Global| Apr 09 2019

Global| Apr 09 2019Italian Retail Sales Tick Higher

Summary

Italian retail sales ticked higher in February, rising by 0.1% after a 0.6% January gain. Still, retail performance is poor with nominal sales up by less than 1% over 12 months (0.9%) and dead flat over both six months and three [...]

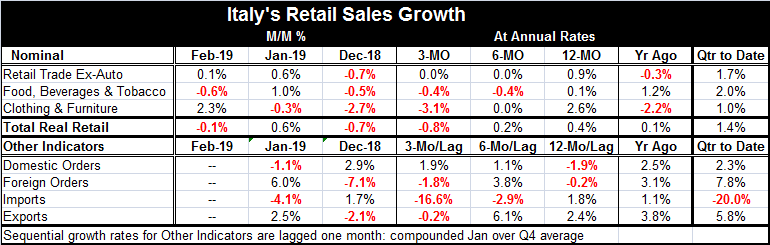

Italian retail sales ticked higher in February, rising by 0.1% after a 0.6% January gain. Still, retail performance is poor with nominal sales up by less than 1% over 12 months (0.9%) and dead flat over both six months and three months. That sort of momentum is not encouraging.

Italian retail sales ticked higher in February, rising by 0.1% after a 0.6% January gain. Still, retail performance is poor with nominal sales up by less than 1% over 12 months (0.9%) and dead flat over both six months and three months. That sort of momentum is not encouraging.

Expressed in real terms, Italian retail sales fell by 0.1% in February after a 0.6% rise in January and a 0.7% decline in December. Over 12 months Italian retail volumes are up by just 0.4% and over six months real sales are rising at a 0.2%.annual rate. Over three months retail sales are falling at a 0.8% annual rate.

However, on a quarter-to-date basis, real retail sales are expanding at a 1.4% annual rate.

Of the four indicators in the table two are declining in January and three show net declines over three months. Italian domestic orders show a drop over 12 months but net gains over six months and three months. But foreign orders do not echo that strength as they are lower over 12 months and falling at a 1.8% annual rate over three months. Italian exports have been at least firm, rising by 2.4% over 12 months and at a 6.1% pace over six months, but that growth has soured to a -0.2% declining pace over three months. Imports, a statistic that speaks to domestic growth and demand, show a distressing trend. Imports ae up by 1.8% over 12 months then are falling at a 2.9% annual rate over six months and now are plunging at a 16.6% annual rate over three months. To say the least, Italian domestic orders and imports seem to be contradictory.

In the quarter-to-date, these indicators also are mixed with solid-to-strong growth in exports and foreign orders, a weaker, 2.3% annual rate rise in domestic orders, and a contrary 20% annual rate plunge in imports. Of course, some of the import weakness could be oil prices, but even oil should not dominate the import series like that. In fact, Italian imports are weak across most import categories- emphasizing the weak domestic demand signal. Italy’s unemployment rate bottomed months ago; and while it is not on a rising trend, it is fluctuating in a range well above its cycle low.

Italian politicians are trying to unite with other anti-immigrant parties in the EMU to form a bloc of opposition to current immigration policies that have disadvantaged Italy. There is also a struggle between the government and the central bank in which the government is trying to gain leverage and control over the Bank of Italy and to gain access to Italy’s gold stock (story here). Italy has the fourth highest gold stock in the world, valued at over $100 billion at current prices. The Five Star movement hopes to be able to unlock significant spending power by gaining access to Italy’s gold. Selling gold would be a way to spend and not be out of compliance with EU Commission rules on debt.

It is surprising that the Italian economy continues to function as well as it does with so much political discord and ongoing economic dislocation. Italy’s growth remains weak and inflation is running at a 1.2% pace overall; the HICP excluding food and energy is rising at just a 0.5% pace. But Italy does have a number of issues to deal with and its finances are hog-tied by EU Commission rules on deficit spending and debt-to-GDP ratios. Italy’s populist political parties continue to seek out-of-the-box solutions to their spending priorities.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief