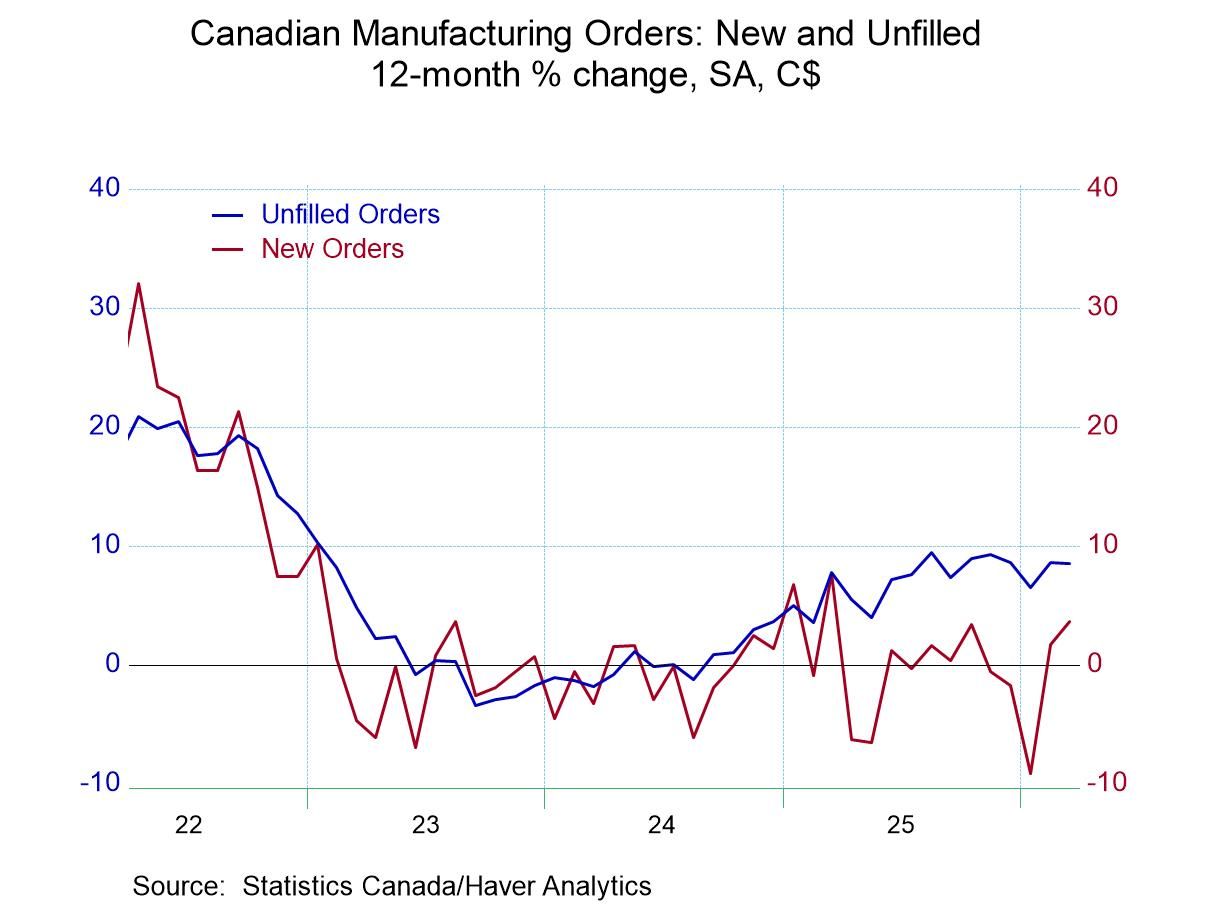

Canadian Industry Perks Up

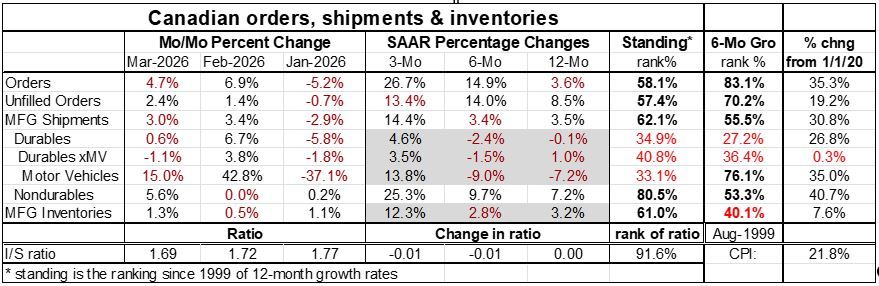

Industrial orders in Canada are back on an expansion path with orders growing 4.7% in March on top of a 6.9% gain in February. These statistics chronicle Canadian orders digging out from a hole they fell into early in 2026. Now the data show emerging sequential growth in Canadian orders, which are advancing 3.6% over 12 months at a 14.9% annual rate over six-months, and a 26.7% annual rate over three-months. Still, on the chart that plots the year-over-year growth rates these recent accelerated rates of growth appear as mere recoveries from what had been earlier weakness. It remains to be seen how much acceleration the Canadian economy will actually undergo.

Unfilled orders expanded in March for the second month in a row, growing 2.4% after growing 1.4% in February once again following the recovery theme.

Manufacturing shipments grew by 3% in March after growing 3.4% in February and after dropping sharply in January - again echoing the recovery theme. Durable goods show two months of increases with the March increase weak after a very strong rise in February. Motor vehicle output recovered very strongly in February, after falling at a 37.1% annual rate in January; motor vehicle output is up by 15% in March, a hefty growth rate but short of what was posted in February. Once again, we see an echo of the theme of recovery. However, shipments of durable goods excluding motor vehicles are less robust, after dropping 1.8% in January output rose by 3.8% in February and has fallen back, dropping by 1.1% in March, a small fly in the ointment of this recovery theme for Canada. And nondurable goods shipments saw a small increase in January of 0.2%, a flat February, and now an extremely strong, 5.6% month-to-month gain in March.

Canada's sequential growth rates are on the verge of showing broad acceleration. Orders clearly do accelerate from 12-months to six-months to three-months. Unfilled orders, however, accelerate over six-months compared to 12-months and then take a small step back over three-months to an annualized growth rate of 13.4% - a very small step back that is still far above the 12-month growth pace. Manufacturing shipments, too, show a small flaw in acceleration as the 6-month pace dips ever so slightly before logging a very strong 3-month pace. Durable goods then are an exception to the acceleration theme; however, nondurable goods get back on board with the strong acceleration move.

Rankings The rank standings for these categories are based on annual growth rates and comparison with data extend back approximately 25 years. Orders have a 58-percentile standing, unfilled orders have a 57-percentile standing, while manufacturing shipments have a 62-percentile standing. Shipments for durable goods durables excluding motor vehicles and from motor vehicles as a stand-alone have rankings in their 30th- to 40th-percentiles, below their historic medians. (medians occur at a ranking of 50). However, nondurables have an extremely strong 80.5 percentile standing. The data are consistent, the recovery and progress with the exception that durable goods shipments that are not fully on board and languish below their historic median results. Ranking the data over six-month growth rates improves the results somewhat and brings motor vehicles on board for a growth rate that is above its historic median.

Signs of improvement Goods-based industry shows signs of picking up even in March as oil prices were rising and industry was facing greater challenges. The US industrial production report for April, similarly, shows acceleration across the board, even as the economy continued to deal with the difficulties of rising oil prices. Of course, the Canadian US economies are closely linked; we would expect the manufacturing sectors to be performing with some degree of synchronization. However, there's no reason to be complacent about the outlook. Oil prices have continued to rise, the challenge to consumers is strong and across all countries. In the US special tax cuts enacted last year, which went into effect earlier this year, have helped to deliver extra money to consumers that have helped them deal with the oil price shock. But these were funds that were supposed to help stimulate the economy to higher growth and were planned by the President to help him with midterm elections coming later in the year. The US economy still has to deal with those realities with sharply divided political reality as well.

Outlook The US acrimony with Canada has taken a back burner for a while. And as that has happened the Canadian economy has come back to life. However, Canada still has some problems with inflation although it also has a broader inflation target to accommodate some flexibility. And the prospect for more inflation because of global oil prices continues to hang in the balance. The results for March are encouraging but certainly not definitive. Canada has mounted a nice recovery after a period of difficulty earlier in the year but it's still hard to say what comes next.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia