Global| Feb 26 2008

Global| Feb 26 2008Italy’s Business Morale is Still Sinking

Summary

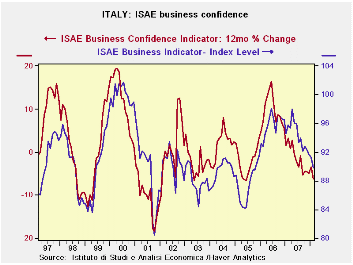

Italy’s Business Confidence Indicator by ISAE is still dropping but not at the sort of speed that we saw in 1998 or in 2000. The downward gradient is steep enough to worry about but not as uncontrolled as in some recent past episodes. [...]

Italy’s Business Confidence Indicator by ISAE is still dropping but not at the sort of speed that we saw in 1998 or in 2000. The downward gradient is steep enough to worry about but not as uncontrolled as in some recent past episodes. Indeed, we plot the index on a two-scale chart that suggests that period of weakening may be coming to an end. On this chart we see that rate of change lags behind the index (of necessity) and that when it stops worsening, that is a sign that the index itself may be near its bottom. In 1998, both the rate of change and the index itself bottomed at the same time. In 2001 the rate of change and the index were separated but both paused before falling and consolidating late in the year. What we see now is that the raw index is still falling but the speed of the drop is not accelerating and that is a constructive development.

Beyond the overall index and its behavior, there are its merits; its details: The survey across total industries and its components show that every component across the main industry sectors is now barely at or below its own midpoint (since January 1999) except for the reading on inventories. Inventories remain high. Overall orders are in the 38th percentile of their range, roughly the same for both domestic and foreign components.

The consumer goods sector is the weakest. Total orders are in their 13th percentile only. Domestic orders are the relative weakest, in their 11th percentile. Foreign orders are just above the bottom third of their range. Inventories are in the top third of their range. And production is in the 13th percentile of its range - in some sense balanced with orders.

Italy is seeing weakness across industry. Business morale is poor. For now, the good news is that the deterioration is not accelerating.

| Italy ISAE Business Sentiment | ||||||

|---|---|---|---|---|---|---|

| Since January 1999 | ||||||

| Feb-08 | Jan-08 | Dec-07 | Nov-07 | Percentile | Rank | |

| Biz Confidence | 89.8 | 91.3 | 91.7 | 92.2 | 43.7 | 68 |

| TOTAL INDUSTRY | ||||||

| Order books & Demand | ||||||

| Total | -13 | -8 | -6 | -7 | 38.1 | 54 |

| Domestic | -16 | -15 | -9 | -11 | 35.7 | 62 |

| Foreign | -17 | -11 | -6 | -9 | 36.4 | 53 |

| Inventories | 5 | 5 | 6 | 6 | 66.7 | 51 |

| Production | -13 | -12 | -4 | -4 | 28.6 | 75 |

| INTERMEDIATE | ||||||

| Order books & Demand | ||||||

| Total | -14 | -13 | -13 | -11 | 40.0 | 56 |

| Domestic | -14 | -17 | -15 | -12 | 43.4 | 49 |

| Foreign | -21 | -13 | -13 | -10 | 33.9 | 70 |

| Inventories | 4 | 3 | 6 | 7 | 65.5 | 29 |

| Production | -13 | -14 | -11 | -5 | 31.0 | 64 |

| INVESTMENT GOODS | ||||||

| Order books & Demand | ||||||

| Total | -4 | 1 | 4 | 4 | 50.7 | 42 |

| Domestic | -8 | -5 | 0 | -6 | 50.7 | 39 |

| Foreign | -8 | -1 | 2 | -1 | 44.6 | 46 |

| Inventories | 6 | 4 | 3 | 6 | 62.2 | 34 |

| Production | -4 | -1 | 6 | 5 | 40.9 | 46 |

| CONSUMER GOODS | ||||||

| Order books & Demand | ||||||

| Total | -23 | -18 | -5 | -10 | 13.6 | 93 |

| Domestic | -24 | -21 | -8 | -15 | 11.1 | 90 |

| Foreign | -18 | -24 | -11 | -15 | 36.2 | 57 |

| Inventories | 6 | 6 | 5 | 8 | 65.4 | 47 |

| Production | -20 | -17 | -2 | -8 | 13.9 | 95 |

| Total number of months: 110 | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief