Global| Mar 14 2008

Global| Mar 14 2008Michigan Consumer Sentiment Fell Again

by:Tom Moeller

|in:Economy in Brief

Summary

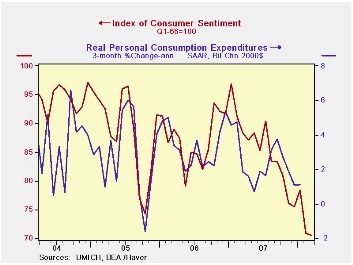

The University of Michigan's consumer sentiment index, in the preliminary reading for March, fell another 0.4% m/m to 70.5 after the 9.7% plunge during February. Consensus expectations had been for a somewhat sharper decline to a [...]

The University of Michigan's consumer sentiment index, in the preliminary reading for March, fell another 0.4% m/m to 70.5 after the 9.7% plunge during February. Consensus expectations had been for a somewhat sharper decline to a reading of 70.1 for early this month.

A lower index of expected business conditions during the next year accounted for all of the decline in overall March sentiment. The 1.6% decline followed an 8.4% February drop and left the index at its lowest since early 1992. Expectations for business conditions during the next year fell 6.0% (-49.5% y/y) but expectations for conditions over the next five years rose, making up virtually all of a February decline. They remained down 7.4% y/y. Expectations for personal finances also improved and made up a February drop but still were down 7.4% y/y.

Opinions about government policy were stable m/m (-22.5% y/y) following the sharp 11.5% shortfall during February. The percentage of those surveyed who indicated that they thought government was doing a good job made up the February decline. They rose to 13% but an increased 44% had a poor opinion.

Expectations for inflation during the next twelve months surged to 4.6%, the highest level in nearly two years though inflation expectations during the next five to ten years fell slightly to 3.3%.

The current conditions index rose a slight 1.0% m/m after the 11.2% February slide. The view of current conditions for buying large household goods ticked up 1.6% after falling 15.8% m/m in February and the view of current personal finances was unchanged after a 4.1% (-15.3% y/y) February drop.

The University of Michigan survey is not seasonally adjusted.The reading is based on telephone interviews with about 500 households at month-end; the mid-month results are based on about 300 interviews. The summary indexes are in Haver's USECON database, with details in the proprietary UMSCA database.

Assessing Employment Growth in 2007 from the Federal Reserve Bank of San Francisco can be found here.

| University of Michigan | March (Prelim) | Feb | Jan | March y/y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 70.5 | 70.8 | 78.4 | -20.2% | 85.6 | 87.3 | 88.5 |

| Current Conditions | 84.6 | 83.8 | 94.4 | -18.3% | 101.2 | 105.1 | 105.9 |

| Expectations | 61.4 | 62.4 | 68.1 | -22.0% | 75.6 | 75.9 | 77.4 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief