Global| Nov 13 2013

Global| Nov 13 2013IP European-style Continues to Tease European Paradox

Summary

EMU industrial production has fallen in eleven of the past 20 months. The chart shows that year-over-year IP growth has been snaking along, just below zero, for some time. Other metrics like the manufacturing and services PMIs from [...]

EMU industrial production has fallen in eleven of the past 20 months. The chart shows that year-over-year IP growth has been snaking along, just below zero, for some time. Other metrics like the manufacturing and services PMIs from Markit seem to show a bit more lift. The OECD LEIs, just released yesterday, point the way to better growth too. But IP itself - not a caricature of it, not an indicator, nor a diffusion shadow-metric - continues to erode. The latest data shows IP is off by 0.7% month-to-month, but IP is higher by 0.2% year-over-year. The year-over-year rise is only the second in the last four months. There was another gain some seven months ago. EMU has not been able to post positive gains in IP and to stick with it.

EMU industrial production has fallen in eleven of the past 20 months. The chart shows that year-over-year IP growth has been snaking along, just below zero, for some time. Other metrics like the manufacturing and services PMIs from Markit seem to show a bit more lift. The OECD LEIs, just released yesterday, point the way to better growth too. But IP itself - not a caricature of it, not an indicator, nor a diffusion shadow-metric - continues to erode. The latest data shows IP is off by 0.7% month-to-month, but IP is higher by 0.2% year-over-year. The year-over-year rise is only the second in the last four months. There was another gain some seven months ago. EMU has not been able to post positive gains in IP and to stick with it.

As the chart shows, and as other metrics hint, IP is making progress and it will start showing consistent growth soon. Or that is the hope.

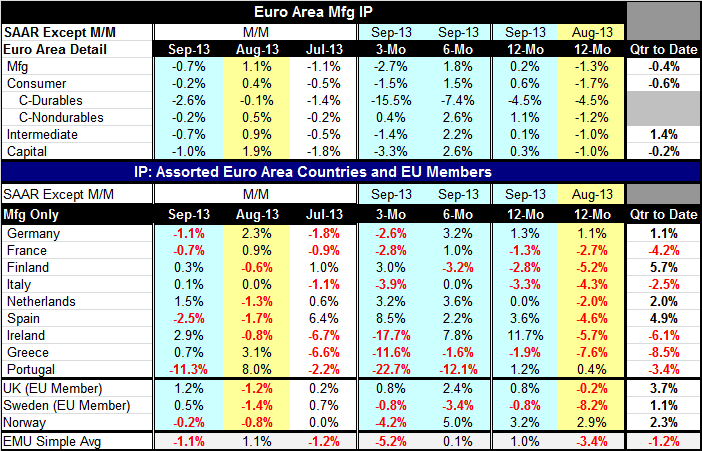

In EMU by sector IP fell in each of them in September: consumer goods, capital goods and intermediate goods. Over three months IP is down in each of these sectors as well. But as of September, over six months only output in consumer durable goods is lower. It is also the only declining output subsector over 12-months. Ominously, the weakness in consumer durables purchases is getting progressively weaker moving from 12-months to 6-months to 3-months. That is not a sign that output is gathering strength. If the consumer is not along for the ride, how long can the ride last?

In the quarter-to-date column, which, this month, is also the preliminary reading for IP growth in Q3, IP is falling in each sector except for intermediate goods. IP in Q3 is falling at a 0.4% annual rate.

In the table, we see that, of the nine EMU members listed, most are showing IP increases in each of the last two months. However, over three-months, output is falling on balance in six of nine of these member states. The countries with rising IP over three-months are Finland, the Nether lands and Spain. Over six-months and 12-months most of these same countries show growth. What does the weakness over three-months mean against this background? It is evidence of backsliding. In the third quarter, five of nine member nations are showing IP declines.

Only Ireland, the Netherlands and Germany have seen their own IP rise so much in the recovery that their current IP levels are less than 10% from their past cycle highs. Output in Spain and Greece is still 30% or more below their respective cycle peaks. Finland and Italy are still short by about 25%. There clearly have been very different amounts of progress made by fellow EMU nations.

Non-EMU nations the UK, Sweden and Norway are faring better. Norway's IP is only 2% below its past cycle peak. In the UK IP is about 9% below its peak. For Sweden it is still 20% below. Each of these countries is showing a solid advance in IP in Q3. However, like EMU members two of the three also show some backtracking over the last three-months.

On balance while Europe has made some progress there is not much evidence here of building momentum. On the contrary, over the past few months there seems to be some set back. European non-EMU members seem to be doing a bit better, although most of the countries here show some recent weakness. The different degrees of progress made since the financial crisis put countries in different positions in terms of what they need and what can be expected of them. Yet there is only one monetary policy for all in EMU (one size fits none?). And, there is no fiscal transfer agency or rule. You can look at this progress and find the glass is half full or half empty- it's all the same. There has been some progress, but there is still so much to do and no consensus on how to get it done. That remains the paradox of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief