Global| May 20 2019

Global| May 20 2019Japan's GDP an Upside Surprise

Summary

Japan's real GDP was expected to shrink in Q1 2019 but managed to post a solid expansion instead. A progression of slowing GDP growth rates saw GDP kick back up in Q1 2019, logging a gain at a 2.1% annualized rate in the quarter and a [...]

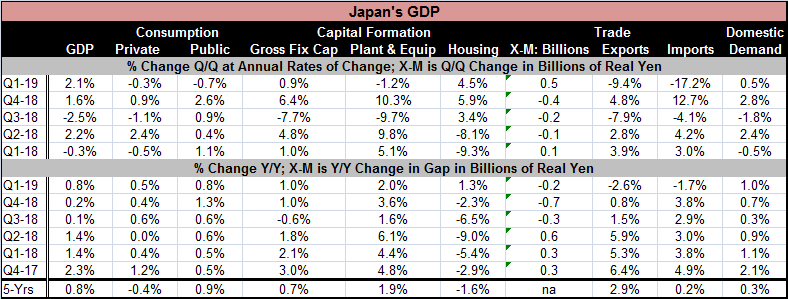

Japan's real GDP was expected to shrink in Q1 2019 but managed to post a solid expansion instead. A progression of slowing GDP growth rates saw GDP kick back up in Q1 2019, logging a gain at a 2.1% annualized rate in the quarter and a year-on-year rise of 0.8%, its strongest since Q2 2018.

Japan's real GDP was expected to shrink in Q1 2019 but managed to post a solid expansion instead. A progression of slowing GDP growth rates saw GDP kick back up in Q1 2019, logging a gain at a 2.1% annualized rate in the quarter and a year-on-year rise of 0.8%, its strongest since Q2 2018.

Japan's GDP result brings with it many of the surprises elements as the U.S. GDP Q1 report. U.S. GDP was stronger than expected, logging a strong-to-firm pace even though much of its growth came from inventories and from falling imports. Japan has these same two characteristics. Like the U.S., Japan posted modest consumption data in Q1 and shows a large drop in manufacturing output as well and a sharp reduction in imports but also manages to post a significant GDP-boosting rise for inventories.

As in the case of the U.S., all of these things make GDP look good right now, but they also raise eyebrows about the future. An inventory build-up speaks of inventory excess and could lead to an order reduction and production cut backs, weakening output in the period ahead. That is even more likely if spending is weak and real final demand in Japan is weak (as it was in Q1 in the U.S.). Moreover, where did the inventories come from? Japan's manufacturing IP in Q1 fell at a 9.7% annual rate and imports imploded, falling at a 17.2% annual rate. So with modest investment absorbing some goods and a slight decline in consumption, where did these inventories come from any way? They were not produced (IP down) and were not imported (imports down) so how did inventories rise? The U.S. and Japan have the same enigmatic result for Q1. And whatever the answer is, it does not bode well for Q2 growth prospects.

The U.S.-China trade snit or war (or whatever you prefer to refer to) is still in progress. This bodes poorly for growth ahead. China is Japan's main trading partner. Unless you live under a rock, you know that China came to town to negotiate the final stage of the trade deal with the U.S. and instead pulled the rug out from under the U.S. negotiators taking back many of the critical ingredients that had been agreed to. Now China refers to the U.S. demands as extravagant- these are things China had previously said it was prepared to do. So no one can tell where the trade deal negotiations are because they most certainly are not where they were.

The U.S.-China trade snit or war (or whatever you prefer to refer to) is still in progress. This bodes poorly for growth ahead. China is Japan's main trading partner. Unless you live under a rock, you know that China came to town to negotiate the final stage of the trade deal with the U.S. and instead pulled the rug out from under the U.S. negotiators taking back many of the critical ingredients that had been agreed to. Now China refers to the U.S. demands as extravagant- these are things China had previously said it was prepared to do. So no one can tell where the trade deal negotiations are because they most certainly are not where they were.

There is no knowing where the trade snit goes next. Trump has put off consideration of auto tariffs for six months; that gives Japan some breathing room. But there is still a lot hanging in the balance and underdetermined on the trade front.

The G20 meeting will be held in Japan and that will be putting it more in the focus. I offer the chart above as a reminder as to what is going on with Japan's population. It is shrinking. Against that background, Japan's GDP is performing exceptionally well. Growth in the future will remain challenged.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief