Global| Mar 06 2003

Global| Mar 06 2003Initial Claims for Jobless Insurance Up Again

by:Tom Moeller

|in:Economy in Brief

Summary

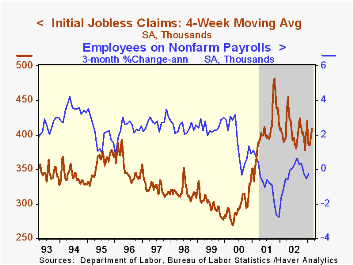

Initial claims for unemployment insurance unexpectedly rose last week, up 2.9% from the prior week's level which was little revised. It was the third consecutive week of significant increase. Claims for all of February were 5.6% [...]

Initial claims for unemployment insurance unexpectedly rose last week, up 2.9% from the prior week's level which was little revised. It was the third consecutive week of significant increase. Claims for all of February were 5.6% higher than January.

The four-week moving average of initial claims rose to 408,750, up 4.6% y/y. During the last ten years there has been a 71% correlation (inverse) between initial claims and the three month growth in nonfarm payrolls.

Continuing claims for unemployment insurance surged 5.4% from the prior week's level which was revised down. It was the highest claimant level since mid-November.

The insured rate of unemployment rose slightly to 2.8%, also the highest level since mid-November.

| Unemployment Insurance (000s) | 3/01/03 | 2/22/03 | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Initial Claims | 430.0 | 418.0 | 9.7% | 405.0 | 405.8 | 299.8 |

| Continuing Claims | -- | 3,516 | 0.1% | 3,588 | 3,021 | 2,114 |

by Tom Moeller March 6, 2003

Nonfarm labor productivity last quarter was revised up slightly more than expected owing to a raised estimate of output growth, now at 1.7% versus the initial estimate of 0.8% growth. Hours worked rose 0.9%, about the same as estimated earlier.

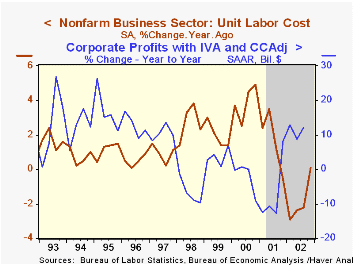

Unit labor cost growth was revised down sharply. The annual decline in unit costs was the first since 1983 and by far the steepest of the postwar era. During the last ten years there has been a 58% (inverse) correlation between year-to-year growth in unit labor costs and corporate profits.

Manufacturing sector productivity growth was revised down to 0.1% (4.4% y/y from 0.7%. The surge in unit labor costs was revised up to 5.4% (0.6% y/y) from 4.6%. For the year, unit labor costs in the factory sector fell 0.7%.

Analysis by the Federal Reserve Bank of San Francisco which analyzes the effect of innovation on productivity can be found here.

| Nonfarm Business Sector (SAAR) | 4Q '02 Revised | 4Q '02 Prelim. | 3Q '02 Final | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|---|

| Output per Hour | 0.8% | -0.2% | 5.5% | 4.1% | 4.8% | 1.1% | 2.9% |

| Compensation | 4.6% | 4.6% | 5.4% | 4.2% | 2.8% | 2.7% | 7.0% |

| Unit Labor Costs | 3.8% | 4.8% | -0.1% | 0.1% | -1.9% | 1.6% | 3.9% |

by Tom Moeller March 6, 2003

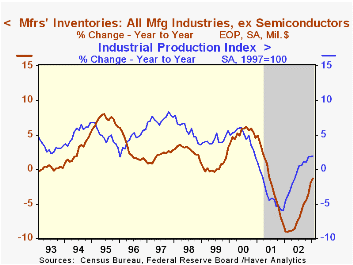

Manufacturing inventories fell just slightly last month following strong accumulation in December.

That strong accumulation in December was limited to the transportation sector (aircraft, light trucks and ships). Outside of transportation, inventories fell slightly last month and have been about unchanged since September.

Inventory declines have continued in a broad range of durable goods industries including computers & electronic products and machinery. Inventories of furniture rose for the second month in three.

Nondurable goods inventories rose 0.2% (+2.0% y/y) for the first rise in three months.

Factory shipments rose a sharp 2.2% (2.2% y/y). Excluding transportation, shipments rose 1.3% (3.1% y/y).

Factory orders rose a sharp 2.1% owing to a steep 2.9% increase in durable goods orders, revised from 3.3% in the advance report.

| Factory Survey (NAICS) | Jan | Dec | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Inventories | -0.0% | 0.6% | -1.3% | -1.9% | -8.0% | 4.5% |

| New Orders | 0.4% | -0.8% | 2.7% | -0.8% | -7.2% | 5.2% |

| Shipments | -0.6% | -1.1% | -0.6% | -1.1% | -5.3% | 4.4% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief