Global| Sep 24 2007

Global| Sep 24 2007Inflation Fears: The Data Behind Them

by:Tom Moeller

|in:Economy in Brief

Summary

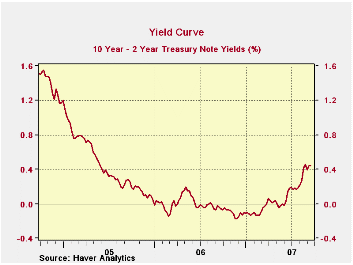

Since the Fed lowered interest rates last week, many now worry that the risk of future price inflation has risen. In fact, if the slope of the yield curve is any measure, i.e., the difference between the yield on the 10 year and 2 [...]

Since the Fed lowered interest rates last week, many now worry that the risk of future price inflation has risen. In fact, if the slope of the yield curve is any measure, i.e., the difference between the yield on the 10 year and 2 year Treasury notes, the credit markets began pricing in that risk last Spring.

The question is did the Fed stoke an inflation fire? Three measures of just how hot that fire is bear watching: GDP growth versus its potential, liquidity, and outside forces, i.e., the price of imported goods.

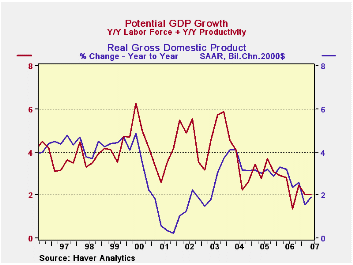

Worry #1 - Potential GDP growth usually is measured by taking the growth in the labor force and adding it to the growth in how productive that labor force is. For the U.S. economy, the slowdown in its potential rate of growth during the last few years is dramatic due to slower productivity growth. At the same time, the actual rate of economic growth has slowed as well, perhaps by enough to alleviate concerns about overheating.

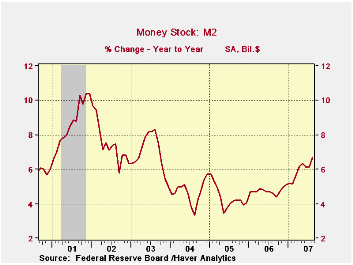

Worry #2 - Growth in liquidity, as measured by the growth in M2, has roughly doubled during the last two years to 6.5%. That may or may not be a rate of growth that is threatening, but it is up. And it has been accompanied by a moderate acceleration in the narrower measures of money growth. M1 growth is up moderately to a still negative 0.4% and a MZM has accelerated sharply to 10.4%.

Worry #3 - This one, maybe, is not so threatening. Prices for imported goods have been decelerating recently due to the past weakness in oil prices that lowered gasoline prices. This, however, is certainly threatened by the recent run-up in crude oil prices. Prices for nonpetroleum imports have been fairly tame, held back by the stability of pricing for automotive products and industrial supplies other than petroleum. What bears watching, however, is the moderate acceleration in the pricing of capital goods as well as the prices for non-automotive consumer goods.

The markets, therefore, seem to be pricing in a very real threat of higher price inflation. Measured inflation, on the other hand has been very well behaved, but that most likely is the result of the past slow growth in liquidity and the past slow growth in import prices.

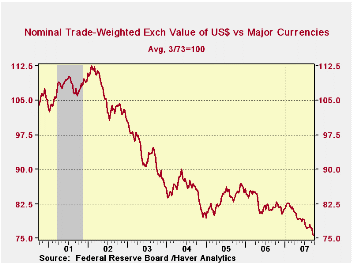

Will inflation accelerate? The answer is yet to be determined, but the recent evidence strongly suggests that it will. Over the short term, what bears watching is just how much economic growth continues to exceed its potential. Another short term factor is whether the growth in the prices of imported goods perhaps becomes more stable. The recent weakness in the trade weighted value of the U.S. dollar does not bode well for that.

All of the data used to research the above analysis are available in Haver's USECON database and the WEEKLY database.

The Effectiveness of Monetary Policy from the Federal Reserve Bank of St. Louis is available here.

How Well Does Employment Predict Output? also from the Federal Reserve Bank of St. Louis can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief