Global| May 03 2019

Global| May 03 2019Internal EMU Inflation Trends Go Awry

Summary

Since the EMU formation, Germany has been the low inflation country. Germany as the largest economy in the EMU gets the greatest weight in setting EMU macroeconomic data, including the HICP, for just that reason. In the past ‘most’ [...]

Since the EMU formation, Germany has been the low inflation country. Germany as the largest economy in the EMU gets the greatest weight in setting EMU macroeconomic data, including the HICP, for just that reason. In the past ‘most’ EMU members overshot the mark for allowable EMU inflation, but EMU-wide inflation stayed on course because Germany ran an inflation rate below what was prescribed and that event combined with Germany’s large weight meant that EMU inflation would stay on track and below its prescribed level of just less than 2%.

Since the EMU formation, Germany has been the low inflation country. Germany as the largest economy in the EMU gets the greatest weight in setting EMU macroeconomic data, including the HICP, for just that reason. In the past ‘most’ EMU members overshot the mark for allowable EMU inflation, but EMU-wide inflation stayed on course because Germany ran an inflation rate below what was prescribed and that event combined with Germany’s large weight meant that EMU inflation would stay on track and below its prescribed level of just less than 2%.

That was then and this is now.

Great recession made for some great changes

From June 2000 to November 2012, 59% of the time a majority of EMU members had inflation at or above 2% in the same month. But since the Great Recession, things have changed. In the last 76 months since December 2007, there have only been seven instances (10% of the time) when half of more or the EMU members had inflation at or above the 2% mark in the same month. The financial crisis really changed things in the EMU and conditions in the EMU continue to evolve.

Germany is King...not what it wanted

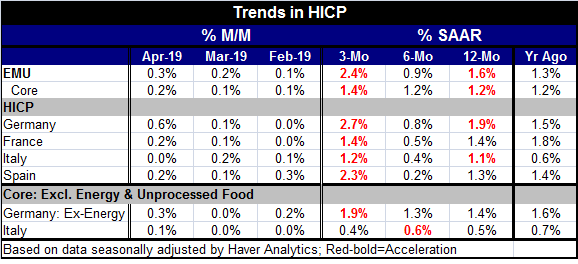

Among the four largest EMU economies, Germany now has the highest rate of HICP inflation in April. The German HICP rise over 12 months is 1.9%. For France it is 1.4%; for Spain it is 1.3%; for Italy it is 1.1%. Inflation-conscious Germany, a country that is already running a contractive fiscal surplus, is running the highest inflation rate among the four largest EMU economies. That turns history on its head.

Running out of slack?

Viewed in Keynesian terms, this is not surprising since Germany also has the lowest unemployment rate in the EMU at 3.2%. The French rate is at 8.8%, the Spanish rate is at 14.0% and the Italian rate is at 10.2%. And yes all this countries are in the same customs and monetary union. Against that backdrop, it is not surprising that inflation in Germany is rising faster than in the other three largest EMU economies. And Germany may actually be feeling more constraints as its unemployment rate fell by just 0.3 p.p. over the last 12 months compared to declines of 0.4 p.p. for France, 1.9 p.p. for Spain and 0.7 p.p. for Italy. The other large EMU economics are still finding ways to use up labor making use of slack, while Germany seems to have a hard time finding idle resources to employ.

German inflation high and rising

And German inflation is rising rapidly while the other three large EMU countries see less pressure. However, over six months all see slightly lower inflation compared to 12 months. But over three months compared to 12 months, pressures are rising. For Germany, annualized three-month inflation (SAAR) is up to a 2.7% pace, an acceleration of 0.8 percentage points from its 12-month pace. Spain’s acceleration is slightly faster as its three-month pace accelerates to 2.3%, a rise of a full percentage point. Italy has inflation acceleration of just 0.1 percentage point from 12-months to three-months while France’s inflation rate remains the same for those two paces. So Germany is experiencing the highest inflation rate in this grouping and the most pressure over three months and has second highest acceleration to deal with.

German ex-energy inflation accelerates too

German ex-energy inflation is up at a 1.4% pace over 12 months. It also backtracks over six months then accelerates over three months compared to 12-months rising 0.5 percentage points faster. In contrast, Italian core inflation (excluding food and energy) is up by just 0.5% over 12 months. It actually bumps up over six months, but over three months the Italian pace is below its 12-month pace.

French and Italian inflation are below German inflation (!)

...and both trends are weaker than Germany’s trend that is moving up strongly

Germany loses its spot as having had its low inflation ranking in the EMU

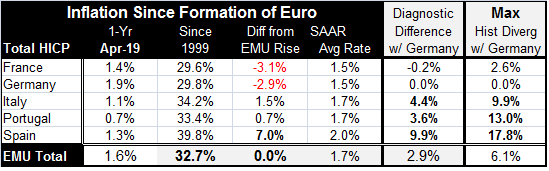

The table right below provides some historic perspective on how inflation has evolved in the EMU. Typically inflation has been lowest in Germany as the price level rise in Germany had for a long time been by less than anywhere else. But now as Germany has acquired some inflation issues, France has taken over as the country (in this group) with the smallest rise in its HICP since the EMU was formed. It nosed out Germany at the finish line by 0.2 percentage points based on April results since the German price level rose by 0.6% and the French price level rose by only 0.2%. Italian inflation has been higher generally as Italy’s price level has risen by 4.4% more than Germany’s since the EMU was formed. Portugal’s price level has risen by 3.6 percentage points more and Spain’s price level has risen by 9.9 percentage points more. This metric matters since it refers to actual differences in the price level since all these countries use the same currency. The far right hand column shows that these countries have all made some progress or substantial progress in closing the gap with Germany compared to their worst performance since the EMU was formed. Getting the price levels realigned and keeping inflation rates in the community more closely in touch, as well, will make the job of making monetary policy easier for the ECB.

New EMU dynamics

But for now there are some different dynamics in the EMU. Most of them seem to relate to the way oil prices ae impacting the various economies, but that is not the whole of it. And since the ECB makes policy for the community and not Germany, there could be some uncomfortable months ahead as German domestic inflation could reach above the 2% mark with EMU-wide inflation lower causing the ECB to hold its ground at a time that Germans would like to have a rate hike.

Temper inflation...but growing strains?

EMU-wide prices are rising by only 1.6% over 12 months and are up at a 2.4% annual rate over three months. That’s a 0.8 percentage point acceleration, the same as what Germany is experiencing. But the EMU core inflation rate of 1.2% over 12 months is below Germany’s 1.4% ex-energy pace. The EMU core rate only accelerated by 0.2 percentage points over three months compared to its 12-month pace of 1.2%, bringing the EMU core pace to 1.4% over three months. That is well below Germany’s ex-energy three-month pace of 1.9%. Still, since Germany has a large weight in the EMU if German inflation continues to rise above 2% it won’t be long before EMU inflation will follow, unless there is severe economic weakness and countervailing downward price pressure elsewhere. That does not seem to be in the cards. Italy has had two consecutive quarters of negative growth (small contractions), but it is growing again. Growth in the rest of the EMU seems on track too. Still, it is clear that the dynamics in EMU are changing. There are already concerns that there could be some repositioning of influence in the EU, the Area’s rule-making body, when this next round of elections is completed. There might also be different and unusual macroeconomic strains to add to that tension.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief