Global| Jan 15 2010

Global| Jan 15 2010Michigan Consumer Sentiment Edges Higher

by:Tom Moeller

|in:Economy in Brief

Summary

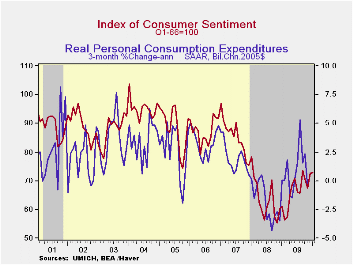

Improvement in consumer attitudes continues. The Reuters/University of Michigan Index of Consumer Sentiment for mid-January ticked up to 72.8 from 72.5 last month. Though the latest figure fell short of Consensus expectations for a [...]

Improvement

in consumer attitudes continues. The Reuters/University of Michigan

Index of Consumer Sentiment for mid-January ticked up to 72.8 from 72.5

last month. Though the latest figure fell short of Consensus

expectations for a reading of 74.0 it was well improved from the low

last fall. During the last ten years there has been a two-thirds

correlation between the level of sentiment and the three-month change

real consumer spending.

Improvement

in consumer attitudes continues. The Reuters/University of Michigan

Index of Consumer Sentiment for mid-January ticked up to 72.8 from 72.5

last month. Though the latest figure fell short of Consensus

expectations for a reading of 74.0 it was well improved from the low

last fall. During the last ten years there has been a two-thirds

correlation between the level of sentiment and the three-month change

real consumer spending.

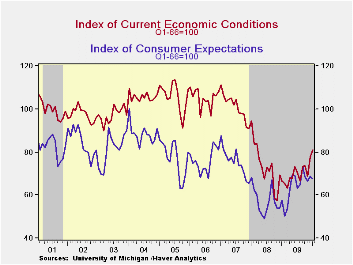

Sentiment about current economic conditions increased another 3.8% after its 13.4% jump from November. The latest was the highest level since March of 2008. Assessments of current financial conditions improved modestly m/m to the highest since September of last year. Buying conditions for large household goods, including furniture, refrigerators, stoves & televisions, also moved up 4.7% to the highest level since January 2008.

The mid-January reading on expected economic conditions fell for the third month in the last four. The 2.0% decline left it down 8.2% from the September high. The outlook for personal finances during the next twelve months fell hard to the lowest level since last March but expectations for business conditions during the year improved and have more-than doubled since last February. Expectations for business conditions during the next five years were unchanged m/m though improved from the 2008 low.

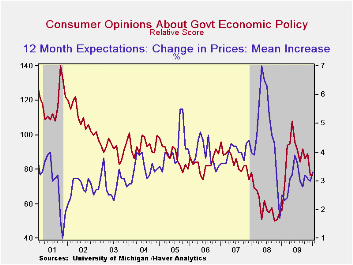

Expected price inflation during the next year rose m/m to 3.3% and it was up from the December 2008 reading of 1.7%. Respondents' view of government policy, which may eventually influence economic expectations, held steady following the sharp December decline. Just twelve percent of respondents thought that a good job was being done by government versus 35% who thought a poor job was being done.

The Reuters/University of Michigan survey data are not seasonally adjusted. The reading is based on telephone interviews with about 500 households at month-end. These mid-month results are based on about 320 interviews. The summary indexes are in Haver's USECON database with details in the proprietary UMSCA database.

Personal Saving and Economic Growth from the Federal Reserve bank of St. Louis is available here here.

| University of Michigan | Mid-January | December | November | Jan y/y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 72.8 | 72.5 | 67.4 | 19.0% | 66.3 | 63.8 | 85.6 |

| Current Conditions | 81.0 | 78.0 | 68.8 | 21.8 | 69.6 | 73.7 | 101.2 |

| Expectations | 67.5 | 68.9 | 66.5 | 16.8 | 64.1 | 57.3 | 75.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief